The U.S. economy’s resilience amid a high-rate environment is likely to provide a durable catalyst for stocks for the rest of 2024. We explore stock selection ideas in industries where we see the most attractive opportunities in an economy driven by robust and sustainable consumer spending, a healthy banking system, and positive housing market trends. Each of these strengths is likely to become more pronounced given the likelihood of interest-rate cuts later this year, in our view.

While we remain alert to signs of any potential setback in the wake of the U.S. Federal Reserve’s (Fed’s) aggressive interest-rate hikes dating to March 2022, we’ve been among those who continue to believe that the economy will avoid a hard-landing recession—a view that’s been borne out by early 2024 data. With modest rate cuts now appearing to be likely in coming months, it appears that the Fed has succeeded in orchestrating a soft landing while putting inflation on a downward trajectory; any economic deceleration is likely to be shallow and short-lived, in our view. Retail spending has held up well in recent months, indicating that consumers have managed to adjust to the higher borrowing costs resulting from the Fed’s hikes. Businesses also appear to have adapted to higher rates and the labor market has remained solid, with jobs growth exceeding consensus expectations.

Through the rest of 2024, we expect that the economy’s overall trajectory will pick up, driven by a resilient consumer, stable rates, and renewed business confidence. Against this backdrop, we may see an elevated level of economic uncertainty—as well as bouts of market volatility—in a year of heightened geopolitical risks and key elections in the United States and several other major economies.

Key industries to watch through the rest of 2024

While such an environment presents challenges, we believe that it’s well suited to active, bottom-up investment managers who seek to identify opportunities such as security mispricings. A disciplined approach to valuation can be critically important in times like these and, with an eye on this year’s earnings trends, we’re focusing much of our attention on these key industries, where we see an abundance of opportunities:

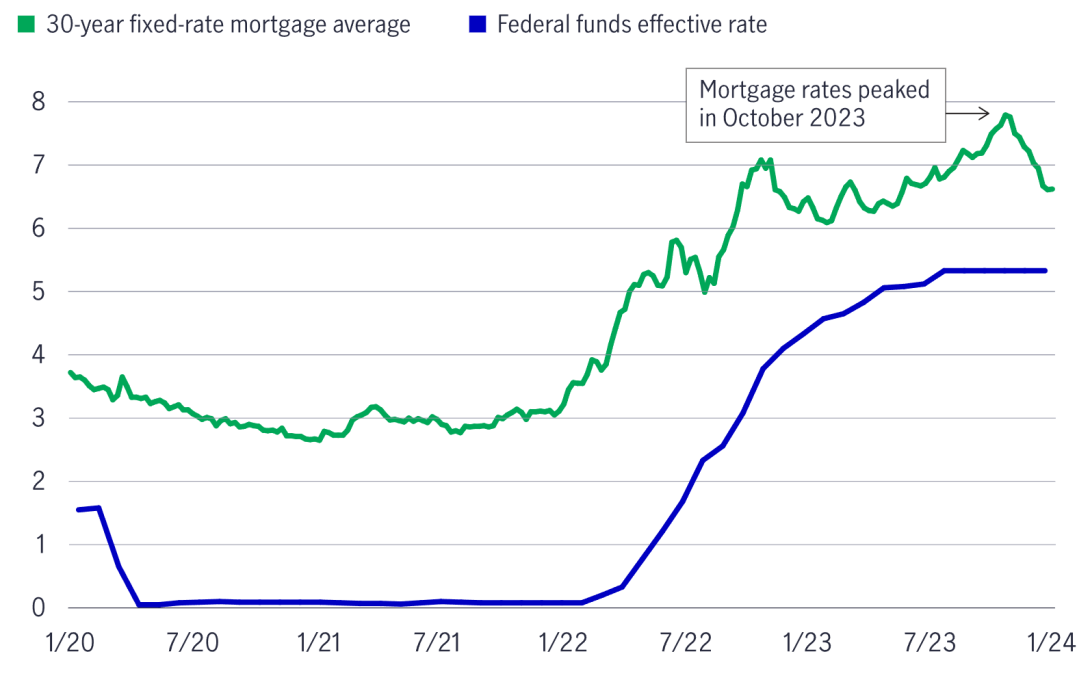

- Homebuilders—This market segment has held up relatively well in our view, considering the negative impact that high mortgage rates have had on home sales and orders for homebuilders. After peaking last October and November, mortgage rates have declined in anticipation of pending rate cuts, which we believe will provide the needed catalyst for prospective homebuyers who have been waiting to get off the sidelines. For builders, we see especially strong growth potential in the many local markets with shortages of affordable housing; many of these markets are starving for more supply. We’ve identified selected builders with strong business fundamentals, such as long-term records of generating steady revenue growth and resilient books of new home orders, even amid the rising inflation and rates of the past couple of years. Some of these names have recently traded at low valuations, providing what we consider to be a margin of safety from an investment perspective when combined with these stocks’ other strengths.

Mortgage rates began falling in late 2023 in anticipation of lower interest rates

30-year fixed-rate mortgage average and the federal funds effective rate, January 2020–January 2024 (%)

Source: U.S. Federal Reserve, Freddie Mac, February 2024. Past performance does not guarantee future results.

- Banks—The banking industry’s growth potential is also tied to the downward trajectory that we believe is ahead for interest rates and the resulting positive impact on mortgage lending activity. While early 2023 saw a small number of banks fail amid a liquidity crunch triggered in part by high rates, those setbacks were limited to a few regional institutions in niche markets. Overall, banks have remained well capitalized, as evidenced by findings from the latest round of annual stress tests conducted by the Fed. For example, all 23 banks required to take the 2023 exam fared better than they had the previous year, with each institution remaining above its minimum capital requirements during a hypothetical recessionary environment. We believe that the industry’s overall health is vastly improved from the state of affairs some 15 years ago, when a global financial crisis—the catalyst that led to the U.S. regulatory requirement mandating the stress tests—was triggered by a wide range of factors, notably undercapitalized banks, an overheated housing market, and excessive consumer debt. Across today’s banking industry, capital markets-sensitive institutions that generate revenue from investment banking are our chief focus from an investment perspective. We see strong current potential for this segment owing to prospects for a rebound in initial public offerings, secondary offerings, and debt issuance following a dry spell over the past couple years.

- E-commerce—On the growth side of the equity style spectrum, select e-commerce companies appear to us to offer attractive combinations of reasonable valuations with strong growth potential. One catalyst for this segment is the recently improved financial health of U.S. middle-class consumers, who account for a 70% share of overall retail spending.1 With wages rising faster than prices since early 2023 and rate cuts likely later this year, e-commerce companies appear to us to be well positioned to capitalize on a potential increase in discretionary spending.

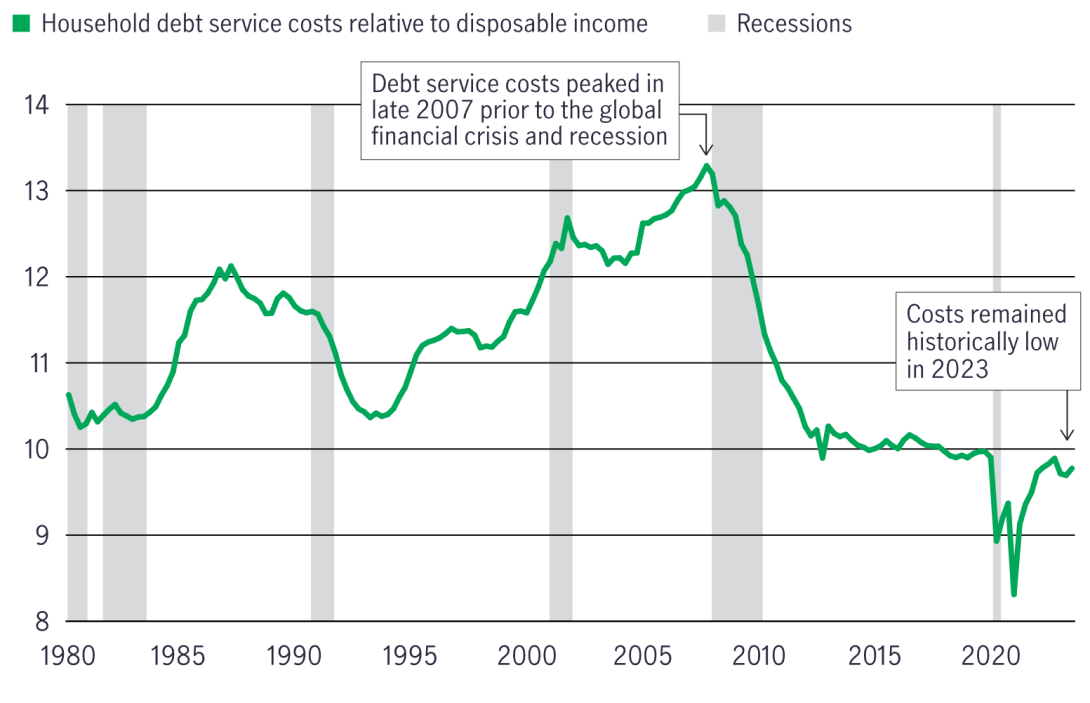

Despite risks, the U.S. consumer outlook has continued to improve

The U.S. economy does face challenges, including a recent rise in consumer debt. However, we view consumer debt loads as manageable, given the improvement in the overall finances that most Americans have experienced in recent years. For example, an October 2023 Fed survey found that American families’ real median net worth surged 37% from 2019 to 2022. Over that period, the share of families with credit card debt remained fairly stable at around 45%, and card debt balances declined. In addition, household debt service costs relative to disposable income have recently remained near the lowest recorded levels dating to 1980—although the ratio has recently edged above the record lows of 2020 and 2021, when government stimulus payments supported consumers during the COVID-19 pandemic.

Consumers' debt costs have remained near their lowest levels in decades

Household debt service costs relative to disposable income, January 1980–June 2023 (%)

Source: U.S. Federal Reserve, January 2024. Recession periods indicated are as defined by the National Bureau of Economic Research. Past performance does not guarantee future results.

Given the potential that we see for earnings growth to pick up through the rest of 2024, we believe that valuations in the three areas above and in other market segments may become more attractive in coming months. In such an environment, we see plenty of opportunities at the individual security level across the equity style spectrum, including value stocks as well as selected growth names.

Going forward, we take comfort in the ongoing health of the consumer, the strength in the job market, record cash levels on the sidelines, strong corporate profitability and balance sheets, and considerable pent-up demand and capital spending plans. We’re trying to maintain a disciplined focus on bottom-up stock picking while emphasizing financially sound companies with competitive advantages, the ability to generate substantial cash flow over sustained periods, and attractive stock prices relative to our estimates of their worth.

1 Empirical Research Partners LLC, 2024.

Important Disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. Mainland China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

3390188