- The growth trajectory of the U.S. economy exceeds its preCOVID path, and we continue to believe real estate investors should consider modestly higher risk/return strategies.

- We believe the commercial real estate sector is uniquely suited to benefit from current monetary policy, which may allow for higher inflation.

- Out of favor property types including retail, office, and hotel may offer attractive relative value today, and should not be ignored by investors seeking a diversified portfolio.

Introduction

We believe the U.S. economy is on a strong growth path, with GDP on track to exceed its pre-COVID trajectory. Specifically, had the COVID-19 pandemic never occurred, the Congressional Budget Office estimated in 2019 that 2021 U.S. GDP would have been $19.9 trillion1, but today we expect the year to finish at $20.0 trillion. If realized, this will be the first post-WW2 economic recovery where the size of the economy grows above the pre-recessionary trend in the year following the end of the recession. While the late summer and early fall months have continued to exemplify strong economic growth, they also brought risks, with rapid spread of the highly contagious COVID Delta variant, as well as some concern regarding the prospects of economic turmoil faced by several major Chinese property developers. Nonetheless, we remain positive on the economic outlook, and forecast 5.5% GDP growth for 2021. As a result, when considered alongside our analysis of current market pricing that we will outline later in the report, we believe real estate offers attractive relative value, and that investors may benefit from higher risk, and modestly higher yielding real estate investments.

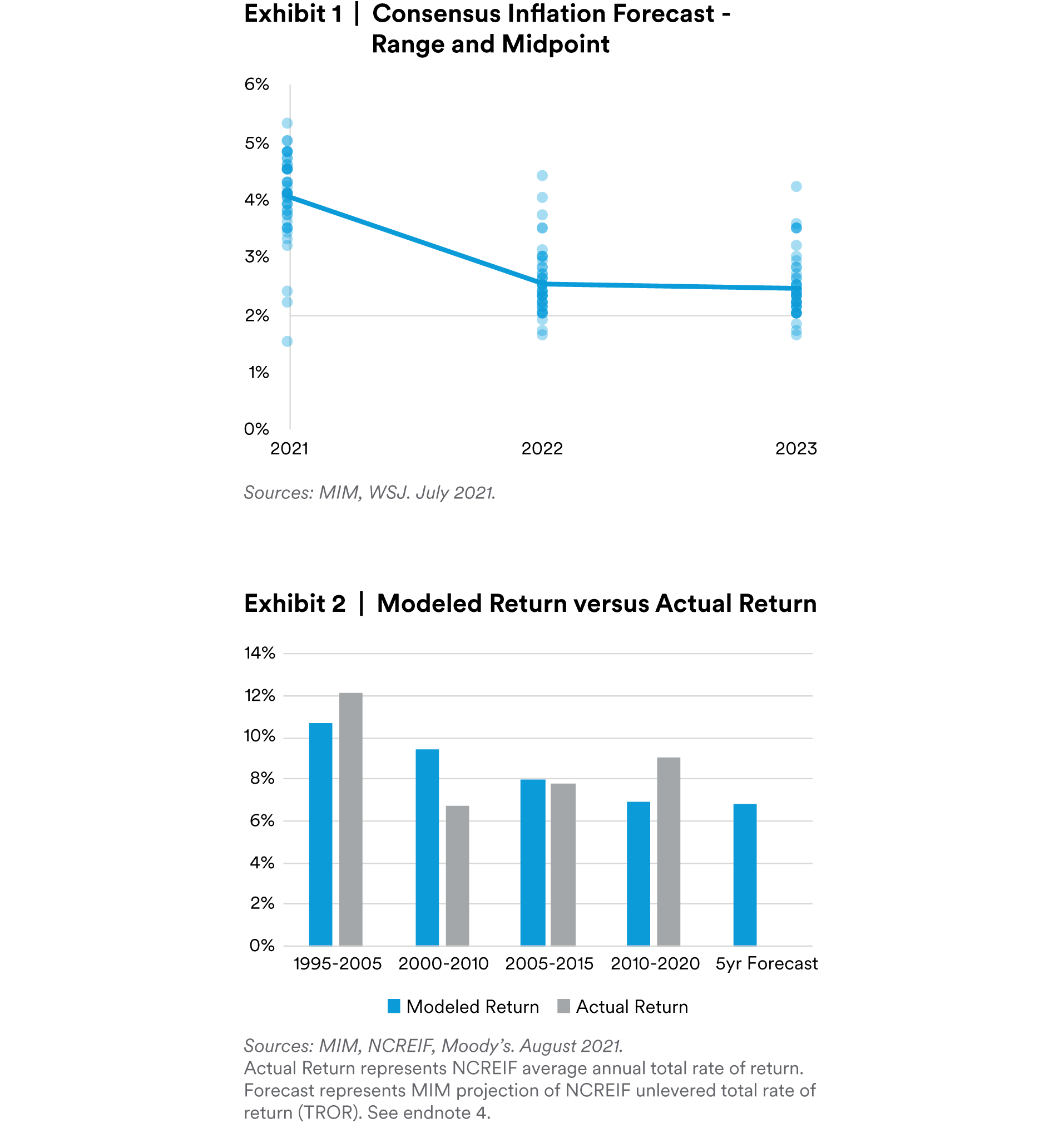

Made-for-CRE Monetary Policy

Although some segments of commercial real estate were squarely in the crosshairs of the COVID-19 impact, we believe the sector may be uniquely suited for current economic conditions. Namely, the economy is in a not-often-seen position where inflation is increasing while interest rates and yields across investment sectors have remained low. Real estate prices have historically benefitted from both low interest rates and rising inflation. Usually, these two conditions do not occur at the same time. We believe the fact that this is occurring simultaneously today exemplifies the Fed’s 2020 updated policy guidance allowing inflation to exceed their 2% target (even when the economy is in a rapid growth mode). The Fed itself is forecasting above 2% inflation all the way through its forecast horizon (2024), and as evidenced in exhibit 1, expectations among market participants appear to be anchored in that range. Although our base case view is not that inflation will run significantly above the 2% target, the possibility of a bout of sustained 3% or higher inflation has grown.

Download PDF

Endnotes

1 2019 CBO estimate.

2 Discussion of real estate returns represents gross unlevered returns as measured by NCREIF. Gross returns will be reduced by costs and expenses, including management fees, and do not reflect, even on a hypothetical basis, net returns resulting from the reduction of these costs and expenses.

3 Moody’s Analytics, 3Q21.

4 The index returns shown herein are for illustrative purposes only, and do not reflect actual historical trading results for any product or investment strategy, and are not a guarantee of future performance. Hypothetical results are subject to various modeling assumptions, statistical variances and interpretational differences. No representations are made as to the reasonableness of the assumptions used and any change in these assumptions would have a material impact on the hypothetical performance results portrayed. Hypothetical results have other limitations including: they do not reflect actual trading and therefore don’t reflect the impact that actual market conditions may have had on the investment manager’s decision making process; regulatory or tax rules that may have existed during the periods modeled; and it also does not take into account an investor’s ability to withstand losses in a down market and assumes the strategy was continuously invested throughout the periods modeled. There is no guarantee that any actual product or strategy that followed any of the hypothetical portfolios modeled herein would have had similar performance. A decision to invest in an investment strategy should not be based off of hypothetical or simulated performance.

5 Moody’s Intermediate-Term Bond Yield Average: Corporate - Rated Baa - Bonds with Seven-year Average Maturities, NCREIF. 3Q21.

6 CoStar, 3Q21.

7 CoStar, MIM. 3Q21.

8 NCREIF, Moody’s. 3Q21.

9 Ibid.

10 CoStar/STR, 3Q21.

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor. This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address Level 34 One Canada Square London E14 5AA United Kingdom. This document is only intended for, and may only be distributed to, investors in the EEA who qualify as a Professional Client as defined under the EEA’s Markets in Financial Instruments Directive, as implemented in the relevant EEA jurisdiction. The investment strategy described herein is intended to be structured as an investment management agreement between MIML (or its affiliates, as the case may be) and a client, although alternative structures more suitable for a particular client can be discussed.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), a registered Financial Instruments Business Operator (“FIBO”).

For Investors in Hong Kong: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”).

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC.