As we enter 2024, Invesco believes this year will present insurers with many different investment opportunities in a relatively stable market and economic environment. Whereas in recent years we have observed rapid, substantial interest rate hikes along with pronounced, albeit short-lived, periods of equity volatility we believe this year will be characterized by greater market stability. While economic growth is likely to continue slowing in the face of restrictive monetary policy, we think growth is likely to improve later in the year as central banks begin easing monetary policy. Additionally, the high inflation observed following Covid is expected to continue abating (see charts below). Against this backdrop, we believe insurers will find a number of compelling portfolio opportunities in both public and private markets.

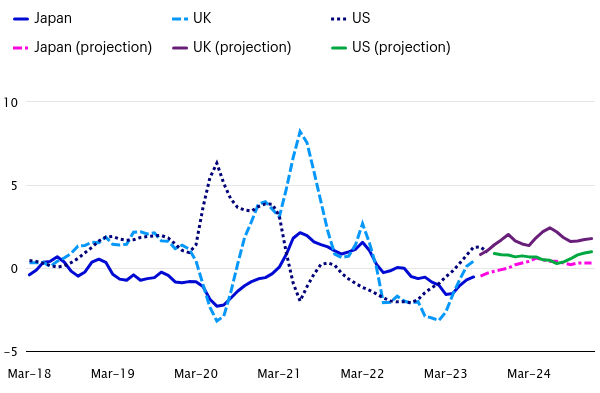

Real wage growth expected to improve in 2024

Note: There can be no assurance that any stated projections will be realized. chart shows monthly real wage growth data for US, UK and Japan from March 2018 to December 2024. Projections are from Invesco and are shown in dotted lines. Sources: Bloomberg L.P., OECD, and Invesco.All data is latest available as of October 31,

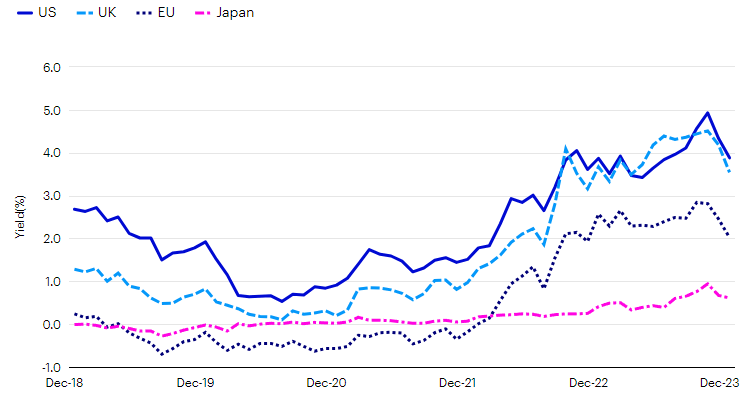

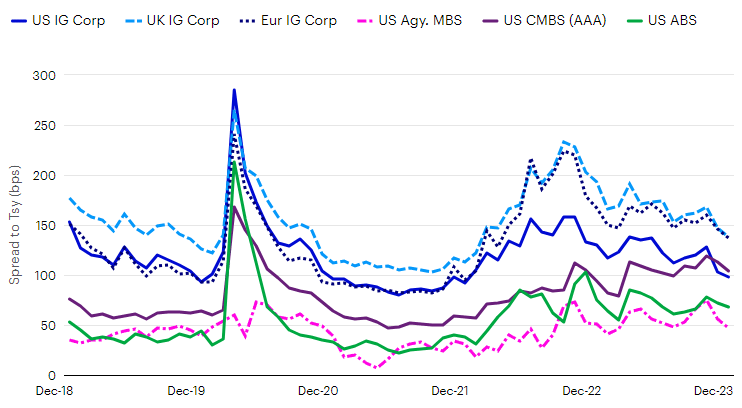

Turning to current market conditions, we have clearly seen a meaningful shift higher in fixed income yields in recent years. As central banks have tightened policy rates to combat high inflation, 10-year sovereign yields are at or near multi-year highs (see chart below) with expectations for central bank easing likely keeping a lid on intermediate and long yields for some time. Meanwhile, spreads – particularly in structured credit – have currently offered reasonable compensation for credit risk, producing all-in yields for US and UK investment grade exposure in the 5% context and European yields in the high 3% context. Relative to the yields observed fairly recently when most of the world’s central banks maintained policy rates at, or even below zero, we believe these public-market yields are attractive for insurers, particularly when considering risk-based capital requirements.

10 Year Gov't Bond Yields

Source: Bloomberg L.P. as of December 29, 2023. An investment cannot be made directly into an index.

Selected Fixed Income Spreads

Source: Bloomberg L.P. as of December 29, 2023. Indices used: US IG Corp = Bloomberg US Corporate Bond Index, UK IG Corp = Bloomberg Sterling Corporate Bond Index, Eur IG Corp = Bloomberg Euro Aggregate Corporate Bond Index, US Agy. MBS = Bloomberg US MBS Fixed Rate Index, US CMBS (AAA) = Bloomberg CMBS Investment Grade AAA Index, US ABS = Bloomberg US Aggregate ABS Index. An investment cannot be made directly into an index.

While we see interesting opportunities in public fixed income, we believe insurers should continue building out or refining their private market portfolios as well. Within private credit, we believe distressed and special situations may offer attractive opportunities in the coming quarters, even if the macroeconomic backdrop remains strong as bottom-up opportunities remain. This means insurers can potentially achieve equity-like returns within credit, enhancing their asset portfolio’s capital efficiency. Similarly, while commercial real estate (CRE) has been under pressure in recent years, the current environment offers attractive CRE debt yields – here again, we believe this is an opportunity to enhance capital-adjusted returns. Within direct lending, opportunities certainly exist but given the amount of investment capital that has entered the space we believe strong underwriting and debt covenants are as important as ever.

Within private equity, we encourage caution. The higher interest rate environment discussed previously may provide attractive investing opportunities in fixed income, but conversely it is a headwind for strategies that rely on meaningful leverage to generate returns.

We see a few opportunities within the real assets category; with commercial real estate potentially nearing a turning point, CRE equity represents a diversifying opportunity for insurers. For life insurers in the US, it may be even more compelling in light of the reduced capital charges implemented in recent years. Value-add in particular may be the most attractive opportunity globally to deploy equity capital within real estate. We believe infrastructure will continue to be of keen interest to insurers as another source of diversification and steady cash flow generation, particularly outside the US; of note, some US municipal bonds can now be classified as infrastructure investments by European insurers, offering them a way to access their desired exposure in a more liquid format.

From a regulatory perspective, there are a number of items of interest in 2024. In the U.K., the Prudential Regulation Authority (PRA) continues its work to refine solvency rules, particularly as it relates to annuities. These adjustments should benefit insurers, and hopefully, the broader economy. In continental Europe, any changes are likely to take more time to be implemented, and may not be as business-friendly as those observed in the U.K. In the US, discussion continues on how to appropriately capture the risk within asset-backed security (ABS) residual tranches. While an interim risk-based capital (RBC) charge of 45% has been assessed for life insurers this year, the potential for longer-term changes remains. Regulatory discussions also continue on topics including bond definitions, the role of credit rating agencies in the insurance industry, and the prevalence of insurers owned by alternative asset managers. While definitive answers on many of these questions may not arrive in 2024, we expect significant industry discussion throughout the year with much debate between regulators and carriers.

In summary, we expect 2024 to offer more breadth of opportunities than has been observed for a number of years. This is largely a function of public bond yields being more attractive now than they’ve been in a long time, especially in light of how we expect the economy and central bank policy to unfold. As such, now may be the year for insurers to lock in more duration. But there continue to also be excellent opportunities in select private markets, particularly CRE debt and distressed debt.

Stay up to date with our insurance insights newsletter

Investment Risk Warnings

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.

For Institutional Investor Use Only

Invesco Advisers, Inc. is an investment adviser; it provides investment advisory services to individual and institutional clients and does not sell securities.

Data as of December 29, 2023, unless otherwise stated.

All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This is being provided for informational purposes only, is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in any investment making decision. This should not be considered a recommendation to purchase any in-vestment product. As with all investments there are associated inherent risks. This does not constitute a recommendation of any investment strategy for a particular investor. Investors should consult a financial professional before making any investment decisions if they are uncertain whether an investment is suitable for them. Please read all financial material carefully before investing. Past performance is not indicative of future results. The opinions expressed herein are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.