As the global economy continues to recover, an accommodative Federal Reserve (Fed) and stimulative fiscal policy have pushed inflation concerns to center stage. By some measures, inflation is at its highest in over a decade, and several factors could sustain these levels. Conversely, other metrics point to a more benign environment, and suggest the recent increase may be “transitory.” While we do not predict the future, we believe overall inflation risks are elevated, particularly given current spreads and valuations. In this piece, we focus on key inflation metrics and the potential impact of inflation on the insurance industry.

On a Scale of 1 to 10, How Much Does This Hurt?

Inflation impacts various types of insurers differently. Near term, inflation has the potential to pressure the cost of claims and bond prices, however, longer term, elevated interest rates likely to accompany inflation present an opportunity to increase book yields and net investment income by reinvesting cash flows at higher rates.

Property & Casualty (P&C) • P&Cs insuring single-family homes and autos, sectors with outsize inflation, may see a rise in claims for specific damage to these types of assets as the cost to repair and replace has risen in recent months.

Health • Health insurers may see higher claims costs as a result of rising health care expenses and increased demand for medical procedures deferred during the pandemic.

Life • Life insurers will likely benefit from modest inflation, primarily due to potentially higher long-term bond yields which could be beneficial for the spread-based liabilities of life insurers.

Insurers are mitigating the higher claims costs by repricing policies and raising premiums, which provides a measure of protection, and demonstrates the pricing power of insurance companies as the prices of many goods and services rise.

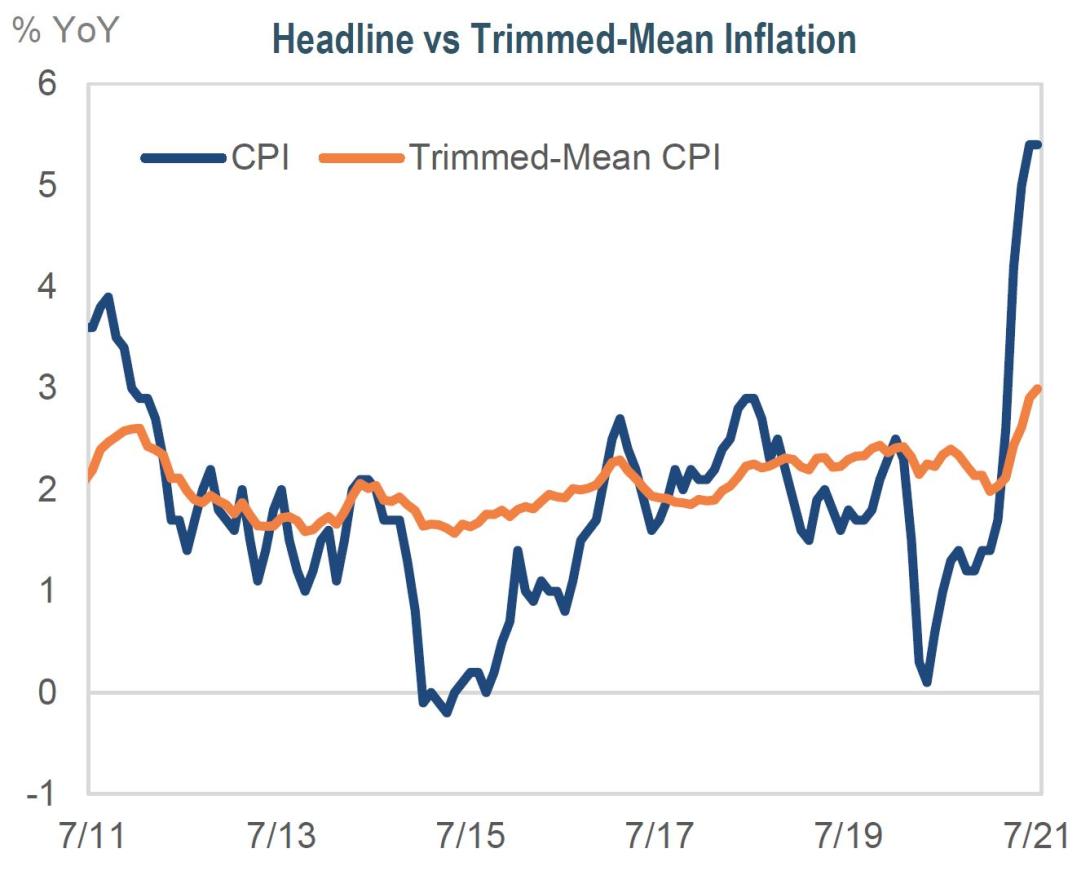

Measuring Inflation: The Devil Is In The Details

Alphabet soup. There is no one way (or acronym) to measure inflation. While each method helps tell the story, Consumer Price Inflation (CPI) and Trimmed-Mean CPI are two key metrics that illustrate how results can differ based on the methodology.

CPI, or headline CPI, measures the prices paid by consumers for a basket of goods and services, including food and energy, which are often more volatile. The recent jump in CPI has been fueled in part by supply chain bottlenecks. For example, used cars and trucks account for almost one third of recent increases, which have been affected by the chip shortage.

Trimmed-Mean CPI¹ adjusts CPI to remove items with the highest and lowest one-month price changes. By excluding outliers, this metric can provide better signals of underlying trends.

Both metrics show an increase in inflation. However, trimmed- mean CPI has experienced a much smaller rise, which might indicate a more transitory jump than a sustained shift higher.

Inflation expectations are important. The Fed watches real-time inflation data, but also factors expectations into their decisions. The Fed closely monitors breakeven inflation rates, which measure the difference in yields between nominal Treasuries and similar-maturity TIPS (Treasury Inflation-Protected Securities). Although breakevens have been on the rise, they recently fell as the Fed continues to emphasize the temporary nature of the current inflation spike.

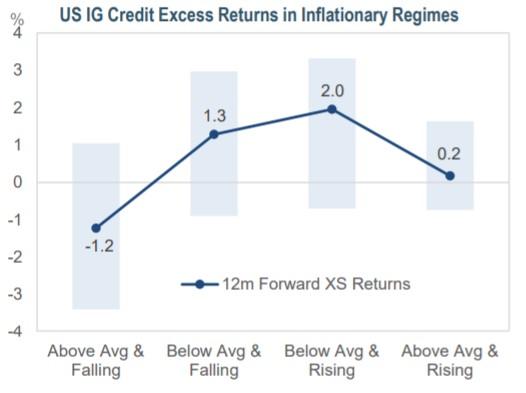

Impact of Inflation Regimes on Different Asset Classes

Based on history, trend inflation, defined as the 5-year rolling average of CPI, is at relatively low absolute levels. Asset classes respond differently when inflation is rising or falling relative to trend.

Sourced from Morgan Stanley as of 7/31/2021 and shows 12 month forward US IG Credit excess returns in inflationary environment based on CPI from 1970 to 7/31/2021.Blue bars show the interquartile range of excess returns and dark blue line is the median.

Where are we now? Inflation was below trend going into 2020. However, since hitting a pandemic-low of 0.1% in May 2020, inflation has broadly moved higher. While base effects and supply chain bottlenecks have factored into recent CPI reports, the last two readings have been sharply above trend, which could have implications for asset returns.

Treasuries tend to perform worst in rising inflation environments, as higher inflation both reduces the value of cashflows and typically leads to higher interest rates.

TIPS can offer protection against rising inflation. However, TIPS returns are more correlated to interest rates than changes in inflation. Additionally, TIPS look most attractive when deflation fears have pushed breakevens near zero.

Credit typically does best when inflation is below average and rising, which is generally an indicator of economic growth. However, too much inflation might be the result of an overheating economy, which can lead to diminished returns.

Securitized assets can offer attractive relative value in this environment. These bonds have more frequent cashflows than a corporate bond, providing the ability to reinvest at a higher rate if rates rise due to inflation, boosting book yield.

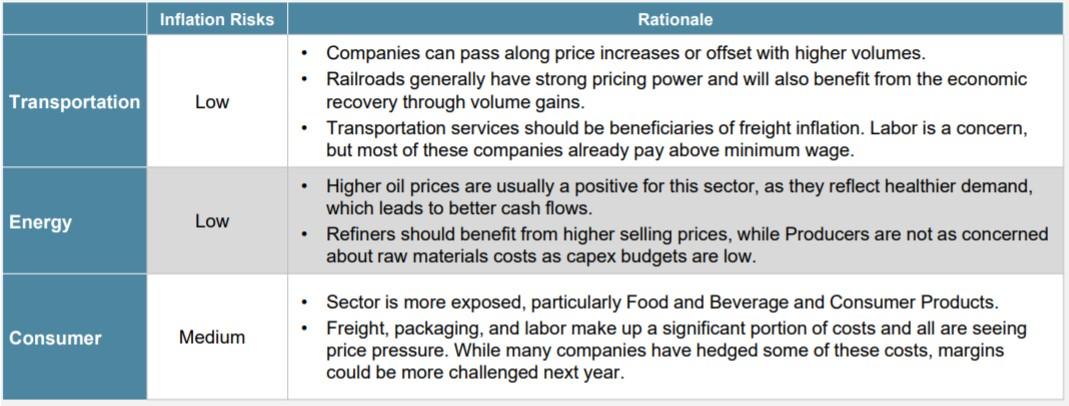

Opportunities and Watchouts In A Rising Inflationary Environment

Within credit, we believe certain sectors, such as Transportation and Energy, are better positioned to moderate the impact of inflation. We think other sectors, like Consumer, are less so.

Don’t throw the baby out with the bathwater. Although some sectors are more inflation-sensitive, there are attractive opportunities at the security level. Given current valuations and higher overall risk levels, we think it is prudent to focus only on the highest conviction ideas.

The Only Thing I Cannot Predict Is The Future

Accurate forecasting is difficult. The number of scenarios that could lead to greater inflation have increased, and several factors may lead to a sustained higher level. This bout of inflation could also be temporary, as there are many structural elements that could keep levels low.

Upside Risks • Accommodative monetary and fiscal policy. The Fed’s balance sheet has expanded more than during QE1, 2, and 3 combined. Fiscal response increased the budget deficit in 2020 to almost 15% of GDP, compared to the 50- year average of 3%. • Fed policy. In a historic shift, the Fed last year stated that it would target an average, instead of fixed, 2% inflation level. Fed officials have commented that they are comfortable letting inflation “run hot” for some period to achieve this goal. • Labor market pressure. Job openings are at a record high, but so is the percentage of firms not able to fill positions. Certain sectors, like hospitality and leisure, are seeing significant growth in wages.

Downside Risks • Demographics. Forecasts call for a declining birth rate and general graying of the population. An older and slower-growing population may be deflationary if it leads to lower overall demand. • Technology. Besides creating a better iPhone, technological revolutions lead to supply-side shocks. These shocks can be deflationary, enabling companies to produce more for the same cost or less. Many automation trends that existed before COVID accelerated during the pandemic, which could constrain labor pressure. • Labor market pressure. The US is still roughly 7 million jobs short of pre-pandemic levels, and there remains little sign of broad wage pressures. Additional unemployment benefits are set to expire in September, which could lure more workers back to the workforce.

Don’t go chasing waterfalls. Inflation is an important factor to consider when making decisions related to portfolio positioning. While we do have views on the potential direction of inflation, we remain duration-neutral and instead express these views through bottom-up security selection. We prefer to remain diversified and “take what the market gives us,” rather than position for a specific forecast.

At IR+M, we believe the risk of higher inflation, particularly in an environment of tighter spreads and high relative valuations, cannot be overlooked. However, we maintain that inflation is difficult to predict accurately and consistently, and as such, do not position for a specific target. We endeavor to create well-diversified portfolios and rely on our bottom-up security selection expertise to identify bonds that may be less susceptible to rising inflation. If inflation does lead to increased interest rates insurers stand to benefit due to the ability to reinvest at higher rates.

Bloomberg, Bloomberg Barclays and IR+M Analytics as of 7/31/2021. 1Trimmed-Mean CPI refers to the Federal Reserve Bank of Cleveland 16% Trimmed-Mean CPI.

The views contained in this report are those of IR+M and are based on information obtained by IR+M from sources that are believed to be reliable. This report is for informational purposes only and is not intended to provide specific advice, recommendations for, or projected returns of any particular IR+M product. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Income Research & Management.