DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

Bond ETFs are increasingly popular tools for insurers looking for exposure to fixed income without worrying about fluctuations in market liquidity. Recent NAIC accounting guidance could make bond ETFs even more attractive to insurers, since it gives them greater clarity over how to treat the instruments.

Over the last six years, some significant regulatory changes have spurred insurance companies’ interest in investing in exchange-traded funds (ETFs) that track bonds. The most recent of these occurred in April 2017, when the National Association of Insurance Commissioners (NAIC) issued accounting guidance providing additional clarity around how insurers could treat some of these ETFs like ordinary bonds.

Bond ETFs have a number of advantages over ordinary bonds. Among them are their resistance to short-term fluctuations in liquidity and potentially lower volatility during financial crises than cash bonds often exhibit. They are also useful for quickly taking exposure to different sectors of the fixed income markets, such as high yield, and can therefore be used to park capital while portfolio managers identify and secure appropriate cash bonds.

Because of these advantages, insurance companies have been allocating more capital to bond ETFs in recent years. In 2016, bond ETF assets held by insurance companies rose 25 percent from previous year. While the absolute figures remain small relative to total industry assets, the rate of growth is notable.

The dynamics of the fixed income markets have changed since the financial crisis. Financial regulation has curbed proprietary trading and has imposed higher capital charges on traditional fixed income liquidity providers (i.e., investment banks). As a result, investors have gravitated toward alternative products for fixed income exposure that are more reliably liquid, in particular, ETFs.

Meanwhile, there has recently been a significant regulatory change that has bolstered insurers’ confidence in these instruments. An example is the decision by the NAIC’s Securities Valuation Office (SVO) to allow some bond ETFs to be treated as bonds, subject to certain conditions. And, over the last half-decade, a large number of bond ETFs have been reviewed by the SVO and included on its designated list of ETFs.

These developments have helped to foster the increase in insurers’ use of these instruments. During 2016, for example, total industry holdings went up from about $15.2 billion to $19 billion. While those are certainly large numbers, these instruments still comprise a very small percentage of the industry’s $5 trillion in total assets.*

The dominant users of ETFs continue to be property casualty companies. They accounted for about 60 percent of the total industry allocation to ETFs, with life insurance companies following up with about 30 percent and health insurers holding the balance.*

Equity ETFs made up 83 percent of the industry’s total ETF assets in 2015, but that percentage declined in 2016 to about 75 percent due to the increased allocation to fixed income ETFs. While bond ETFs were 16 percent of the total at year- end, the proportion has risen to about 23 percent as of year- end 2016.*

The latest rule changes to benefit insurers looking to invest in bond ETFs provided accounting clarity. The NAIC’s Statutory Accounting Principles Working Group approved substantive amendments to SSAP 26R – Bonds during the NAIC’s spring meeting. The amendments were part of reference project 2013-36, which:

These changes were welcome, although hurdles still remain in some states. Our clients use bond ETFs to achieve a variety of goals. Some state codes make it a challenge to construct portfolios entirely out of fixed income ETFs, but we have seen companies use them extensively in jurisdictions with sufficiently permissible state codes. In fact, one company replaced its entire bond portfolio with bond ETFs in order to achieve the exposures it wanted. However, that’s a highly unusual case, and generally state code limits make that approach somewhat challenging.

Short of that, insurance companies are using bond ETFs either to gain exposure to specific sectors, such as high yield, and using ETFs as placeholders to park funds as they work to secure other investments. For example, if a company wants to build or grow an investment grade corporate bond portfolio, and if it has a sudden, large cash flow, it might use a corporate bond ETF as a placeholder while it looks for the cash securities it wants to meet its portfolio needs.

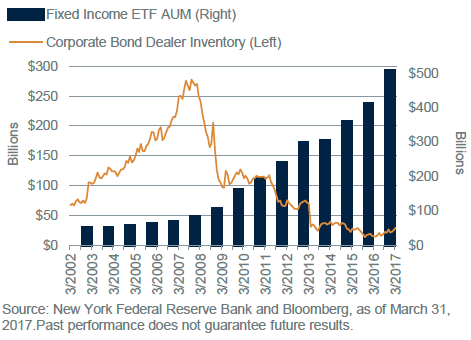

The growth of fixed income ETFs has been remarkable with the first one launched in 2002, almost 10 years after the first equity ETF. By the end of 2006, there were only six products totaling $20.5 billion in assets. In 2007, the SEC approved the requirements for standardized Fixed Income baskets and the generic listing process for fixed income ETFs. Due to these changes, the industry saw an influx of new fixed income ETFs come to market from multiple ETF issuers. This was an opportune timing for what was about to happen next.

During the financial crisis in 2008, broker-dealers pulled back from their cash bond market-making businesses to conserve capital, shed assets and subsequently meet more stringent regulatory capital requirements. These changes reduced inventory of cash bonds, resulting in investors gravitating to alternative products; they discovered ETFs as a way to access the fixed income market. Currently there are 323 fixed income ETFs listed in the US with under $528 billion under management (March 2017). Figure one shows how ETF volumes grew as dealer inventories shrank; primary dealer balances are on the left axis and ETF assets under management since 2002 to March of this year on the right.

ETFs work via a creation/redemption mechanism that allows authorized participants (APs) to manage how a fund expands or contracts as a result of investor demand. In a creation, the AP delivers either cash equities or cash bonds to the fund. In return, the asset manager delivers ETF shares to the AP. In a redemption, the AP delivers ETF shares in exchange for cash equities or cash bonds. Only APs can create or redeem directly with the ETF trust. The key point here is that there are actual, physical securities changing hands.

The creation process for equity ETFs is usually full replication. So, for an S&P 500 ETF, there would be 500 equities delivered for creation or for redemption. Nonetheless, there are differences between equity ETFs and bond ETFs. Fixed income indexes can be much larger and bonds do not trade as continuously as equities.

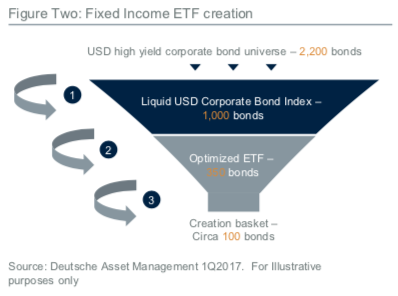

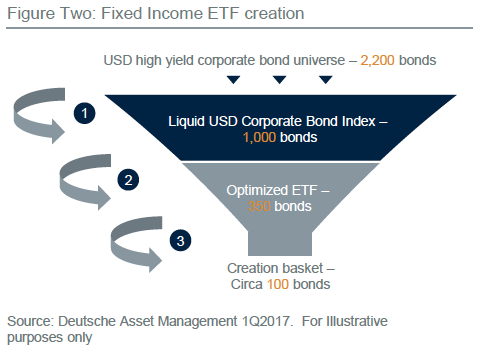

Figure two shows how bond ETF portfolios can be constructed. The U.S. high yield corporate bond universe could contain about 2,200 bonds. The liquid U.S. corporate bond index for an ETF could include 1,000 of these bonds, but the ETF is optimized to include only 350. To create or redeem depending on what bonds are available could only require 100 bonds for delivery. Those 100 bonds would be chosen to be a good representation of the index to track the underlying portfolio.

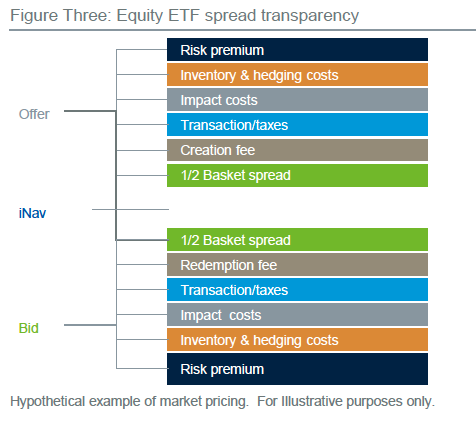

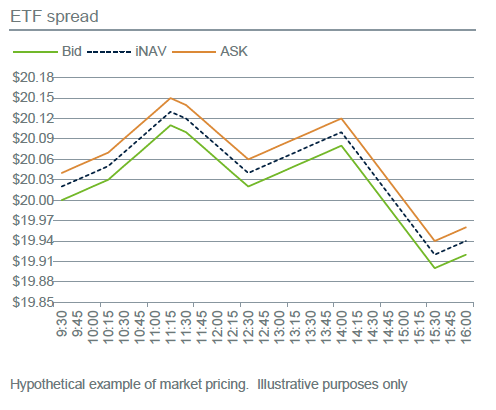

The spreads on equity ETFs are different from those on fixed income ETFs. Figure three shows how an equity ETF onscreen spread reflects the creation and redemption costs. Every ETF has a creation fee. These can range from a few hundred to a few thousand dollars. APs or market makers must pay any transaction fee and applicable taxes when executing the basket of underlying securities.

Impact costs on the underlying securities depending on the size of the trade. Authorized participants or market makers are charged to use their firms’ balance sheets. If they hedge, there is a cost to that, as well as a risk premium. These are all components of the spread in an ETF.

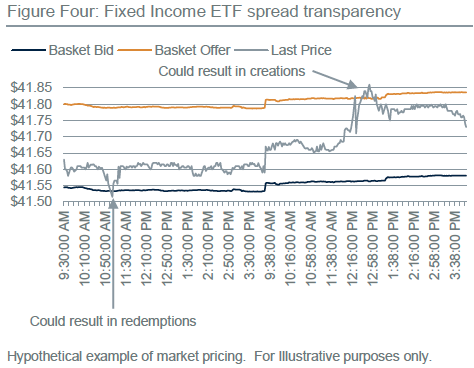

Fixed income is slightly different. Figure four shows the basket bid for a portfolio of bonds (blue) and a basket offer (orange). Since the NAV of fixed income ETFs is either marked to the bid or mid of the underlying cash bonds, fixed income ETFs will generally trade at a premium to reflect the full cost of creation/redemption.

There are four concerns about bond ETFs that are often voiced that have little basis in fact. Putting these myths to rest is important so that insurers considering bond ETFs can make decisions based on the instruments’ merits.

The first is that ETFs trade less during market corrections. In reality, what often happens is that volumes actually pick up two to three times their average daily volume. Since 2002, any time there has been an event or deep market volatility, we have actually seen the volume in the secondary market pick up.

The second concern is that high yield ETFs are moving the markets. In fact, high yield ETFs only represent approximately 4 percent of the high yield cash market (June 2017). Mutual funds make up almost 28 percent. It is important to keep that in perspective. If you think back to December 2015, when the high yield market was under some stress, there were a few mutual funds that had to suspend redemptions. ETFs had no such problem and continued to trade on the secondary market. There were no issues with the creation/redemption processes.

The third concern is that fixed income ETFs are constrained by underlying liquidity. That this is false can be seen every year on Columbus Day, when the equity markets are open but bond markets are closed. Fixed income ETFs trade on the equity exchanges, and on Columbus Day, they trade hundreds of millions of dollars very efficiently. Rather than being constrained by the underlying liquidity, they are additive to that liquidity profile.

The fourth concern is that fixed income ETFs do not have enough cash to meet redemptions. However, fixed income ETFs don’t actually have to have cash to meet redemptions, because they transact in kind, delivering cash bonds rather than cash. Unlike an open ended mutual fund, an ETF manager does not have to sell bonds to raise cash.

With these concerns allayed, insurance companies can focus on determining whether bond ETFs make sense as part of their portfolio strategies, and what degree of latitude their state regulators provide for their use. Given the changes to the traditional cash bond market since the financial crisis, bond ETFs can be useful tools for acquiring fixed income exposures that would otherwise be difficult to achieve.

By Deutsche Asset Management

Contributors

Mike Earley, Head of Client Solutions—Americas

Luke Oliver, Head of ETF Capital Markets—Americas

David Stack, ETF Capital Markets

*Source: SNL Financial based on Dec. 2016 data.

Note: Unlike bonds, exchange-traded funds (ETFs) are subject to greater market risks, including the risk of loss of capital as bonds typically offer the repayment of principal, subject to the creditworthiness of the underlying issuer.

Risk Disclosure: Bond investments are subject to interest-rate and credit risks. When interest rates rise, bond prices generally fall. Credit risk refers to the ability of an issuer to make timely payments of principal and interest. Investing in derivatives entails special risks relating to liquidity, leverage and credit that may reduce returns and/or increased volatility. Investing in foreign securities, particularly those of emerging markets, presents certain risks, such as currency fluctuations, political and economic changes, and market risks.

Deutsche Asset Management is the brand name of the Asset Management division of the Deutsche Bank Group. The respective legal entities offering products or services under the Deutsche Asset Management brand are specified in the respective contracts, sales materials and other product information documents.

For purposes of ERISA and the Department of Labor’s fiduciary rule, we are relying on the sophisticated fiduciary exception in marketing our services and products, and nothing herein is intended as fiduciary or impartial investment advice unless it is provided under an existing mandate.

Confidential. For Professional Clients (MiFID Directive 2004/39/EC Annex II) only. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

“For Institutional investors only. Further distribution of this material is strictly prohibited”

Investments are subject to risk, including possible loss of investment capital.

The material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It is for professional investors only. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for Deutsche Bank AG and its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein.

Please note that this information is not intended to provide tax or legal advice and should not be relied upon as such. Deutsche Asset Management does not provide tax, legal or accounting advice. Please consult with your respective experts before making investment decisions.

Neither Deutsche Bank AG nor any of its affiliates, gives any warranty as to the accuracy, reliability or completeness of information which is contained. Except insofar as liability under any statute cannot be excluded, no member of the Deutsche Bank Group, the Issuer or any officer, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered.

For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

For investors in Switzerland: Deutsche Asset Management Schweiz AG is the asset management arm of Deutsche Bank AG in Switzerland, authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”). This material is intended for information purposes only and does not constitute investment advice or a personal recommendation. This document should not be construed as an offer to sell any investment or service. Furthermore, this document does not constitute the solicitation of an offer to purchase or subscribe for any investment or service in any jurisdiction where, or from any person in respect of whom, such a solicitation of an offer is unlawful. Neither Deutsche Bank AG nor any of its affiliates, gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Past performance or any prediction or forecast is not indicative of future results. The views expressed in this document constitute Deutsche Bank AG or its affiliates’ judgment at the time of issue and are subject to change. Deutsche Bank has no obligation to update, modify or amend this letter or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate, or if research on the subject company is withdrawn. Prices and availability of financial instruments also are subject to change without notice. The information provided in this document is addressed solely to Qualified Investors pursuant to Article 10 paragraph 3 of the Swiss Federal Act on Collective Investment Schemes (CISA) and Article 6 of the Ordinance on Collective Investment Schemes. This document is not a prospectus within the meaning of Articles 1156 and 652a of the Swiss Code of Obligations and may not comply with the information standards required thereunder. This document may not be copied, reproduced, distributed or passed on to others without the prior written consent of Deutsche Bank AG or its affiliates.

For investors in South Korea (based on a reverse solicitation): This material deals with a specific product/investment strategy which is not registered in Korea. Therefore the material can not be used for Korean investors. Only passive communication to respond to a request from a Korean investor is allowed. This material can not be sent to a Korean investor unless the investor requests the material on an unsolicited basis or the investor is an existing client of the product. Also, it may be prudent to have some paper trail which can evidence the fact that the request was made by the investor on an unsolicited basis.

For the UK: Issued and approved by Deutsche Asset Management (UK) Limited of Winchester House, 1 Great Winchester Street, London EC2N 2DB, authorised and regulated by the Financial Conduct Authority (“FCA”).

This document is a “non-retail communication” within the meaning of the FCA’s Rules and is directed only at persons satisfying the FCA’s client categorisation criteria for an eligible counterparty or a professional client. This document is not intended for and should not be relied upon by a retail client. This document may not be reproduced or circulated without written consent of the issuer.`

For investors in Belgium: The information contained herein is only intended for and must only be distributed to institutional and/or professional investors (as defined in the Belgian law of 2 August 2002 on the supervision of the financial sector and the financial services). In reviewing this presentation you confirm that you are such an institutional or professional investor. When making an investment decision, potential investors should rely solely on the final documentation (including the prospectus) relating to the investment or service and not the information contained herein. The investments or services mentioned herein may not be adequate or appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand the transaction and have made an independent assessment of the suitability or appropriatness of the transaction in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such a transaction. You should also consider seeking advice from your own advisers in making the assessment. If you decide to enter into a transaction with us you do so in reliance on your own judgment.

For investors in Hong Kong: This document is issued by Deutsche Bank AG acting through its Hong Kong Branch. Investment involve risks, including possible loss of principal amount invested. Past performance or any prediction or forecast is not indicative of future results. Interests in the investment mentioned in the document may not be offered or sold in Hong Kong, by means of an advertisement, invitation or any other document, other than to Authorized Persons only and as such, is not approved under the Securities and Futures Ordinance (SFO) or the Companies Ordinance and shall not be distributed to non-Authorized Persons in Hong Kong or to anyone in any other jurisdiction in which such distribution is not authorized. This document has not been reviewed by any regulatory authority in Hong Kong. For the purposes of this statement, an “Authorized Person” must be a category (a) to (i) professional investor as defined under the interpretation of Schedule 1 part 1 of the SFO. The distribution of this information may be restricted in certain jurisdictions.

For investors in Japan: This document is prepared by Deutsche Bank A.G. London Branch and is distributed in Japan by Deutsche Securities Inc. (DSI). Please contact the responsible employee of DSI in case you have any question on this document because DSI serves as contacts for the product or service described in this document. This document is for distribution to Professional Investors only under the Financial Instruments and Exchange Law. The term “resident of Japan” means any natural person having his place of domicile or residence in Japan, any corporation or other entity organized under the laws of Japan or having its main office in Japan, or an office in Japan of any corporation or other entity having its main office outside Japan.

For investors in Taiwan: The interests described in this document may be made available for investment outside Taiwan by investors residing in Taiwan, but may not be offered or sold in Taiwan. The interests described in this document are not registered or approved by FSC of Taiwan ROC and could not be offered, distributed or resold to the public in Taiwan. The investment risk borne by unregistered and unapproved interests could cause investors to lose part of or all investment amount. The securities may be made available for purchase outside Taiwan by investors residing in Taiwan, but may not be offered or sold in Taiwan.

This document is intended for discussion purposes only and does not create any legally binding obligations on the part of Deutsche Bank AG and/or its affiliates (“DB”). Without limitation, this document does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for DB to enter into or arrange any type of transaction as a consequence of any information contained herein. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Past performance is not a guarantee of future results. Any forecasts provided herein are based upon our opinion of the market as at this date and are subject to change, dependent on future changes in the market. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. Investments are subject to risks, including possible loss of principal amount invested.

When making an investment decision, potential investors should rely solely on the final documentation relating to the investment or service and not the information contained herein. The investments or services mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand the transaction and have made an independent assessment of the appropriateness of the transaction in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. For general information regarding the nature and risks of the proposed transaction and types of financial instruments please go to https://www.db.com/company/en/risk-disclosures.htm. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with us you do so in reliance on your own judgment.

Certain Deutsche Asset Management products and services may not be available in every region or country for legal or other reasons, and information about these products or services is not directed to those investors residing or located in any such region or country. DB SPECIFICALLY DISCLAIMS ALL LIABILITY FOR ANY DIRECT, INDIRECT, CONSEQUENTIAL OR OTHER LOSSES OR DAMAGES INCLUDING LOSS OF PROFITS INCURRED BY YOU OR ANY THIRD PARTY THAT MAY ARISE FROM ANY RELIANCE ON THIS DOCUMENT OR FOR THE RELIABILITY, ACCURACY, COMPLETENESS OR TIMELINESS THEREOF.

The material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It is for professional investors only. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for Deutsche Bank AG and its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Investment decisions should always be based on the Sales Prospectus, supplemented in each case by the most recent audited annual report and, in addition, by the most recent half-year report, if this report is more recent than the most recently available annual report.

Past performance is not indicative of future results. No representation or warranty is made as to the efficacy of any particular strategy or the actual returns that may be achieved.

Neither Deutsche Bank AG nor any of its affiliates, gives any warranty as to the accuracy, reliability or completeness of information which is contained. Except insofar as liability under any statute cannot be excluded, no member of the Deutsche Bank Group, the Issuer or any officer, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered.

The views expressed constitute Deutsche Bank AG’s or its affiliates’ judgment at the time of issue and are subject to change. Any forecasts provided herein are based upon our opinion of the market as at this date and are subject to change, dependent on future changes in the market. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. Investments are subject to risks, including possible loss of principal amount invested. The value of shares/units and their derived income may fall as well as rise. Past performance or any prediction or forecast is not indicative of future results.

Certain Deutsche Asset Management investment products and services may not be available in every region or country for legal or other reasons, and information about these products or services is not directed to those investors residing or located in any such region or country.

Deutsche Asset Management represents the asset management activities conducted by Deutsche Bank AG or any of its subsidiaries. ©2017. All rights reserved I-051502-1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in