Emerging markets have long taken a back seat to U.S. investment grade credit in insurance company portfolios. Insurance companies are in many ways the ideal investors for emerging market fixed income, but lower credit ratings, higher volatility and insurers’ limits on foreign exposure have deterred most from allocating dedicated capital to the sector. However, these dynamics may be changing, and we believe now is the time for insurance companies to consider adding emerging market fixed income to their strategic asset allocation. First and foremost for insurers, strong fundamentals have lifted credit quality overall in emerging markets. Today, over half of the JP Morgan EMBI Global Diversified Index (by market capitalization) is investment grade. So insurance companies can now invest in many EM assets without holding more regulatory capital than for investment grade credit. We see several other reasons for insurers to consider adding EM fixed income to their portfolios.

1. ATTRACTIVE VALUATIONS:

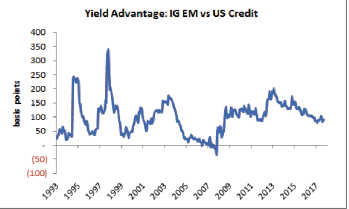

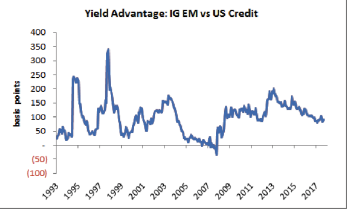

High-grade EM sovereign bonds offer a meaningful pickup in yield versus U.S. investment grade corporate credit. Figure 1 shows the historically higher yield for the investment grade component of the EMBI Global Diversified Index versus the Bloomberg Barclays U.S. Credit Index. Moreover, the yield on the EMBI Global Diversified is nearing 5%, which has tended to be an attractive entry point since 2008 and would potentially allow insurers to lock in the high book yields that are so valuable for accounting purposes.

Figure 1: Yield advantage: Investment grade emerging market sovereign bonds have historically topped U.S. investment grade credit

Source: JP Morgan and Bloomberg, 30 September 2018 | Past performance is not a guarantee or a reliable indicator of future results.

2. DIVERSIFICATION:

The correlation of investment grade emerging market sovereign bonds (measured by the EMBI Global Diversified Index as of 30 September) to U.S. Treasury bonds is appreciably lower than that of U.S. investment grade credit to Treasuries, so emerging markets can provide diversification within a portfolio. Even a modest allocation to emerging markets could help raise overall portfolio efficiency.

3. EXPOSURE TO CORPORATES:

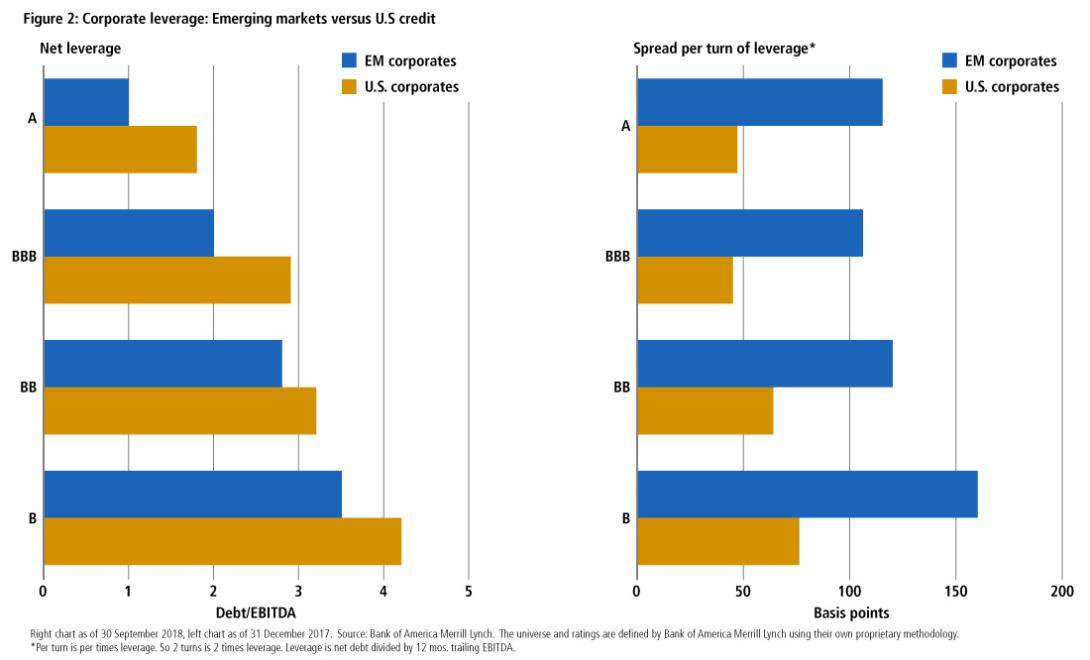

Many investors are surprised to hear how vibrant the EM corporate space is: At $2.5 trillion, it offers an increasingly diverse cross-section of countries, industries, tenors and credit quality. Perhaps even more surprising is the lower leverage for EM companies versus those in the U.S. - and the higher spreads in EM for each unit of leverage, as shown in Figure 2. Assuming ratings are accurately reflecting creditworthiness, the charts together suggest some EM corporate bonds may be less risky and compensate investors more handsomely for the risk taken.

Figure 2: Corporate leverage: Emerging markets versus U.S credit

Right chart as of 30 September 2018, left chart as of 31 December 2017 Source: Bank of America Merrill Lynch | The universe and ratings are defined by Bank of America Merrill Lynch using their own proprietary methodology. | *Per turn is per times leverage. So 2 turns is 2 times leverage. Leverage is net debt divided by 12 mos. trailing EBITDA

TACTICAL OPPORTUNITIES:

Emerging markets’ appeal rests partly on the expectation of credit quality improvement. For investors who can look beyond the high-grade space, emerging markets frequently present opportunities to take tactical exposure in anticipation of credit rating upgrades. For insurance investors who have the flexibility to hold a portion of their portfolio in high yield, EM high yield bonds may be a way to add not only diversification but also yield to the portfolio. Similarly, local bond markets may merit consideration, especially considering their current combination of local currency valuations and high yields, which are attractive, in our view.

NAVIGATING THE RISKS IN EMERGING MARKETS

The volatility in the investment grade portion of the emerging market sovereign bond sector is still around 200 basis points higher than U.S. investment grade credit on average, so the two are not perfectly fungible. Emerging markets overall are a highly diverse group of countries with idiosyncratic risks, and stringent risk management is crucial for investors.

We think active management that draws on deep emerging markets expertise and credit research to choose countries, companies and specific bonds is also critical to navigating the risks and taking full advantage of the opportunities.

A GOOD MATCH

For insurance companies with long-dated liabilities emerging markets pairs well, with the sector’s duration of nearly eight years (as proxied by the EMBI Global Diversified). In addition, emerging markets can be a less liquid asset class. Buy-and-hold insurance investors, with relatively low liquidity needs and longer time horizons, may be well suited to benefit from the higher liquidity premiums found in emerging markets. For the same reasons, they can be well positioned to weather the periodic volatility and downdrafts in the asset class.

For insurers seeking attractive yield, strong credit quality and diversification, this may be an opportune time to consider an investment in high-grade emerging markets.

By PIMCO

Christopher T. Getter, Emerging Market Strategist

Mary Anne Guediguian, Account Manager, Financial Institutions Group

Past performance is not a guarantee or a reliable indicator of future results.

Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Sovereign securities are generally backed by the issuing government. The use of leverage may cause a portfolio to liquidate positions when it may not be advantageous to do so to satisfy its obligations or to meet segregation requirements. Leverage, including borrowing, may cause a portfolio to be more volatile than if the portfolio had not been leveraged. Diversification does not ensure against loss.

The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio. The correlation of various indexes or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially in the future or over different time periods that can result in greater volatility. It is not possible to invest directly in an unmanaged index.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2018, PIMCO.

CMR2018-1018-360178

Download PDF Reprint