Two of the most important economic questions right now are how high the unemployment rate will rise, and how fast inflation will fall. We see a particularly uncertain economic path forward, and so we have constructed four scenarios for year-end 2023 around these two economic indicators.

As the most likely outcome, we expect a reduction in inflation combined with elevated unemployment.1 However, other scenarios have a greater-than-usual chance of taking place and warrant a closer look.

Table 1 | Probabilities by Scenario

| Core PCE y/y by Q4 2023 |

|---|

| At or below 3% | Above 3% |

|---|

| Maximum unemployment rate 2023 | At or below 4.5% | 20%

Soft landing | 10%

High inflation |

|---|

| Above 4.5% | 55%

Ordinary recession | 15%

Stagflation recession |

Ordinary Recession

We consider this to be the most likely outcome. We believe the Fed when it expresses its commitment to lowering inflation. Inflation has been stubborn this year, and while there is no guarantee that the Fed will be able to reduce inflation down to 2%, we do expect that the Fed’s efforts are likely to lead to sub-3% core PCE growth.

At the same time, this effort is likely to entail raising the Fed Funds rates even higher than it currently is to sufficiently reduce demand. Demand reduction to the level required may ultimately only be achieved by increasing the unemployment rate to recessionary levels.

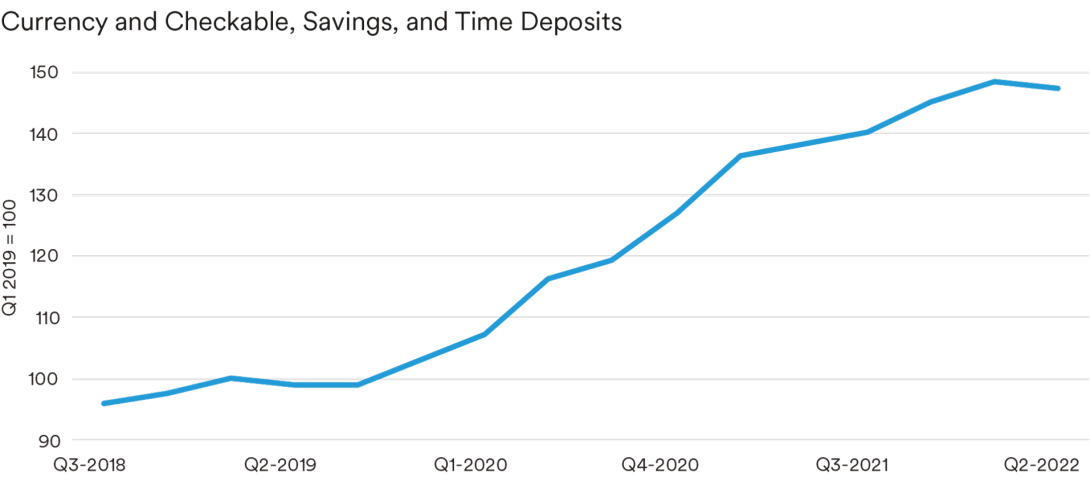

Consumers still have a lot of money saved up. Figure 1 shows households’ liquid holdings (cash, checking, savings).

Normalized against Q1 2019, holdings peaked in Q1 2022 but are still nearly 50% higher than they were pre-COVID-19.2 To counter this huge consumer war chest, the Fed appears to need to create income insecurity by pushing toward higher unemployment – i.e., recession.

This type of recession would be consistent with a continued tight monetary policy. It is particularly likely in cases where the Fed continues to raise rates despite the known lagged effect of the Fed Funds rate on inflation. It is also more likely in cases where the Fed maintains a tight monetary policy for an extended period of time.

Figure 1 | Household Liquid Holdings Nearly 50% Higher Than Pre-COVID Levels

Source: Federal Reserve Board, Haver, MIM

Soft Landing

We feel that a soft landing is substantially less likely than an outright recession, but we see it as the second most likely outcome. A soft landing would require the Fed to do a Goldilocks: raise rates by just enough to rein in inflation but not enough to trigger a recession.

This balancing act will be difficult. The unemployment rate tends to have a tipping point where it suddenly shoots up once economic conditions deteriorate, as all companies seem to tighten their belts at once.

If the Fed does achieve a soft landing rather than a recession, it will likely be a result of luck— getting the level of monetary policy tightness just right, while experiencing no further inflation shocks.

Stagflation

Although stagflation has been much discussed, we believe this may be because the only inflationary episode in most Americans’ living memory was the 1970s stagflationary episode. Most Americans have not lived through an “ordinary” inflationary episode.

The Fed has repeatedly said it is determined to subordinate its employment mandate to its inflation mandate in the near term as it seeks to get inflation under control. With long-run inflation expectations well anchored, as seen by both consumer sentiment surveys and market indicators of inflation expectations, we expect the Fed to succeed in taming inflation.

Therefore, the most likely situation in which inflation would not be well contained by the end of the 2023 is if there is some exogenous shock such as another oil shock, a natural or man-made disaster that affects critical resources, or a military escalation. Acute shortages, well beyond what are currently expected, where it may not be viable for the Fed to respond with a commensurate reduction in demand, may result in stagflation.

More prosaically, it is also possible that inflation heads in the right direction, but that it falls below 3% in early 2024, just missing our year-end 2023 call.

Continued High Inflation

The least likely scenario, in our view, is a continuation of the current situation: high inflation and low unemployment. The Fed is actively trying to shift the economy from the current situation with the most rapidly tightening financial conditions in a generation. It’s quite unlikely that this rapid tightening will have no material effect on the macroeconomic landscape, even if it takes months for its effects to be broadly felt. Even now, a fair number of goods are already seeing outright deflation. The most likely way in which we could wind up in this scenario by year-end 2023 is if there is an unlikely combination of events—say, the beginnings of a soft landing combined with an exogenous shock that reignites inflation.

Conclusion

The next few FOMC meetings are likely to be particularly crucial toward determining which of these scenarios is likely to take place. The Fed’s continued decisive action should have the benefit of substantially reducing the likelihood of prolonged inflation but will most likely lead to recession.

Endnotes

1 High unemployment and recessions tend to occur at the same time. The unemployment rate of 4.5% is taken as a threshold point as it more than fulfills the Sahm rule of a 0.5% or more increase over the past year’s unemployment rate, and is consistent with prior recession onsets that have seen a sharp, generally greater than one percentage point increase in unemployment, going into a recession.

2 These data are through Q2; Bank of America has calculated data through August that show a modest decline in the first two months of Q3.

Read more from MetLife

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document has been prepared by MetLife Investment Management (“MIM”) solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyodaku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC and MetLife Investment Management Europe Limited.