Increasingly, companies are being measured not only by their earnings and cash flow, but according to the effect their activities have on the environment and society. As a result, credit investors no longer judge those companies solely on their risk and return characteristics, but increasingly by their external impact as well.

So-called impact investing is not a new asset class: it is a natural extension of environmental-, social-and governance- focused (‘ESG’) investment approaches in credit. The idea is to identify debt issuers on the right side of change— those that are seeking to deliver a beneficial environmental and social impact, as well as positive financial returns.

Impact investing has grown considerably in the past few years. But a lack of knowledge and several commonly shared misconceptions may discourage investors from considering this way of investing in credit.

In this article, we attempt to debunk four popular myths about impact investing, as well as showing how T. Rowe Price’s Global Impact Credit Strategy addresses them.

Four impact investing myths

Myth 1: “Impact investing doesn’t work in the secondary market”

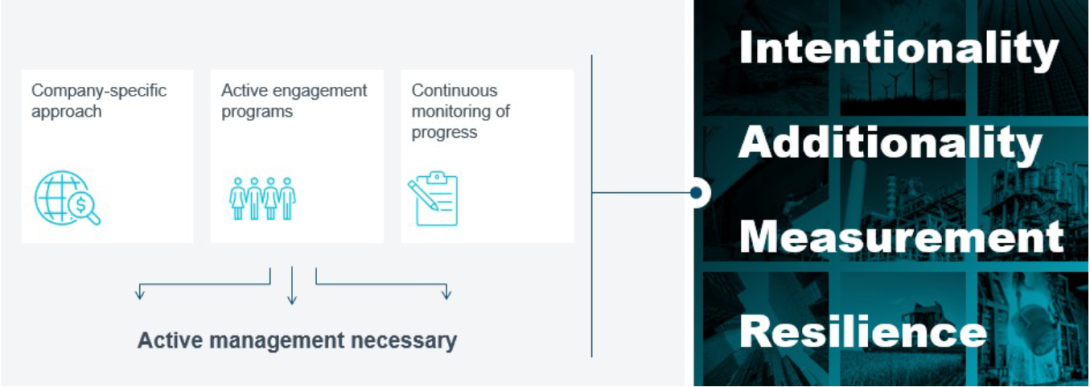

In theory, impact investing is simple, but in practice it is not easy. Active management is crucial in making a real difference in the secondary market for corporate credit, for three reasons: the need to take a company- specific approach; the requirement for active engagement; and the need for continuous monitoring.

Three reasons for active management in impact investing

Company-specific approach

Any analysis of impact investments in the secondary credit market requires a company-specific, bottom-up approach. We use our proprietary research models to help identify and screen impact opportunities, ensuring that all investment decisions are based on a clearly defined, positive impact thesis that is both material and measurable.

With every impact investment, we identify a Key Performance Indicator (KPI) that we record, track and report over time.

Active engagement

Active engagement aims to ensure our capital is being used for the desired impact investment. We don’t invest passively in corporate debt; we seek to influence companies’ decisions to ensure that our clients achieve their desired impact investment goals. We believe active engagement is a prerequisite to achieving these objectives.

Continuous monitoring

Continuous monitoring of a company’s progress towards its impact goals is vital. On a regular basis, we revisit the thesis of our impact investment, alongside the company’s post-issuance reporting, to ensure it remains on track with the portfolio’s desired goals. This outcome- oriented approach also helps us track our KPIs, meaning we can report our annual impact metrics to clients comprehensively and transparently, helping them assess the impact their investments have made.

These three tenets rely on a diligent and methodological impact investing philosophy. We embed the principles of intentionality, additionality, measurement and resilience into our everyday impact investment process.

For more on our philosophy, please view our impact charter, which delves deeper into these principles.

Myth 2: “Only ESG-labelled bonds can create a positive impact”

We disagree with this assertion: impact investing, in our view, can and should go beyond bonds labelled as having a positive environmental, social or governance impact. While we do invest in labelled-bonds, our Global Impact Credit Strategy also seeks impact investments outside the ESG labelled- bond market. We believe this approach offers us greater depth and diversity, as well as presenting additional alpha generation opportunities.

There is an abundance of issuers whose products, solutions, and activities create a positive ESG impact. Many of these companies choose to finance their activities through conventional, as opposed to ESG-labelled bonds.

For example, renewable energy developers help reduce carbon emissions through solar and wind projects. Emerging market banks drive financial inclusion through microfinance. And not-for-profit paediatric hospitals provide healthcare solutions in an inclusive and affordable manner.

As at the end of October 2022, approximately 42% of our Global Impact Credit representative portfolio was made up of high-impact, non-labelled bonds.

NextEra Energy Partners falls into this category: it operates an industry-leading portfolio of wind, solar, and battery storage assets. 100% of the company’s power generation comes from clean or renewable resources, which will accelerate global decarbonisation by supporting the transition of energy production away from fossil fuels. Ignoring such investments on the basis of the absence of an ESG label could be a missed opportunity.

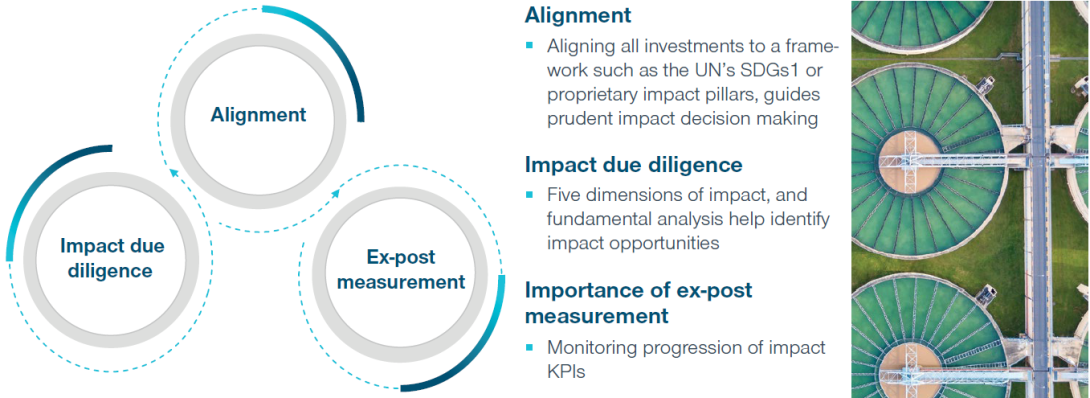

However, accepting a non-labelled bond in an impact credit portfolio is more challenging than relying on a bond issue whose use of proceeds is clearly earmarked. In our Global Impact Credit Strategy, we therefore ensure that every investment is aligned to one of our 3 proprietary impact pillars, 8 sub- pillars and at least one UN Sustainable Development Goal (SDG).

After identifying this alignment and quantifying its extent, we carry out an in-depth due diligence process on every impact investment. We then commit to monitoring and measuring the progression of impact KPIs. In the diagram below, we show how we qualify a non-labelled bond as impact in our Global Impact Credit Strategy.

Finally, there are risks associated with investing only in ESG-labelled bonds. The labelled bond market is dominated by a small number of sectors, which may result into reduced diversification and higher systemic risk. The so-called ‘greenium’—a valuation premium for bonds that are labelled as green—can also compromise the relative value of labelled-bonds and reduce the alpha opportunities for investors.

Qualifying a non-labelled bond

1 United Nation’s Sustainable Development Goals

Myth 3: “Achieving impact requires an overhaul of the portfolio construction process”

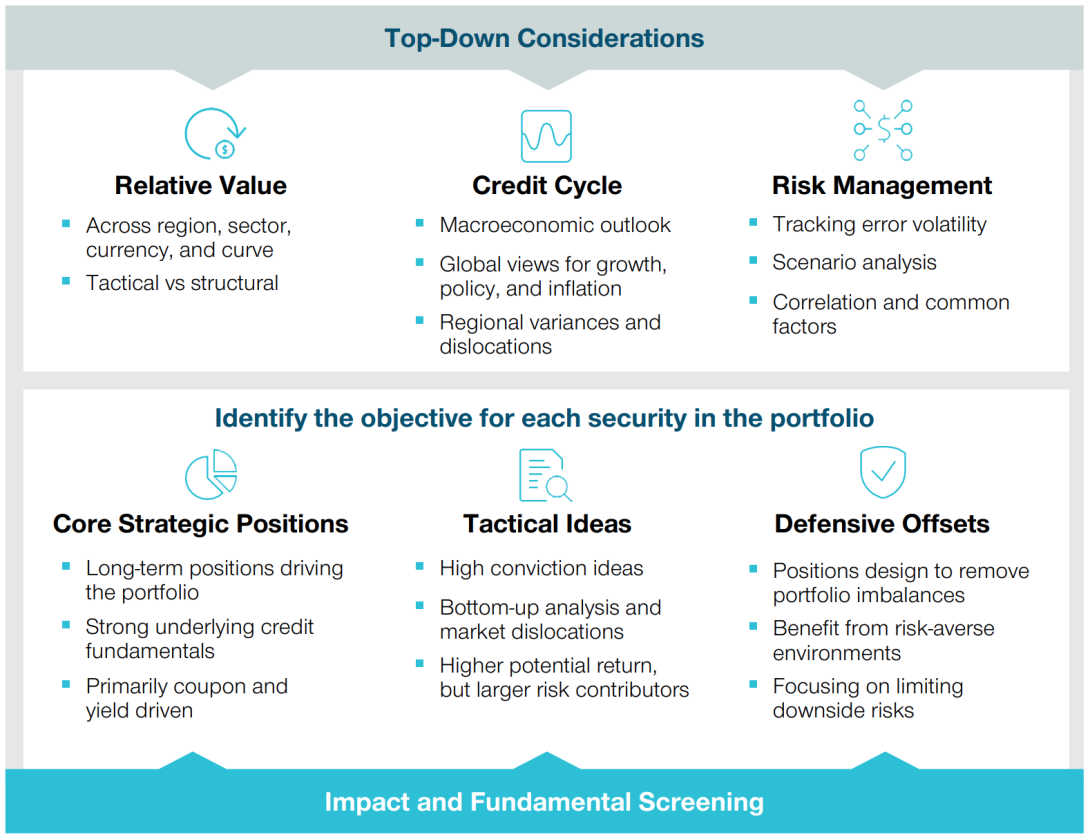

Again, we don’t believe this to be true. The traditional portfolio construction process forms the foundation for impact investing, but just requires an additional step: screening potential investments for their impact characteristics.

The risk management of an impact portfolio is also consistent with that of a traditional bond portfolio. We manage the portfolio in a similar way to our Investment Grade Credit Strategy, which combines three types of market ‘beta’: core strategic positions (around 70% of the representative portfolio), tactical, higher-beta bets (around 15%) and defensive offsets (also around 15%).*

Top-down considerations, such as global relative value and macro-economic variables, also influence the sources of portfolio risk and their desired level. However, our bottom-up impact screening process is the starting point of portfolio construction (see the diagram).

*as of 30 September 2022

Impact screening is the starting point of portfolio construction

Myth 4: “An impact approach causes higher tracking error”

Any actively managed portfolio whose bond weights differ from those of the benchmark will inevitably have some tracking error. But an impact credit portfolio will not necessarily have higher tracking error than a traditional bond portfolio, despite the more limited investment universe.

Like any actively managed strategy, impact credit portfolios can be managed flexibly to suit different client objectives, such as demands for specific duration, credit quality and beta. And just as in a mainstream credit portfolio, an impact portfolio manager can deliberately target the level and sources of risk, based on market views and client objectives.

For example, we recently ran four model impact credit portfolios to demonstrate how flexible budgeting for duration, yield curve, sector, quality, and tracking error can achieve a desired level of risk, whilst still capturing impact. The below demonstrates this by showing how each portfolio’s tracking error stays in check despite the range of differing mandates (conservative to income):

Flexible budgeting across duration, curve, sector, and quality to achieve desired risk

| | Bloomberg Global Aggregate Credit | | Impact - Conservative | Impact - Income | Impact - Aggressive |

| Quality | A2/A3 | | A3/Baa1 | Baa1/Baa2 | Baa2/Baa3 |

| Option Adjusted Spread (OAS) (bps) | 144 | | 185 | 206 | 252 |

| USD Hedged Yield | 5.08% | | 5.54% | 5.72% | 6.23% |

| Option Adjusted Duration (OAD) | 6.35 | | 6.25 | 4.15 | 6.21 |

| Duration Times Spread (DTS) | 9.57 | | 11.46 | 9.29 | 15.05 |

| Tracking Error Volatility (TEV) (bps) | N/A | | 113 | 160 | 240 |

For illustrative purposes only.

The impact models shown are based on the Global Impact Credit representative portfolio and customized to reflect different holdings and security weights to demonstrate the potential outcome of different risk scenarios across the risk spectrum. The conservative portfolio is adjusted to hold a high percentage [>30%] to defensive securities, such as Supranationals, as these generally have lower spreads, beta, and credit risk compared to the benchmark. The aggressive portfolio has larger exposure to securities with higher spreads, beta and credit risk, such as emerging markets. The income portfolio has greater emphasis on income generating securities versus beta.

Model Results: The results shown above are based on the application of a model and do not represent the actual returns of any T. Rowe Price product or strategy. Model results are hypothetical, do not reflect actual investment results, and are not a guarantee of future results. Model results were developed with the benefit of hindsight and have inherent limitations. Model results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Certain assumptions have been made for modeling purposes that may not be realized. Management fees, transaction costs, taxes, potential expenses, and the effects of inflation have not been considered and would reduce returns. Results have not been adjusted to reflect the reinvestment of dividend and capital gains. Actual results experienced by clients may vary significantly from the results shown.

Source for Bloomberg data: “Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price.

Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend this product. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to this product.

Conclusion

At T. Rowe Price, we believe that impact investing is a vital tool for credit investors wishing to incorporate a positive environmental, social or governance impact into their fixed income portfolios. In this article, we showed that impact investing in credit can go hand-in-hand with the traditional investment process, but requires a clear, methodical impact philosophy and an active approach.

By bringing together deep fundamental and impact research capabilities with an active approach that goes beyond ESG-labelled bonds, we believe we can consistently deliver both impact and outperformance relative to the portfolio’s benchmark.

Download PDF

Authors

Matt Lawton

Portfolio Manager, Fixed Income

Benji Baxter

Portfolio Analyst, Fixed Income

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2022 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

LE63857 (11/2022)

202210 -2501754