Environmental, social and governance (ESG) matters have transitioned from an infrequent and standalone set of considerations into numerous pervasive, highly complex issues for corporations, government entities and investors of all sizes. The implications of ESG matters are already influencing decisions on investments, consumption, regulation and legislation. We believe the ESG phenomenon has created interconnectedness across the global economy that will play a major role in the next 20 years.

KEY TAKEAWAYS

We believe insurers must consider ESG impacts on their assets and liabilities.

In our view, customized solutions are needed to navigate ESG while balancing enterprise risk and meeting yield targets.

Our insurance solutions team takes a data-driven, research- informed approach to building ESG portfolios. This includes proprietary ESG ratings and technology support, engagement, screens and custom reporting.

INTERCONNECTIONS ACROSS THE GLOBAL ECONOMY

Insurers’ Complex ESG Profiles

Insurers are in a unique position as they carefully evaluate the impact and interrelation of ESG impacts on both the asset and liability sides of their balance sheets. Consider property and casualty (P&C) insurers that are experiencing increases in loss frequency and the severity of shifts in climate and weather events in geographies where they have investment dollars placed. Health insurers are contending with societal pressures that are increasing demands for equitable coverage at cost levels that are more accessible to the broader population. They are also being encouraged to invest in their coverage areas to deliver these services. Life insurers price long-tail liabilities that could have altered experience outcomes based on shifts in climate patterns and emergence of new diseases. This may be concurrent with losses on their investment portfolios that are highly exposed to the very same ESG factors. In addition, insurers remain committed to enhancing equity, diversity, influencing long-term health and economic growth. Insurance company boards of directors are tasked with navigating this multi- faceted ESG environment at the enterprise risk level while continuing to provide profitable products and investments that generate sufficient income or return levels. Insurance portfolios have long been customized, and these needs are only increasing as insurers look to their portfolios to provide the greatest potential for meeting their income goals while delivering on new and shifting ESG demands. We believe that each insurer is on its own distinct ESG journey, and Loomis Sayles can play an important role in this journey.

Need for Customization

As awareness of ESG matters has grown, investors have become more attuned to their complexity, the inherent ratings dispersions among issuers and the likely benefits of taking a focused, customized approach. To address these dynamics effectively, it is essential to understand the impact of material ESG factors on investment performance. Insurers looking for ESG solutions typically approach Loomis Sayles in two ways. Some define their specific ESG expectations, while others seek our input to help identify and evaluate the material ESG factors to include in their investment solutions. In either instance, we can help our clients understand the potential portfolio impacts of their decisions. Our analysts’ ESG ratings, supported by Loomis Sayles’ proprietary ESG tools, enable us to create custom portfolios that move clients closer to their ESG goals. In terms of scope, insurance investors can realistically take a holistic approach that addresses a spectrum of ESG issues to improve a portfolio’s ESG footprint. However, we recognize that some insurers may target a specific area of environmental, social and governance challenges, including affordable housing, education, social equity, gender equality and clean energy, to name a few. Our proprietary portfolio construction platform allows us to target a wide array of ESG factors and consider risk-return tradeoffs when building portfolios.

Do you have to Sacrifice Alpha Opportunities?

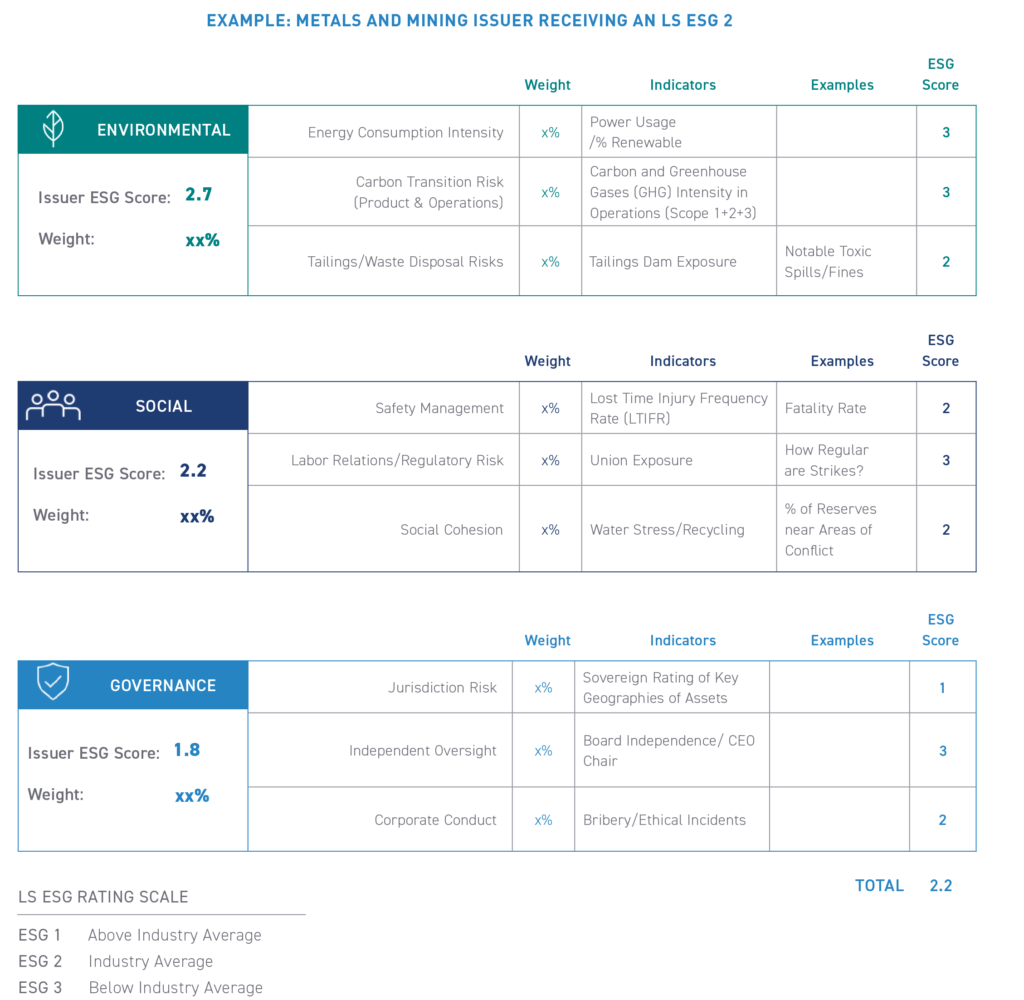

There is a common misconception that investing in issues with high ESG scores involves sacrificing alpha. We would argue that while some sectors or companies screened out by ESG indicators may seem to offer relative upside, they may also carry higher long-term risk from ESG factors (e.g., litigation risks related to environmental harm, labor retention issues or impact of irresponsible suppliers). To assess the most likely outcome, our credit research analysts carefully construct “materiality maps” for their coverage sectors. These tools focus on the ESG factors and sub-factors with the greatest potential to impact an industry, including adjusted weightings for specific ESG factors to reflect their relative importance. In the end, our credit research analysts evaluate each issuer they follow against its industry materiality map and assign a Loomis Sayles ESG score of 1 (above industry average) to 3 (below industry average), as shown in the sample map below. Using Loomis Sayles’ proprietary relative value tools, we can analyze alpha opportunities through an ESG lens. We are also able to filter preferred names that, in our assessment, add an absolute and relative ESG advantage.

Source: Loomis Sayles

Necessary Tools for a Thorough and Thoughtful Appraisal: Negative Screens, Positive Screens and Engagement

Screens — both negative and positive — and engagement are tools in our toolkit as we build custom ESG solutions for clients. We believe it is critical for clients to understand the advantages and disadvantages of each to ensure proper alignment with their ESG goals.

Negative Screens

Loomis Sayles has deep experience implementing negative screens. They can be applied broadly and have been in place for decades for socially responsible investing. Negative screens can exclude issues based on a variety of criteria. For example, some insurers have a specific restricted list that takes into account existing underwriting exposure. Negative screens are binary and do not consider positive momentum in companies that are improving their ESG footprints through active efforts. Comprehensive negative screens can lead to large-scale sector exclusions, which can reduce diversification and limit return opportunities. As a means of influence, they have the potential to curtail capital from going to offenders of beneficial ESG conduct.

Positive Screens

Proactive screens can identify industry leaders incorporating ESG factors or those pioneering innovative solutions. This approach seeks to reward and empower ESG leaders. Given that companies that score higher with respect to ESG actions tend to outperform peers, positive screens may also give an opportunity to tilt the portfolio toward winners. Positive screens need clear goal specification and require greater involvement from asset managers to identify ESG industry leaders and those with positive momentum. Loomis Sayles relies on internal as well as external data to determine longer term trends in firms’ attention and commitment to ESG matters. Our credit research team’s deep issuer knowledge, ongoing dialogue with management teams and their proprietary industry materiality maps enable us to identify companies taking material steps to improve their ESG profiles. This screen type may need frequent updates as definitions of industry leaders and assessment criteria change.

Engagement

Engagement between investors and companies can create positive, influential communication that leads to sustainable, positive changes. This approach requires continued commitment by investors, evaluations of changes implemented and continuous dialogue focused on innovation. In contrast to negative and positive screens, it is more difficult to track engagement and use it to inform portfolio construction. Loomis Sayles has a proprietary ESG engagement database for tracking engagement across asset classes for ESG factors. Started in 2016, the system documents detailed analyst comments about company meetings and engagement on specific ESG factors. This can provide valuable insights into a company’s ESG momentum and can influence the investment team’s decision making.

Summary

Our goal in managing insurance assets is to create balanced and resilient portfolios that can evolve in terms of construction and risk management. We do this using a data-driven and research-informed approach, sensitive to different ESG implications by region and asset class. Sophisticated tools enable us to monitor valuations and relative value through the intersection of fundamental credit quality and ESG factors. We believe our clients can benefit from the insightful ESG-related reporting we provide.

Disclosure

This paper is provided for informational purposes only and should not be construed as investment advice. Opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Other industry analysts and investment personnel may have different views and opinions. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted, and actual results will be different. The charts presented above are shown for illustrative purposes only and used with permission from Bloomberg Finance L.P. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice. Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.Examples above are provided to illustrate the investment process for the strategy used by Loomis Sayles and should not be considered recommendations for action by investors. They may not be representative of the strategy's current or future investments and they have not been selected based on performance. Loomis Sayles makes no representation that they have had a positive or negative return during the holding period.Past performance is no guarantee of, and not necessarily indicative of, future results.LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office. MALR028187

Authors

Pramila Agrawal, PhD, CFA VP, Director of Custom Income Strategies

Erik Troutman, CFA, FSA, MAAA VP, Insurance Strategist

Sean Saia, CFA VP, Investment Director

Colin Dowdall, CFA VP, Director of Insurance Solutions