Introduction

Over the past several decades, the residential rental sector has grown from relative obscurity to become one of the largest and most important institutional investment asset classes. The sector offers a wide range of investment options, including:

- Risk profiles – as low risk as first-lien mortgages to as high risk as ground-up development.

- Housing formats – from class-A high-rise apartment to manufactured housing communities, and everything in-between.

- Geographies – institutional residential investors are now active in over 50 cities across the U.S.

In recent years, investors have also begun considering how the income profiles of residents could shape investment strategies. Looking at strategic opportunities in the sector, we believe Moderate-Income Rental Housing offers attractive long-term risk-adjusted returns while supporting the need for more affordable housing in the U.S.

What is Moderate Income Rental Housing?

Rental housing has traditionally been segmented into two income-related categories: [1] marketrate rental housing and [2] government subsidized rental housing

For market-rate housing, rent for new leases is set by the landlord and governed only by prevailing supply and demand conditions in the market without restrictions.

Subsidized housing is a generic term covering all federal, state, or local government programs that reduce the cost of housing, typically for low- or moderate-income residents. This can include government-owned public housing, Section 8 (vouchers provided by the government that reduce the cost of privately owned housing), Low Income Housing Tax Credits that encourage investors to own or build housing for low- or moderate-income residents, among other programs. Owners of subsidized housing are typically required to charge rents that serve residents earning less than 60% of area median income.1

In addition to these two traditional groups, a new category is emerging. For the purposes of this analysis, we will refer to this category as “Moderate Income Rental Housing”, or MIRH. Additional colloquializations include “workforce housing”, “non-subsidized affordable housing”, “class B/C apartments”, among others.

While there is not a single authoritative definition, MIRH typically focuses on market-rent housing intended for moderate income residents, filling a gap between typical subsidized housing that explicitly limits costs to low-or-moderate income renters, and traditional market rate housing that has typically focused on middle-or-upper income renters. Importantly, renters in the MIRH category might exceed income limits for subsidized housing but may also stretch to afford typical market rate rentals.

Our definition of MIRH has two components. First, MIRH is market-rate housing that caters to residents earning between 60% and 120% of local area median income. Formats could include a range of options such as mid-or-high-rise apartments, garden apartments, manufactured housing, or single-family rentals. Second, the rent is offered at a rate that is between 20% and 40% of the renters’ monthly gross income.

A Few Words on Rent Control…

In the interest of disambiguating rental housing terminology, it is worth briefly mentioning “rent control / rent stabilization”. These laws generally put a limit on annual rent increases and outline tenant eviction protections. One example of a rent control law is AB 1482, or the “California Tenant Protection Act”, which passed in 2019 and went into effect on January 1, 2020. AB 1482 restricts the allowable annual rent increase for all California multifamily rental units to 5% plus a local costof-living adjustment of no more than 5%, for a maximum annual rent increase of 10%.2

Rent control laws vary widely by city, and, generally speaking, are uncommon outside of New York, Oregon, and California (which we estimate account for 25% of the rental housing universe).3 However, one common theme among municipalities that employ rent control is to specify older buildings under the purview of rent control legislation. For example, AB 1482 only applies to buildings 15 years old or older. Because MIRH may be more likely to be older vintage housing, it may also be more likely to be subject to rent control.

Mitigating this risk to MIRH is the fact that rent increase limits are typically much higher than what MIRH investors would underwrite over a holding period. Sticking with the AB 1482 example, few investors would underwrite more than 10% rent growth per year. Risks from rent control are more applicable to Class B to Class A conversions, where significant unit upgrades are made with the intention of materially increasing rents and targeting higher-income households. “B-to-A conversions” fall outside of the MIRH strategy, which aims to keep rents at an affordable level, and could be better described as a “buy and hold” or core strategy than a value-add strategy.

Over-demanded and Under-supplied

Housing supply shortfalls and a widening wealth gap in the U.S. are creating positive conditions for MIRH performance.

As we outlined in our recent report The Future of Housing, housing supply growth has been tepid for much of the last decade. Between 2010 and 2020, nearly 10 million new households were formed, but only 4 million net new housing units were delivered in the U.S. This was primarily due to fallout following the Global Financial Crisis when many homebuilders were shuttered.

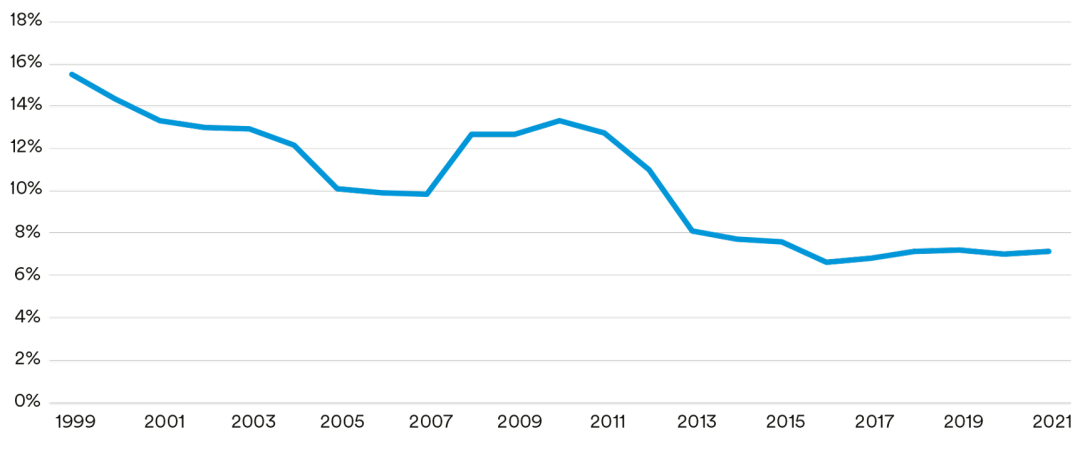

Among the housing units that have been built, most have been geared for higher income households. Construction of moderately sized and affordable homes has rapidly declined over the past 30 years. In the single-family space, for example, homes below 1,400 square feet made up 16% of all new construction in 1999 but made up just 7% of construction in 2021 (exhibit 1). A similar trend is observable in the multifamily sector.

Exhibit 1 | Moderately Sized Homes (<1,400 sf) as Share of Total Single Family Construction

Source: MIM, Census, September 2022.

Due to a number of factors including rising income inequality in the U.S., a large pool of rental properties have gone mostly unnoticed by the institutional investor community. Orlando serves as an instructive example.

Median household income in Orlando averages roughly $70,000. A family earning the median income would need to spend less than $1,600 on rent to avoid the categorization of rent burdened. Apartment properties in Orlando that were completed over the last 10 years rent for an average of $2,100 today (with 2- or 3-bedroom units suitable for families renting for closer to $2,300). This rent level is at least 25% above what would be considered an affordable level for the median income household, and implies most newly constructed market-rate housing is out of reach for many residents.4

Taken together, we believe a deep pool of renter demand coupled with a limited supply growth creates a strong investment case for MIRH.

Attractive Risk-adjusted Returns

Given specific definitions of MIRH do not exist, historical investment performance is unavailable in as robust of a manner as other property types or sub-types. Still, we believe the evidence that does exist suggests strong risk-adjusted returns.

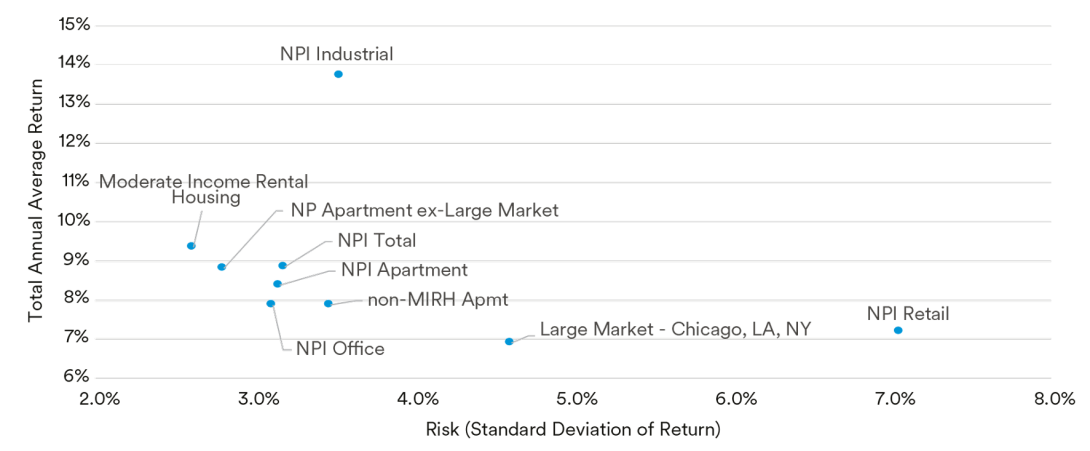

One relevant study was produced by Mark Roberts and Jake Wegmann from Southern Methodist University and the University of Texas at Austin. The study reviewed data from the National Council of Real Estate Investment Fiduciaries (NCREIF) and considered the performance over time of apartment properties that are affordable to residents earning 80% of area median income.

The study was able to show that between 2011 and 2021, MIRH produced absolute returns that out-performed all core property types except for the industrial sector, with the lowest level of volatility (exhibit 2).

Exhibit 2 | NCREIF Property Sector Risk and Return

Source: Jacob Wegmann and Mark Roberts using data from Bloomberg, NCREIF

10 Years as of 2Q2021

Several factors could explain this outperformance, including:

- Limited new construction coupled with attractive demand conditions, as outlined above.

- Moderate income renters may be renters by necessity, not renters by choice. As such, this category does not compete with the for-sale housing market. This could lead to both higher rent growth and lower volatility.

- Renters in this category may move less frequently, which could lead to lower turnover costs and vacancy volatility.

We expect industry definitions of MIRH to continue to evolve, and to solidify. Indeed, as of this writing, NCREIF has coordinated a task force to set firmer guidelines. Growing transparency of returns will shed more light on performance, but preliminary evidence makes a compelling investment case.

Geographic Strategies

As we outlined above, developers have been unwilling to construct housing accessible to moderate income earners. The rising cost of construction is one potential culprit. We estimate new residential construction costs a minimum of $200 per square foot. Assuming a 1,500 square foot 2-bedroom apartment, a 4% cap rate, and 100 bps development profit, the lowest possible rent for newly developed housing is $2,100, generally out of reach for those earning 60% to 120% of median U.S. household income.5

As a result, and absent legislative change that lowers construction costs, the primary source of new MIRH supply is older housing stock that is functional, but no longer in competition with newly developed residences. This can inform market targeting strategies for MIRH investments.

Markets where a significant portion of the housing stock is newly constructed likely have a shortage of MIRH and could produce better MIRH rent growth. Examples include Austin, where the average age of housing units is 26 years, Orlando (30 years), Phoenix (31 years), Atlanta (31 years), and Charlotte (31 years).

Examples of markets with a larger stock of competitive MIRH supply (which could lead to relatively lower rent growth) include New York (64 years), Boston (61 years), Philadelphia (58 years), San Francisco (56 years), and Los Angeles (55 years).6

This is a somewhat counterintuitive result since many of the markets with newer housing stock are considered lower cost of living markets. However, given the influx of higher wage earners to low-cost of living markets and rapid rent growth over the past several years, many markets across the U.S. sunbelt find themselves in significant need of affordable market rate housing for renters earning at or modestly below area median income.

Risks to MIRH

Challenges to the outlook for moderate income rental housing performance mainly center around the political outlook. Housing has been a politically sensitive topic for decades, and the category of renters that underpin this strategy is increasingly in the regulatory spotlight at the federal, state, and local level, rightfully so. Legislation that restricts rent growth or causes an acceleration in supply growth for moderate income housing could cause us to re-visit our views. However, given the current gridlocked political climate, we believe the U.S. may be a decade or more away from offering an adequate amount of housing to low- and moderate-income renters.

Conclusion

We expect favorable performance to persist for rental housing geared for moderate-income residents, who are facing worsening wealth inequality and limited supply of attractive and affordable professionally managed housing options.

In addition to the positive outlook for fundamentals, best estimates of performance history imply moderate income rental housing has been an outperforming property type in recent years. We expect that as industry definitions solidify, and transparency improves, more institutional investors will allocate capital to this strategy, which could cause yields to compress in the medium-term.

Lastly, while we believe the investment case is strong, MIRH has the added benefit of increasing the sustainability of a community by supplying housing for some of its most critical members. These include teachers, police officers, healthcare workers, sanitation workers, and others. In our view, neglecting the housing needs of these groups is already having negative consequences for some metropolitan areas7 , and this could expand if affordability continues to worsen. MIRH therefore has the benefit of potentially helping investors improve the sustainability component of their ESG goals, while also offering investments with attractive returns, in our view.

Endnotes

1 https://archives.huduser.gov/portal/glossary/glossary_all.html

2 https://sfrb.org/article/summary-ab-1482-california-tenant-protection-act-2019

3 MIM, NCREIF. October 2022.

4 MIM, CoStar, Census. October 2022.

5 MIM, NCREIF, Census. October 2022.

6 Census American Community Survey. October 2022.

7 https://www.miamitodaynews.com/2022/07/19/new-council-to-help-hospitals-universities-deal-with-nursing-shortage/ “A lot of nurses can’t even find affordable housing to come here and work, graduate from [a university] be able to work and live there.” -Florida representative Marie Woodson.

Read more from MetLife

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”) solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets. In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor. This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK. MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. About MetLife Investment Management MetLife Investment Management (MIM)1 serves institutional investors around the world by combining a client-centric approach with deep and long-established asset class expertise. Focused on managing Public Fixed Income, Private Credit and Real Estate assets, we aim to deliver strong, risk-adjusted returns by building sustainable, tailored portfolio solutions. We listen first, strategize second, and collaborate constantly to meet clients’ long-term investment objectives. Leveraging the broader resources and 150-year history of MetLife provides us with deep expertise in skillfully navigating markets. We are institutional, but far from typical. For more information, visit: investments.metlife.com © 2022 MetLife Services and Solutions, LLC. For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such). For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414. For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities. For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/ or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC and MetLife Investment Management Europe Limited.