A large and diverse investment universe

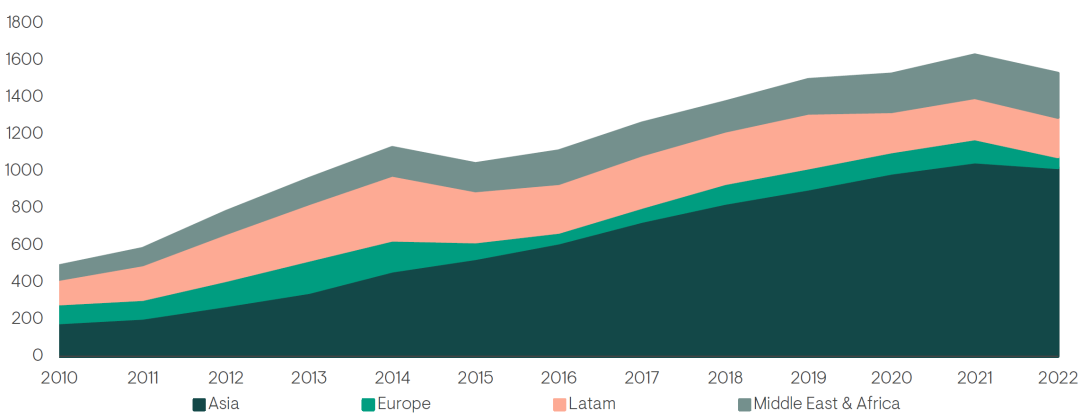

As emerging markets have grown substantially over the past two decades, emerging market-based corporations have turned to international capital markets to help fund and grow their businesses. As a result, JP Morgan launched a suite of emerging market corporate debt indices in 2008. From a market cap of less than US$500 billion in 2010, the investment-grade portion of the entire asset class has grown to c.US$1.6 trillion1 today across 29 countries. While asset class net issuance has turned negative in 2022, this is likely a shorter-term phenomenon and the actual path of growth is likely to continue.

The investment universe is diversified globally across regions, countries, and sectors, with lower leverage than comparably rated developed market peers. We believe this fast-growing and increasingly diverse asset class – which has higher yields, lower duration and less leverage than US investment-grade debt for comparable credit quality – could provide a high-grade complementary solution for institutional investors.

Fig 1. Growth in EM IG corporate bonds (US dollar, billion)

Source: Ninety One, JP Morgan, as at 31 August 2022. All comparative data for EM Investment Grade Corporate asset class is based on the JPMorgan Investment Grade CEMBI Broad Diversified Index and Bloomberg Barclays US Aggregate Index for the US Aggregate Index unless stated otherwise. For further information on indices, please see the important information section.

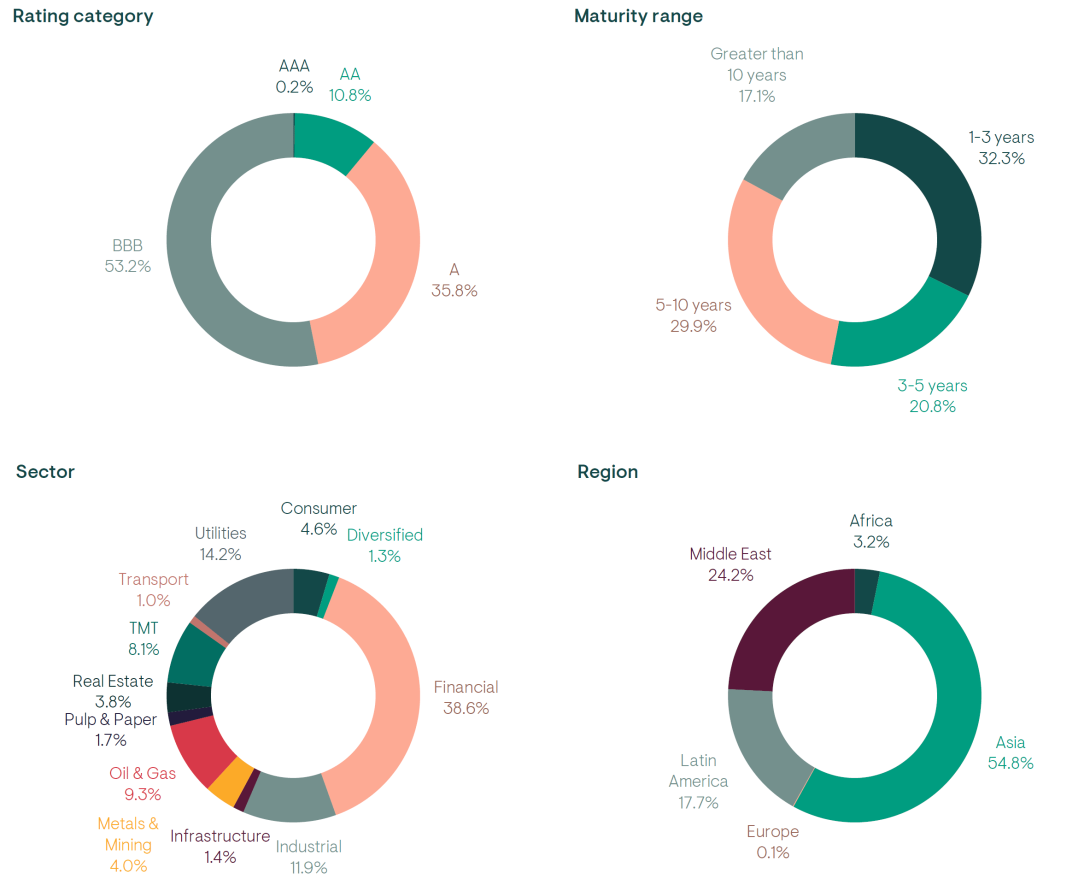

There are now over 1,200 bonds in the JP Morgan CEMBI IG alone, issued by over 400 companies from a range of sectors. From an industry perspective, commodity and financial companies make up around half of the market, but that proportion has decreased over time as the market has grown and become more diversified. Maturities extend from less than a year to over 30 years, providing plenty of choice, including relative-value opportunities within individual issuers’ yield curves.

Fig 2. JPMorgan CEMBI IG rating, maturity, sector and regional breakdown

Source: Ninety One, JP Morgan as at 31 October 2022.

Fundamentally strong companies

Through time, emerging market companies have on average maintained better credit fundamentals than their similarly rated developed market peers, as they have needed to maintain resilience during times of challenging macroeconomic backdrops.

Head-quartered and operating in emerging markets, these companies are familiar with volatility and have historically experienced periods when they struggled to finance themselves with longer-term debt. Thus, their short-term debt is higher as a percentage than it is in developed markets, and their refinancing risks have historically been higher. This has led to a culture of retaining cash while containing leverage. This has been particularly evident since the COVID-19 crisis, as many companies have pared back their expansion and capital expenditure, leaving them with healthy cash balances and strong buffers.

While higher refinancing risks would typically be a fundamental challenge in a rising rate environment – as there is a need to refinance at higher costs – such pressure on EM corporates is meaningfully lower in this cycle relative to prior cycles as most issuers have been able to pre-finance in the ultra-low interest rate regime of the past three years. This has left them well-placed from a financing perspective over the short and medium term.

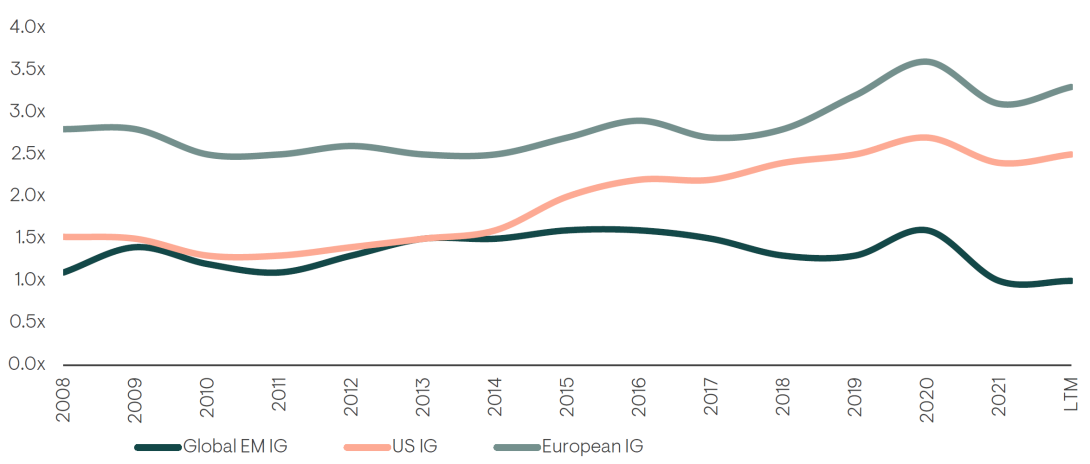

Fig 3. EM vs. US and European IG net leverage comparison

Source: JP Morgan as at 30 June 2022. *LTM = Last twelve months.

For further information on indices, please see the important information section.

The EM ‘zip-code’ premium

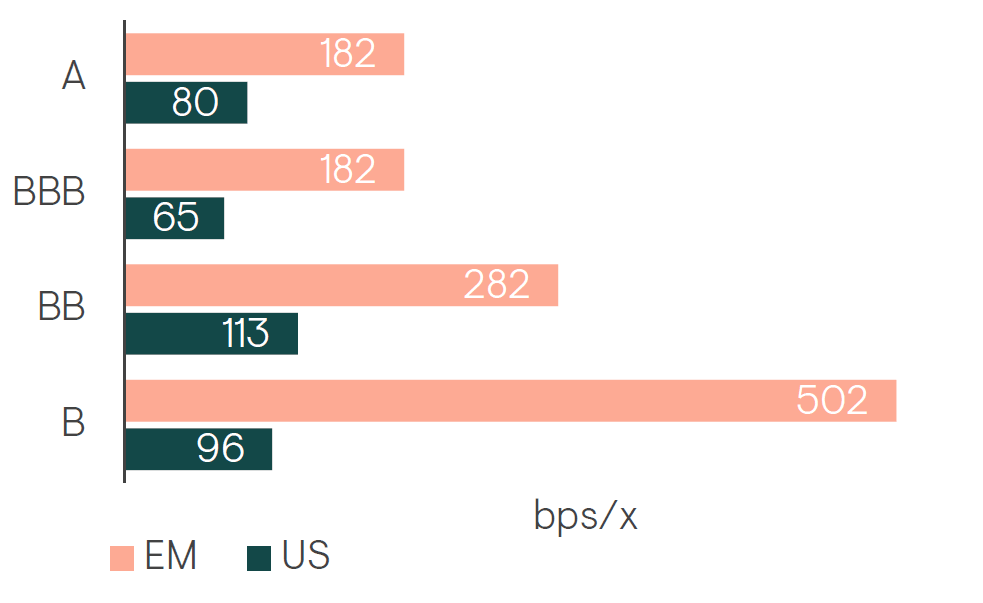

Investors often perceive emerging market companies to be riskier because of their domestic operating environments. Although rating agencies account for this, premiums still exist for EM companies with better credit metrics than developed market peers; in effect, a ‘zip-code premium’. Figure 5 shows this by comparing the spread-per-turn of leverage offered by emerging and developed market companies.

EM company financial strength has led to many improving credit stories, but sovereign credit deterioration/policy shifts have stymied some positive ratings actions and led to downgrades of corporates in some instances. EM companies retain access to multiple financing sources such as equity, local currency bonds and loans, yet many are capped by the rating of their governments; despite the superior fundamentals, their geography effectively drags down the rating. This creates compelling valuation opportunities for investors.

The temporary spike in leverage seen by EM companies in 2020 has reversed. Net leverage remains lower than it is in the US across rating buckets, and deleveraging through 2021 and beyond has resulted in many EM companies’ leverage metrics reaching multi-year lows.

Fig 4. EM Corporates exhibit lower level of leverage than US across most rating buckets

Source: Spreads as at 30 September 2022, BoA Merrill Lynch. Net Leverage as at Q4 2021.

Source: Spreads as at 30 September 2022, BoA Merrill Lynch. Net Leverage as at Q4 2021.

Fig 5. Spread per turn of net leverage

Source: Spreads as at 30 September 2022, BoA Merrill Lynch. Net Leverage as at Q4 2021.

1 JP Morgan, as at 31 March 2022.

Read the full article here

Author

Victoria Harling

Head of Emerging Market Corporate Debt

Victoria is Head of Emerging Market Corporate Debt and is responsible for managing the Emerging Market Corporate Debt Strategy and the Emerging Market Investment Grade Corporate Debt Strategy at Ninety One. Victoria joined Ninety One in 2011 from Nomura International. Victoria previously spent over three years working with emerging market trading desks and capital markets teams for Standard Bank and Nomura. She also spent two years running hedge fund and proprietary trading strategies for Rand Merchant Bank and Whitebeam Capital Management. Prior to this, Victoria spent over eight years working for Henderson Global Investors where she was responsible for running emerging market debt portfolios. Victoria graduated from Leeds University with a Bachelor of Science degree in Biochemistry with Molecular Biology. In addition, she has passed CFA® Level III.