The private placement market offers additional risk reduction and diversification that can help investors at any stage of the economic cycle. Private placements have more robust covenant packages and better recovery rates than public bonds—as well as higher yields. As credit markets face late-cycle headwinds, better downside protection and lower risk become especially attractive to insurers.

CONTEXT ON THE PRIVATE PLACEMENT MARKET

Private placements are bonds that are sold only to qualified institutional buyers (QIBs), offering another avenue for issuers to raise capital.* These bonds are sold through customized transactions that are negotiated privately between the issuer and investor.

Companies might choose to issue private placements for a number of reasons. Because US Securities and Exchange Commission (SEC) registration requirements don’t apply to the asset class, issuers and investors can maintain financial privacy. Issuers may prefer the flexibility of private placements, which don’t require minimum benchmark issuance size or standard maturities. They also offer accommodating and tailored funding options. Companies that issue in this market are often looking to diversify their funding base away from banks.

Investors are drawn to this market because of its unique risk- reducing qualities, enhanced return potential and the additional sector exposure that private placements offer—sometimes to otherwise inaccessible industries. These attributes are especially attractive as we move later in the credit cycle, when managing downside risk, diversifying sources of risk and income, and effectively navigating credit events are critical objectives.

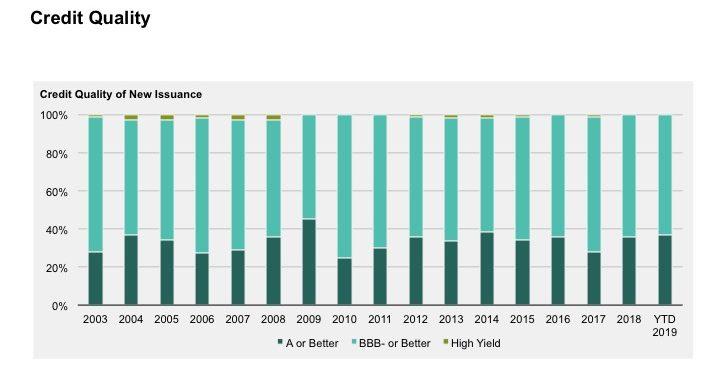

Private placements are typically investment grade: in each of the past 15 years, more than 96% of new-issue private placement bonds were rated BBB– or higher. What’s more, these deals are often brought to market as part of an “agented deal,” with a bank usually serving as the agent, or are originated directly by an asset manager or insurance company. Because agented deals are typically market clearing, they benefit from a higher level of scrutiny.

Most private placement investors are life insurance companies, which typically have longer-term liabilities and less need for liquidity. Given that most private placements are fixed rate, less liquid than public bonds and often held to maturity, they’re appropriate for investors with longer-dated liabilities, like insurers and pension funds.

Bonds are issued in maturities that generally range from five to 30 years, but the overall market is longer dated. Longer-duration instruments like these can help life insurers match assets and liabilities.

A STEADILY GROWING MARKET

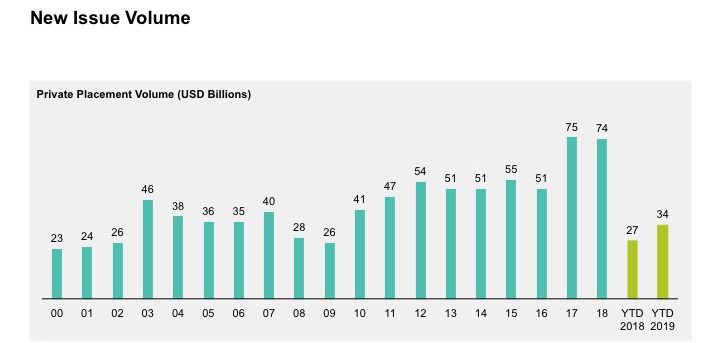

The private placement market is large and very mature. Even though it’s much smaller than the public US corporate bond market, it has been growing steadily. Over the past 20 years, new-issue volume has increased, as companies have shown more interest in diversifying their funding sources. During each of the past seven years, new-issue volume topped US$50 billion, more than doubling the yearly issuance seen at the turn of the century (Display 1).

Display 1: Steady Growth In Private Placements

As of July 8, 2019 | Source: Thomas Reuters (2007 through 2016, Bank of America Merrill Lynch (2019)

As of July 8, 2019 | New deals by dollar amount | Source: Bank of America Merrill Lynch

As 2017 gave way to 2018, issuance in the market was tempered by political uncertainty—particularly regarding US tax reform. At the same time, lingering effects of the global financial crisis also weighed on new supply, with fewer 10-year private placement bonds coming to market for refinancing. But even with this drag, new-issue volume over both years surpassed US$70 billion, setting a record high for annual private placement issuance and further illustrating the market’s healthy pace of growth.

GLOBAL APPEAL FOR INSURERS

Private placements have been garnering more and more interest from investors around the globe. The two private placement markets in Europe, the Schuldschein and euro private placement, have grown over the past few years, even though they’re still on the smaller side relative to the US private placement market.

European markets have more regulatory standards to contend with, such as Solvency II and country-specific requirements, and these can be hard to navigate. They also have more diverse investors, including insurers, as well as banks, asset managers and other QIBs. Because investors’ needs vary, these markets have fewer investment offerings with the specific features that appeal to individual insurers.

That’s why the US private placement market has continued to entice offshore investors—particularly insurers. This market is the largest and most mature, and because its investors are primarily life insurance companies, they all have broadly similar investment guidelines and risk appetites. In response to those common needs, issuers focus on the precise characteristics that are attractive to insurers (Display 2).

Display 2: Characteristics Of The US Private Placement Market

Source: AB

Investors in Europe are also drawn to the US market because— relative to European private placement markets—it offers longer maturities, better covenant packages and exposure to additional names. Many publicly traded European companies choose to issue in the US private placement market as well, seeking access to a broad group of different QIBs without having to file with the SEC.

PROTECT, RECOVER, DIVERSIFY AND ENHANCE

Because private placements offer unique risk mitigation, diversification and yield enhancement, they can be a strong complement to an investor’s public investment-grade corporate bond allocation.

More Downside Protection: Private placements have better covenant packages than those available in public transactions. Covenants are agreed-upon conditions that an issuer’s business must follow in order to increase the likelihood that it will repay its bond investors.

Because of these more rigorous covenants, private placements provide investors with material downside protection from shareholder-friendly activities such as leveraged buyouts, acquisitions and share repurchases, as well as general industry or credit-market deterioration.

While issuers can request to waive covenants, investors can refuse the request or can choose to renegotiate more favorable terms, possibly with additional fees. For long-term buy-and-hold investors, this protection is especially appealing.

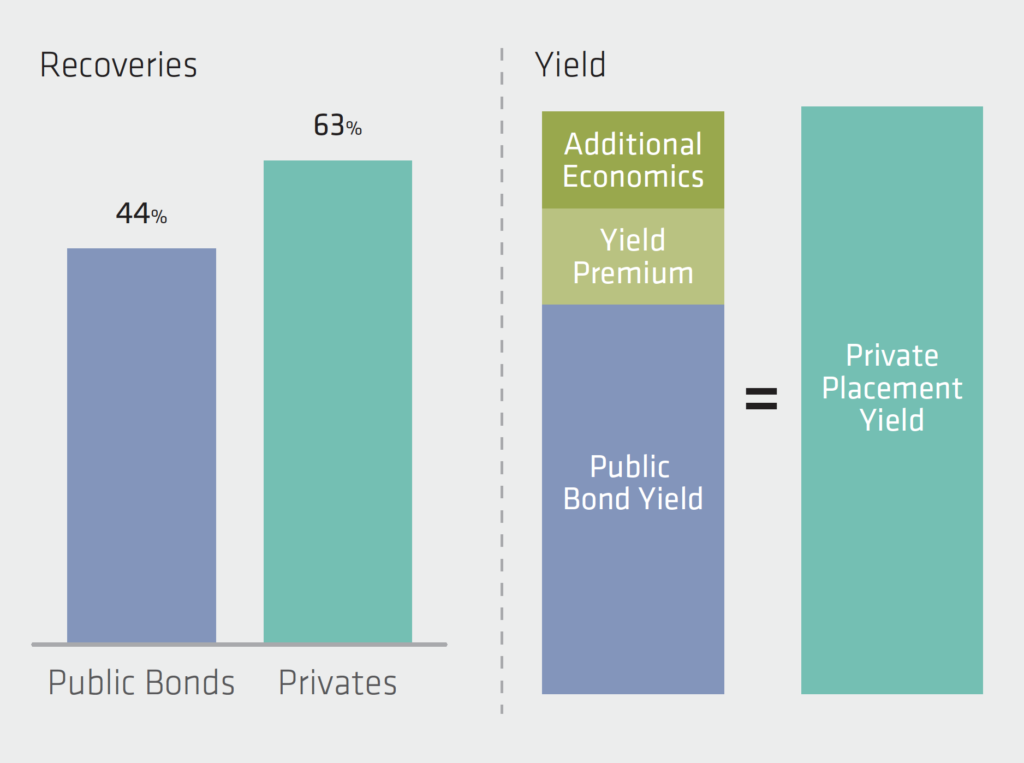

Better Recoveries Than Public Corporate Bonds: Private placements have consistently experienced higher recovery rates than public bonds. In addition to including covenants, private placement bonds are issued on pari passu terms—meaning they have equal priority—with other senior debt obligations. These traits help private placement investors maximize recovery during instances of default or bankruptcy, allowing them to receive make- whole payments or to return to the bargaining table to improve the conditions of the investment agreement.

Because the market is private, independent data on recovery are limited. However, a study by the Society of Actuaries shows that private placement recoveries (63%) consistently exceeded those of public bonds (44%) during the period between 2003 and 2012 (Display 3). These numbers show that the amount recovered by private placement investors was 43% greater than what public investors were able to recover.

Display 3: Better Recoveries And Higher Yields

Private Placements vs. Public Bonds Between 2003 and 2012

As of June 30, 2018 | Source: Society of Actuaries and AB

Effective Diversifiers: Adding a private placement allocation to a public credit portfolio may capture sector exposures not available through publicly traded bonds. Private placements are diversified in terms of duration and ratings, but issuers are also diversified by size, geography and industry.

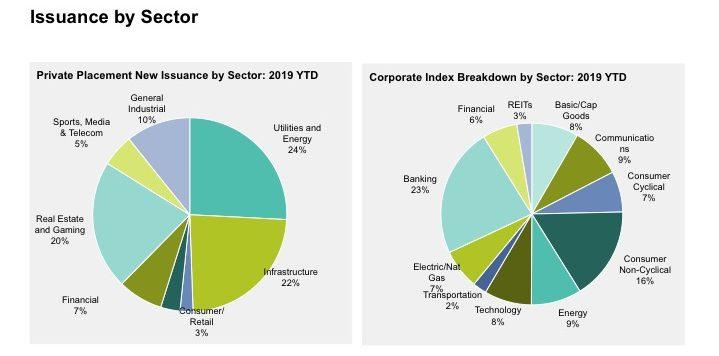

Public credit portfolios have more exposure to financials. The private placement market has limited financial sector exposure—it’s more heavily weighted toward industrials and utilities (Display 4). These sectors typically have greater visibility and better recovery rates during downturns. The private placement market also allows access to industries that aren’t available to the public, such as sports and infrastructure.

Display 4: Sector Issuance Trends

Private Placements Are Heavily Weighted Toward Non Financials, Such As Industrials and Utilities, and Include Nonpublic Sectors

Left displays as of July 8, 2019, right display as of July 25, 2019 | Numbers may not total 100% due to rounding. | Source: Bank of America Merrill Lynch, Bloomberg Barclays and AB

Opportunities to Enhance Income: Private placements offer higher yields than public bonds with identical credit ratings and maturities (Display 3). Yields on new private placement bonds are often significantly higher than those of their public counterparts. That yield boost comes from the illiquidity premium in private transactions. And given that illiquidity is less of a concern for insurance companies with long-dated liabilities, this yield boost is even more attractive.

Even if a private placement bond is called by the issuer or experiences a default that cannot be waived or amended, covenants (such as make-whole pre-payments) help investors regain initial yield over the rest of the bond’s term, with upfront above par take out. Additional income can also come in the form of coupon bumps or fees to waive or amend covenants. These advantages are in sharp contrast to the experience of public bondholders—deteriorating situations often force investors to sell at a loss or lead to restructuring.

HOW AB INVESTS IN PRIVATE PLACEMENTS

AB’s relative-value approach seeks to deliver a high return by maximizing income—taking advantage of illiquidity premiums and other yield enhancers. We also focus on minimizing downside risk by being selective in a universe of carefully researched private placement bonds.

We employ ongoing research and monitoring to take advantage of other possible return sources from private placements. These include make-whole payments and fees paid by issuers to modify covenants. The less liquid nature of private placements leads many investors to focus on squeezing the most income out of this sector, but our approach also includes capitalizing on as much non-bond income return as possible.

We start by sourcing new deals, then tapping the top-down and bottom-up fundamental research of our economic and credit research teams.

We stay in active dialogue with broker/dealers who specialize in originating private placement transactions. This communication is important because the market is relatively small, with a fairly defined group of institutional buyers generally well known to issuers and their agents.

AB has deep experience and expertise and a varied client base with a regular appetite for new deals. We’re selective in our deals; we’ll only purchase one when we’re comfortable with its covenant package and relative value versus public bonds.

This disciplined approach was validated during the 2008–2009 credit crisis, when we had fewer amendments to our deals and fewer workouts than our peers. The crisis was also the only time in the past decade where one of the issuers we invested in defaulted—and we recovered 77%. In comparison, public market issuers in the same industry had a recovery rate in the mid-20s.

THE ROLE OF PRIVATE PLACEMENTS IN A PORTFOLIO

Private placements offer more downside protection than the public corporate market, as well as valuable issuer and sector diversification. They can also enhance the risk-adjusted return profile of a core fixed- income portfolio. Because private placements are fixed rate and less liquid, they’re especially attractive to insurers and pension funds, which generally have long-term liabilities. In exchange for sacrificing some liquidity, investors receive strong covenant protections.

These covenants provide opportunities to enhance portfolio yield and generate more income. They also allow private placements to offer unique risk-reduction characteristics that are not available to public bonds. These characteristics are particularly appealing when late-cycle volatility hits credit markets. Along with these covenant packages, private placements are issued pari passu with other senior debt, giving them superior recovery (relative to public bonds) during default or bankruptcy. The private placement market also has less exposure to financials sectors than public credit does, as it’s concentrated more in industrials and utilities, which tend to fare better during periods of market stress.

Download PDF Reprint

By AllianceBernstein

Private Placements Team, Originally Published February 2019

Our Private Placements Team

AB has been managing private placement since 1971, making us one of the longest-tenured investors in the US market. As a core component of our US$150 billion dedicated credit platform, we manage US$9 billion in private placement assets, of which US$5 billion are Regulation D (as of June 30, 2019). We’ve built a widely resourced team to focus on credit investing globally, and we’re deeply committed to remaining leaders in this space.

Amy Judd, Director of Private Placements, leads the team. Amy has worked in the industry for more than 30 years, 18 of them with AB. She’s supported by a group of dedicated and experienced analysts with expertise in underwriting, restructuring and portfolio management. Our analysts monitor all portfolio investments continuously, and closely track industry trends that could impact issuers in our portfolios. Because our analysts work only with private placements, they can receive and act on nonpublic information.

A WORD ABOUT RISK

Fixed-Income Securities Risk. Investment in the fixed-income portfolios entails certain risks. Investment returns and principal value of these funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The value of underlying fixed-income investments of a portfolio can vary dramatically, in response to the activities and results of individual companies or because of general market and economic conditions and changes in currency exchange rates. The value of a portfolio’s investments may decline over short- or long-term periods. Specific fixed-income risks include interest-rate risk, lower-rated and unrated investments risk, prepayment risk, sovereign debt obligations risk, corporate debt risk.

IMPORTANT INFORMATION AND DISCLOSURES

This material is provided for informational purposes only

Under no circumstances may any information contained herein be construed as investment advice. This material is not an offer for the purchase or sale of any financial instrument, product or services sponsored or provided by AllianceBernstein L.P. (AB). The information contained herein reflects the views of AB or its affiliates and sources it believes are reliable as of the date of this publication. AB makes no representations or warranties concerning the accuracy of any third-party data. The views expressed herein may change at any time after the date of this publication. Investors should discuss their individual circumstances with the appropriate investment professionals before making any investment decisions.

Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA -Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as “wholesale clients,” as defined in the Corporations Act 2001 (Cth of Australia), and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Important Note for UK and EU Readers: For Professional Client or Investment Professional use only. Not for inspection by distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P. © 2019 AllianceBernstein L.P., 1345 Avenue of the Americas, New York, NY 10105

19–0320195515 FI–7797–0319