We recently sat down with Ron Kantowitz, Managing Director and Head of Invesco Private Debt, to review the direct lending landscape in 2023 as well as discuss market observations and themes he sees playing out in 2024.

Ron, looking back how would you characterize the direct lending environment in 2023?

I would characterize 2023 as a year where uncertainty related to macroeconomic conditions, geopolitical events, and the Federal Reserve’s aggressive tightening stance created a challenging environment for M&A activity. Private equity firms were generally more cautious given the “risk-off” sentiment, higher cost of debt and lower leverage levels available to finance new acquisitions. Adding to these challenges was a reluctance on the part of private equity firms to exit investments at lower valuations. As a result, transaction volumes were down, driving fewer opportunities to deploy capital across the direct lending asset class.

Importantly though, while M&A activity was slow, the quality of the deals that were executed was among the most compelling we’ve seen in direct lending. Transactions that did close were underwritten with a clear view of macro risks. In fact, a “recession scenario” was often modelled as the “base case scenario.” With such a high bar, only the strongest credits with conservative capital structures and tight documentation were able to cross the finish line. Further, given the floating rate nature of the asset class, direct lending offered yields of 12 – 13%, unlevered. When compared to historical yields of 7.5 – 8.0%, the 2023 vintage should be viewed as one of the most attractive we’ve seen in the asset class.

The Federal Reserve recently signaled that it will likely proceed with interest rate cuts later this year. How do you see that impacting the return profile of the direct lending asset class?

As the Fed continues to see evidence of moderating inflation, we should expect they will take a more accommodative stance. While the timing and magnitude of their actions remain to be seen, I expect the impact on direct lending yields to be fairly muted this year.

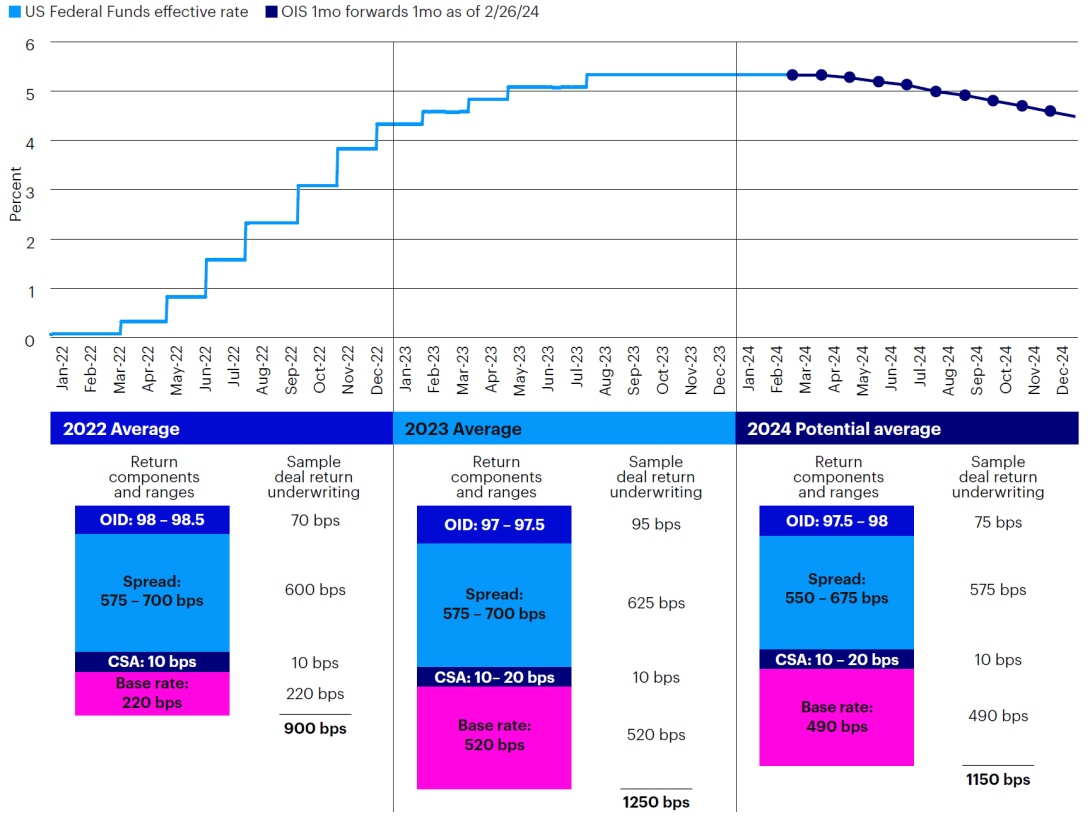

For context, recall that the Fed first started hiking the federal funds rates in March of 2022 and ended the year having raised interest rates seven times. Yet for all of 2022, 3-month SOFR, the floating base rate for direct lending loans, averaged only 2.18%. During 2023, the Fed implemented four additional rate hikes, bringing the average 3-month SOFR for 2023 to 5.17%.

If we assume the Fed cuts three times in 2024, which is currently the consensus view, average 3-month SOFR will pencil out to just under 5.0% this year. That would be well above historical rates and only modestly down compared to 2023.

In addition to SOFR, the other key components of direct lending yields include credit spreads and upfront fees, more commonly known as original issue discounts (“OID”). Should perceived market risks abate during 2024, we anticipate that credit spreads and OIDs will modestly decline and revert to more normalized levels. Obviously, credit risk is specific to each transaction, but more broadly I would expect to see spreads tighten by 25 – 50bps and OID’s tighten from 97.5 to the 98.0 area.

Taking all this into account, we believe the impact on direct lending yields should be fairly muted — with a decline likely in the range of 50 – 100 bps. Under this scenario, direct lending yields should settle in the 11 – 12% area, unlevered. We believe this is still incredibly attractive from a risk/return perspective, and meaningfully higher than the yields direct lending exhibited leading up to the Fed’s tightening cycle.

Historical fed funds rate, implied forward rates1 and direct lending yields (and components)2

1. Source: Bloomberg, as of February 26, 2024.

2. Source: Invesco as of February 26, 2024; as observed and executed upon by Invesco Direct Lending team. ‘CSA’ represents credit spread adjustment. ‘OID’ represents original issue discount. For illustrative purposes only; past performance is not a guarantee of future results. Forward-looking statements are not a guarantee of future results. They involve risks, uncertainties and assumptions. There can be no assurance that actual results will not differ materially from expectations.

It’s well documented that over the last decade, the size and scale of the direct lending market has experienced dramatic growth, with AUM reaching ~$1.6 trillion. No doubt, the attractive risk/return characteristics are at the forefront of investor appetite. But with so much capital and many new entrants in the market, how do you think about increased competition and the impact on the asset class from a yield and structure perspective?

I think it’s important to look through to the different segments within direct lending to understand where capital is being directed, and consequently, where competitive pressures may be impacting the risk/return paradigm.

In our view, much of the capital that has recently come into the asset class has been directed towards a small subset of direct lenders. As these managers have amassed large sums of dry powder, they have transitioned out of middle market in favor of the larger cap segment as a means to satisfy ever increasing deployment targets. While the opportunity to deploy larger sums of capital is available in the large cap segment, these direct lenders must compete not only amongst each other, but also with banking institutions who have historically dominated the space. This dynamic has translated into deals that look less like traditional direct lending and more like broadly syndicated loans, including aggressive capital structures, tighter pricing and weaker terms and documentation (e.g. covenant-lite, PIK Toggles, etc.).

Importantly, the core middle market, where we focus, continues to be relatively insulated from these trends. While there has certainly been a large influx of capital into the core middle market, competitive pressures are far more benign as this segment tends to be more “clubby” and collaborative. You can see this in our yields, tighter documentation, and conservative structures.

Thank you for that Ron. Given all of this perspective, what is your outlook for 2024?

As we look to 2024, our view is that the backdrop supporting a more favorable transaction environment is firmly in place, including better visibility into the macro environment, softening inflationary pressures, potential rate reductions and heightened pressure from LPs for private equity firms to generate realizations and invest in new platform companies. Combined with continued discipline in terms of credit quality and a relatively stable yield environment, we believe 2024 is shaping up to be a compelling opportunity to deploy capital in the direct lending asset class.

About risk

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested. Alternative investment products, including private debt, may involve a higher degree of risk, may engage in leveraging and other speculative investment practices that may increase the risk of investment loss, can be highly illiquid, may not be required to provide periodic pricing or valuation information to investors, may involve complex tax structures and delays in distributing important tax information, are not subject to the same regulatory requirements as mutual portfolios, often charge higher fees which may offset any trading profits, and in many cases the underlying investments are not transparent and are known only to the investment manager. There is often no secondary market for private equity interests, and none is expected to develop. There may be restrictions on transferring interests in such investments.

For Institutional Investor Use Only

Invesco Senior Secured Management, Inc. is an investment adviser; it provides investment advisory services to individuals and institutional clients and does not sell securities.

All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This is being provided for informational purposes only, is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in any investment making decision. This should not be considered a recommendation to purchase any investment product. As with all investments there are associated inherent risks. This does not constitute a recommendation of any investment strategy for a particular investor. Investors should consult a financial professional before making any investment decisions if they are uncertain whether an investment is suitable for them. Please read all financial material carefully before investing. Past performance is not indicative of future results. The opinions expressed herein are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.