In the 14th century, traders and merchants from all over Europe would gather in the square opposite the Ter Buerse Inn in Bruges to exchange promissory notes, government issues, and other securities as they sought to raise liquidity, lay off unwanted risk, or both. Since the advent of these exchanges, or bourses, global capital markets have grown larger and more complex. Today, trillions of dollars in equities, bonds, derivatives, and commodities are traded on these exchanges daily. The flexibility and price transparency inherent in liquid markets have historically eluded investors in private equity, venture capital, and real estate, who accepted the prospect of outsize and uncorrelated returns as adequate compensation for the illiquidity and opacity of private market holdings.

However, as private markets have gone from alternative to mainstream over the past several decades, an ecosystem of investors and advisers has developed that offer ready liquidity to limited partners (LPs) and general partners alike. From its earliest incarnation on the streets of Bruges, the so-called secondaries market eventually reached private markets. They first appeared in private equity and venture capital. Now, secondaries have come of age for the largest and oldest asset class, private real estate.

Secondaries provide several potential benefits to real estate investors including, alpha generation and risk mitigation through discounted entry pricing, portfolio management efficiencies and enhanced diversification. Although this paper emphasizes traditional private equity real estate (PERE) secondaries, there are several alternative ways for investors to access this compelling opportunity.

Traditional PERE fund secondaries are purchased from LPs seeking liquidity prior to the natural liquidation of a fund’s assets. Because the fund has often been substantially invested, buyers have greater insight into the underlying assets in the fund’s portfolio. Often, they are able to secure some level of discount to the net asset value (NAV). Active secondaries investors can build portfolios that offer a compelling set of attributes, including J-curve mitigation (due to buying at discounts to reported NAV) and an exceptionally high degree of diversification, gaining exposure to many individual assets, property types, markets, and managers. Because secondaries investments are typically made later in the life cycle of a fund when assets are often closer to liquidation, their duration is significantly shorter than that of a primary fund investment. Owing to discounts, returns can be higher than those achieved on comparable assets acquired directly.

The PERE secondaries market has expanded significantly over the past decade, becoming a widely used tool for institutional investors seeking to actively manage their portfolios. The secondaries market provides a means for investors to sell down what would otherwise be illiquid holdings in a relatively straightforward manner. Recessions and corresponding real estate downcycles have historically triggered a wave of secondaries sales as investors seek to generate liquidity and rebalance their portfolios. This white paper describes the evolution of the traditional secondaries market, the structures available, the market factors that give rise to them, and how we would expect those opportunities to manifest in a post-Covid market.

Market Development & Benefits

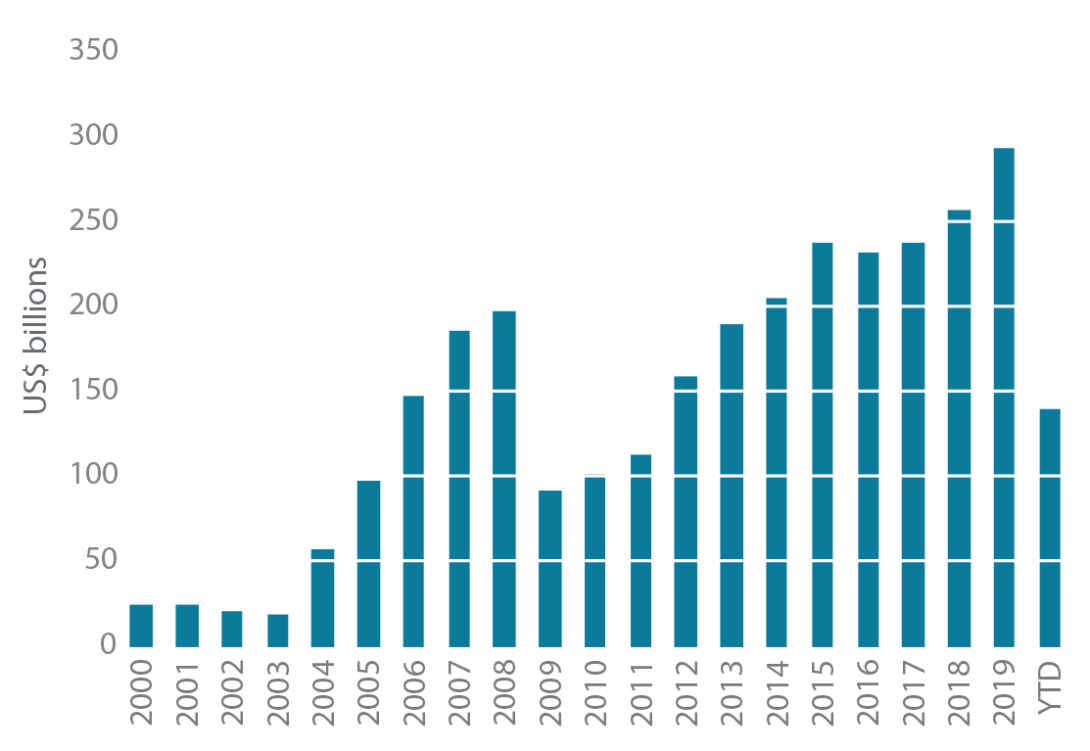

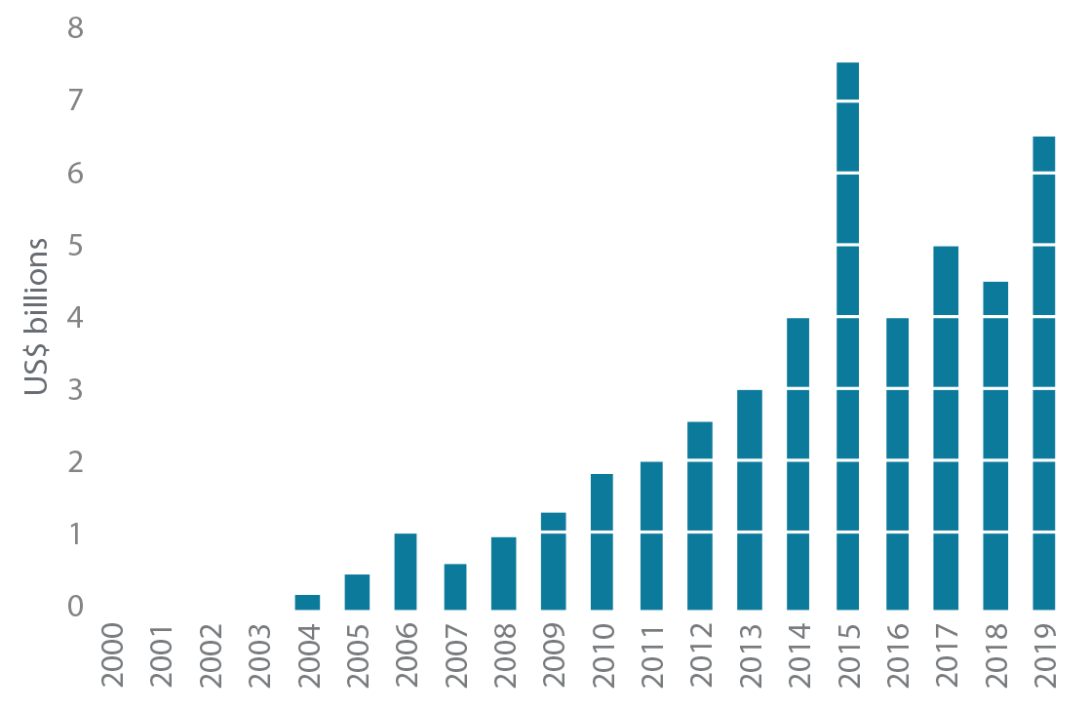

THE EMERGENCE OF THE REAL ESTATE SECONDARIES MARKET The availability of PERE secondaries opportunities will naturally reflect the size of the underlying primary fund universe (Figure 1). The comparatively low volume of real estate secondaries trading activity in the early 2000s was attributable to the relative newness of PERE funds as an institutional asset class. This was especially true of funds with either a Value Add or an Opportunistic risk profile, which only really started to grow after 2004. The PERE secondaries market emerged during the pre-GFC market upcycle and matured during the bull market that preceded the onset of the Covid-19 pandemic. Between 2002 and 2007, the average PERE secondaries transaction volume was only US$440 million, or 0.2% the size of the average outstanding PERE NAV over the same period (Figures 2). Compare this with the secondaries market for corporate private equity interests in which 1.6% outstanding corporate private equity NAV per vintage was traded.

While PERE secondaries transaction volume began its ascent during the GFC, this nascent market was fraught with failed processes due to the wide bid-ask gaps that occur anytime reported valuations lag true values.

FIGURE 1 | GLOBAL PERE HISTORICAL FUNDRAISING

Source: Preqin, August 2020.

FIGURE 2 | GLOBAL REAL ESTATE SECONDARIES TRANSACTION VOLUMES

Sources: Greenhill, Evercore, June 2020.

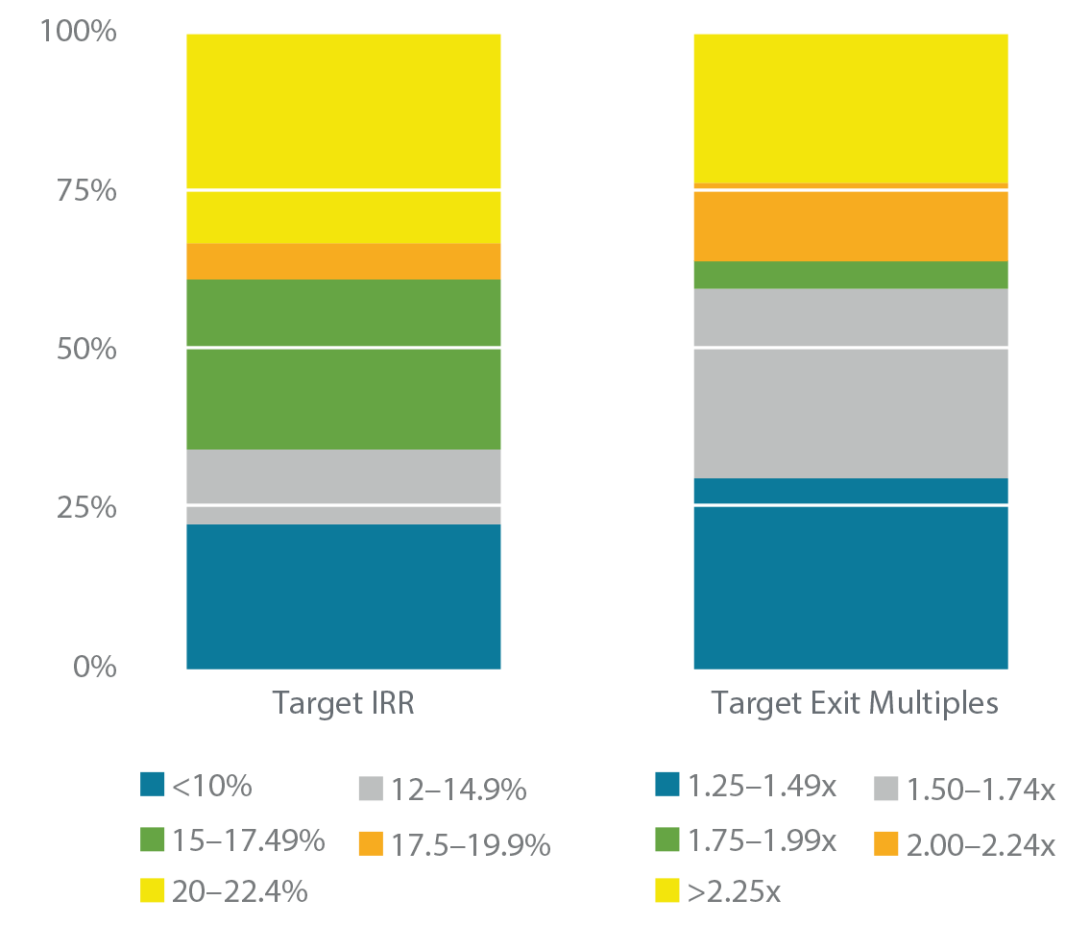

As the direct asset trading volumes began to pick up in 2010, buyers’ and sellers’ perception of value converged, enabling meaningful levels of secondaries trading. Just as the dot-com bubble had a multiplier effect on private equity secondaries activity, the GFC catalyzed a step-function increase in PERE secondaries activity that has persisted. Annual transaction volume averaged US$5.3 billion between 2014 and 2019, a greater-than-tenfold increase relative to the five-year pre-GFC average. At the end of 2019, real estate secondaries assets under management were US$25.3 billion—more than a 1,000% increase over 2009 levels.Most investors tend to regard PERE secondaries as a highyield strategy. As seen in Figure 3, nearly two in three buyers had a target return of 15% or above, which is consistent with Value Add and Opportunistic strategies. Still, there are plenty of opportunities farther down the risk–return curve. These opportunities in Core and Core-Plus real estate have historically been more prevalent in developed markets. Through the first quarter of 2020, nearly 80% of the Global Real Estate Core Fund Index was allocated to North America and Europe.1

Lower-risk real estate fund strategies are typically executed through perpetual open-ended structures that permit investor subscriptions and redemptions on an ongoing basis. Although these vehicles have liquidity mechanisms, redemption queues, the suspension of redemptions, and other issues have undermined the effectiveness of these mechanisms. As a result, a vibrant secondaries market has developed. This initially grew in the UK, where subscriptions and redemptions typically entail friction costs that mirror those of the direct transaction market, so there was naturally a “secondaries price” where willing buyers and sellers could trade inside the spread of these costs. This market is now well established globally with good levels of price transparency intermediated by a small number of dedicated brokers and, in certain instances, the GPs themselves.

FIGURE 3 | DEDICATED REAL ESTATE SECONDARIES BUYERS’ TARGET RETURNS

Source: Campbell Lutyens, 2019.

POST-GFC PERIOD PERE FUND SELLER MOTIVATIONSThe very factors that allowed the PERE secondaries market to flourish after the GFC continue to provide prospective sellers with a relatively straightforward and efficient option for generating short-term liquidity. These factors, which are summarized below, were central to the development of the PERE secondaries market.

» Portfolio Management Decisions. LPs rebalance their portfolios for several reasons including increasing or decreasing their exposure to private real estate;2 changing the number of investment manager relationships; reducing or increasing holdings overseen by underperforming or outperforming managers; changing risk profile exposures; shifting exposure from fund investments to direct investments or joint ventures seeking additional control; and rebalancing exposures to certain geographies or real estate product types.

» Regulatory Changes. Regulatory changes following the GFC resulted in new policies aimed at mitigating the effects of future downturns. Basel III set higher capital reserve requirements for banks, particularly for their higher-risk private equity investments. Solvency II, which governs European insurance companies, also imposed higher reserve requirements and penalizes illiquid investments such as real estate. These regulatory changes induced meaningful sales volumes over several years.

» Need for Liquidity. The disruption caused by the GFC forced many funds to extend the business plans of their investments, thereby increasing their duration. Many perpetual open-ended funds faced delays in asset sales and also developed exit queues, freezing liquidity for their investors. As a result, the secondaries market expanded to meet investors’ demand for liquidity.

BUYER BENEFITSWith the expansion of the PERE primary funds market and the disruption created by the GFC, real estate secondaries became a potential opportunity for investors. In a similar vein to the corporate private equity secondaries market, traditional PERE secondaries offer a number of key benefits including:

» J-Curve Mitigation. Secondaries mitigate the J-curve effect that is typical in primary investments in funds by providing investors exposure to specified and seasoned assets at discounts to their market value and allowing them to avoid paying fund management fees and costs before all of the fund’s capital is invested.

» Discounted Entry Pricing. Traditional PERE secondaries are typically acquired at a discount to NAV. Figure 4 shows that particularly accretive pricing can be achieved when markets are stressed. Discounted entry pricing, which was prevalent throughout the bull market of 2010–2020, provides both downside risk mitigation and alpha-generating potential.

» Diversification. A secondaries investment program includes multiple investments in funds, each of which owns multiple assets. Therefore, real estate secondaries investors have the potential to achieve an extraordinarily broad level of diversification by region, property type, number of assets, and vintage year.

» Mitigated Execution Risk. In contrast to investing in blindpool funds, secondaries buyers can underwrite existing and, in the majority of instances, fully specific portfolios.

» Managing Duration Risk. Since secondaries investments are typically made deep into the life of a fund, the manager’s business plan has usually been fully actualized. Consequently, secondaries may be less risky and closer to realization, therefore reducing market cycle risk.

FIGURE 4 | PERE FUND SECONDARIES PRICING VS NAV

Source: Greenhill, July 2020.

Available Strategies & Structures

CLOSED-ENDED VEHICLESClosed-ended PERE fund structures are typically used for higher risk–return value add and opportunistic strategies, although a few Core-Plus programs are also executed through these vehicles. PERE secondaries in closed-ended funds can be broadly categorized by life cycle.

» Early-stage funds are largely unfunded, having only been raised within the last three years. Sellers are released from their commitment obligations, and prospective buyers only have partial visibility on what remains an incomplete portfolio.

» In seasoned funds, the GP has made all of the underlying investments, and the business plans for each are often at varying stages of fruition. Prospective buyers have substantial to full visibility on the portfolio's composition.

» Significant realization activity has taken place in tail-end funds; any remaining assets are likely to be highly seasoned. Prospective buyers have full visibility on the assets.

OPEN-ENDED VEHICLES

Core and Core-Plus funds are typically structured as perpetual vehicles with subscription and redemption mechanisms. The ability to provide investors with liquidity varies at different phases of market cycles.

In stable market conditions, there may be entry queues, which allow managers to easily service investors’ liquidity needs with new investors’ capital, or by selling assets into strong markets. When market conditions are favorable, investors are often able to sell their interests in open-ended funds at premiums to their NAV. Investors seeking to enter the fund see the advantage of this “queue jumping” because they can put their capital to work more quickly than they could by waiting several quarters for the queue to clear.

By contrast, during market downturns, there tend to be more investors seeking liquidity than investors seeking to enter a fund; if property values have declined, managers are reluctant to sell assets to service investors’ liquidity needs. In addition, dislocations between NAVs, which are based on appraisals, and the ”true’’ fair market value (FMV) make it hard to set the redemption price. When this occurs, fund managers will “gate” redemption activities. These situations can lead to attractive opportunities for secondaries buyers with medium-term investment horizons who can benefit from the discounts that arise from short-term overselling.

ACCESSING PERE SECONDARIES

LPs can access real estate secondaries directly, through dedicated closed-ended commingled funds, or through separately managed accounts. According to Preqin, in 2019 these commingled funds had US$25.5 billion in assets under management and US$8 billion in dry powder. Like direct secondary investments, these funds typically focus on investments farther up the risk curve. Although Core and Core-Plus investments are not yet commonly pursued by commingled funds, LPs can access these opportunities through SMAs, which can be tailored to meet investors’ preferred exposure.

INNOVATIONS IN PERE SECONDARIES TRANSACTION STRUCTURESOver the past decade, secondaries investors across private markets have introduced an array of new structures and solutions. The secondaries transaction structures described below seek to allow managers and investors to more flexibly manage portfolio construction, liquidity, and, in certain instances, reduction of “face” discount.

» Vertical strips involve the sale of partial interests in LP positions, enabling sellers to reduce their exposure but retain positions and continue their relationships with the fund manager.

» Fund windups seek to provide liquidity to investors at the tail ends of funds while providing GPs with sufficient time, capital, and incentive to maximize remaining value.

» Direct secondaries are a portfolio management tool that allows LPs to acquire a partial interest in underlying assets and joint ventures held by funds to deliver liquidity.

» In deferred payment structures, the acquisition consideration is partially paid up front with defined payments at future dates. Distributed proceeds can be used to meet the future payment obligations to the seller or to reduce the secondaries buyer’s basis. Deferral mechanisms effectively create leverage for the secondaries buyer, and while they can enhance performance, as with any type of leverage, they can also create material performance volatility.

» Structured secondaries are executed as a financing solution rather than a transaction. For example, secondaries managers could provide LPs with the liquidity to fund outstanding commitments without absorbing the discount that might be required for an outright exit. The secondaries manager benefits from a defined fixed return coupon and/or minimum equity multiple with both parties sharing proportionately in future performance.

The Opportunity Going Forward

During the GFC, PERE funds were in a dire position due to a combination of overleverage, illiquid capital markets, and uncertain economic prospects. This meant that investments in secondaries posed excessive risk. Although assets were generally less levered at the beginning of the Covid-induced recession than at the commencement of the GFC, we expect many of the same dynamics will be present during the impending real estate market downturn. When equity values decline as quickly and as drastically as they do during significant market downturns, it is difficult for astute buyers to acquire secondaries because the FMV of fund interests is generally much lower than the NAV reported by fund managers. Since LPs tend to base the value of a fund interest on the GPs’ reported NAVs, and since fund managers do not typically write their assets down quickly enough to keep pace with true FMV declines, bid-ask spreads widen.

Given the risks of further rent, occupancy, and value diminution prevalent during market downturns, as well as the uncertainty about the timing of a recovery, prudent secondaries buyers should apply conservative underwriting approaches. Sound underwriting requires exceptionally conservative assumptions, such as declining rents, falling occupancy rates, expanding capitalization rates, the loss of certain assets to foreclosure, and the need for equity infusions to bridge the gap between outstanding loan balances and available refinancing proceeds upon loan maturities. The depressed values that emerge owing to this (appropriately) conservative underwriting approach stand in stark contrast to overstated NAVs that many funds tend to report in a declining market. The bid-ask spread can be significant as a result.

During the post-GFC downturn, many PERE fund investors were acutely aware that the values of their interests were plummeting and that they would face liquidity problems throughout their portfolios. These LPs smartly turned to the previously underutilized secondaries market in an attempt to divest. Understandably, upon receiving bids, few of these prospective sellers elected to part with their assets. With market-bottom pricing, LPs would be paid pennies on the dollar for their fund positions; holding on to their devalued PERE fund interests and awaiting a market recovery seemed to be the better decision for most LPs. Although the ratio of transactions completed to secondaries offered for sale was quite low during the post-GFC downturn, in absolute terms, PERE secondaries volume remained steady at approximately US$800 million per year in 2008 and 2009, before doubling to more than US$1.6 billion in 2010 (Figure 2).

Secondaries struck early in the recovery have been strong performers. These transactions benefit from the initial acquisition discount, improving fundamentals as the real estate market recovers, declining yields as capital market participants grow more competitive, and a high rate of realizations. Though pricing tends to strengthen as the market shifts from forced selling for liquidity to opportunistic selling for portfolio management, returns do not necessarily deteriorate. This is because marks more closely resemble the FMV, and the recovery tends to gain steam mid-cycle.

Whatever faulty wiring Covid exposes is likely to cause the market to recalibrate around a modified framework for risk management. In certain cases (e.g., portfolio management), it will be self-imposed; in others, it will be mandatory. These modifications could trigger a wave of secondaries sales similar to what we saw in the wake of the GFC. If they do, we would expect a strong buyers’ market. For the simple reason that investors are more familiar with secondaries, we believe there will be more portfolio-management-driven secondaries sales during the post-Covid recovery than there were post-GFC.

Conclusion

PERE funds have become a large and established global asset class with a permanent allocation in most institutional investor portfolios. Perhaps inspired by the 14th-century streets of Bruges, a natural extension of this growth has been the growth of a secondaries market for interests in these funds. This has included the emergence of cadres of specialist secondaries buyers and liquidity providers, dedicated to offering increased flexibility to managers and investors in this otherwise illiquid asset class. The catalysts for transactions and the overall opportunity set will ebb and flow with the direct real estate market. Downcycles will often trigger the greatest need for liquidity on behalf of investors and their holdings. Avoiding the falling knives requires diligent underwriting and patience.

The ultimate toll of Covid-19 on the global economy and the manner in which real estate will be utilized in the future is still being unveiled. So far, Covid’s economic effects have been disguised by unprecedented fiscal and monetary stimulus. While we can speculate on the winners and losers, the depth of the trough and the shape of the recovery remain unknown. Thus, we recommend a cautious and patient approach over the coming quarters; a significant volume of PERE secondaries may emerge over the next 12–24 months as LPs seek liquidity for a variety of reasons. Given the benefits that PERE secondaries can impart to investors’ portfolios, we believe an attractive opportunity is on the horizon.

1 INREV, ANREV & NCREIF. 2020. “Global Real Estate Fund Index.”

2 In some cases, this is owing to the denominator effect.

Read the full article here

This document is for information purposes only and has been compiled with publicly available information. StepStone makes no guarantees of the accuracy of the information provided. This information is for the use of StepStone’s clients and contacts only. This report is only provided for informational purposes. This report may include information that is based, in part or in full, on assumptions, models and/or other analysis (not all of which may be described herein). StepStone makes no representation or warranty as to the reasonableness of such assumptions, models or analysis or the conclusions drawn. Any opinions expressed herein are current opinions as of the date hereof and are subject to change at any time. StepStone is not intending to provide investment, tax or other advice to you or any other party, and no information in this document is to be relied upon for the purpose of making or communicating investments or other decisions. Neither the information nor any opinion expressed in this report constitutes a solicitation, an offer or a recommendation to buy, sell or dispose of any investment, to engage in any other transaction or to provide any investment advice or service.

Past performance is not a guarantee of future results. Actual results may vary.

Each of StepStone Group LP, StepStone Group Real Assets LP and StepStone Group Real Estate LP is an investment adviser registered with the Securities and Exchange Commission (“SEC”). StepStone Group Europe LLP is authorized and regulated by the Financial Conduct Authority, firm reference number 551580. Swiss Capital Invest Holding (Dublin) Ltd (“SCHIDL”) is an SEC Registered Investment Advisor and Swiss Capital Alternative Investments AG (“SCAI”) (together with SCHIDL, “SwissCap”) is registered as a Relying Advisor with the SEC. Such registrations do not imply a certain level of skill or training and no inference to the contrary should be made.

Manager references herein are for illustrative purposes only and do not constitute investment recommendations.