In 2004, Kofi Annan, then secretary-general of the United Nations, invited 50 financial institutions to endorse a report titled, Who Cares Wins. In it, Mr. Annan concluded companies that are well managed with regard to environmental, social, and governance (ESG) issues should compete more successfully and increase shareholder value. Those that don’t might not be able to weather regulatory changes or stakeholder actions. In addition, such businesses tend to miss growth opportunities such as accessing new markets.

Who Cares Wins reminds us responsibly-managed companies should contribute to a “sustainably-managed society.” To some, this sounded a lot like the many failed Economically Targeted Investment programs of the same era, which encouraged consideration of a “double bottom line.” On the contrary, Who Cares Wins argued there should be a direct relationship between good ESG management and good financial management. But it has taken more than a decade for thought leaders to explain how this relationship might work. From this report emerged the United Nations Principles for Responsible Investment (UNPRI) in 2006.

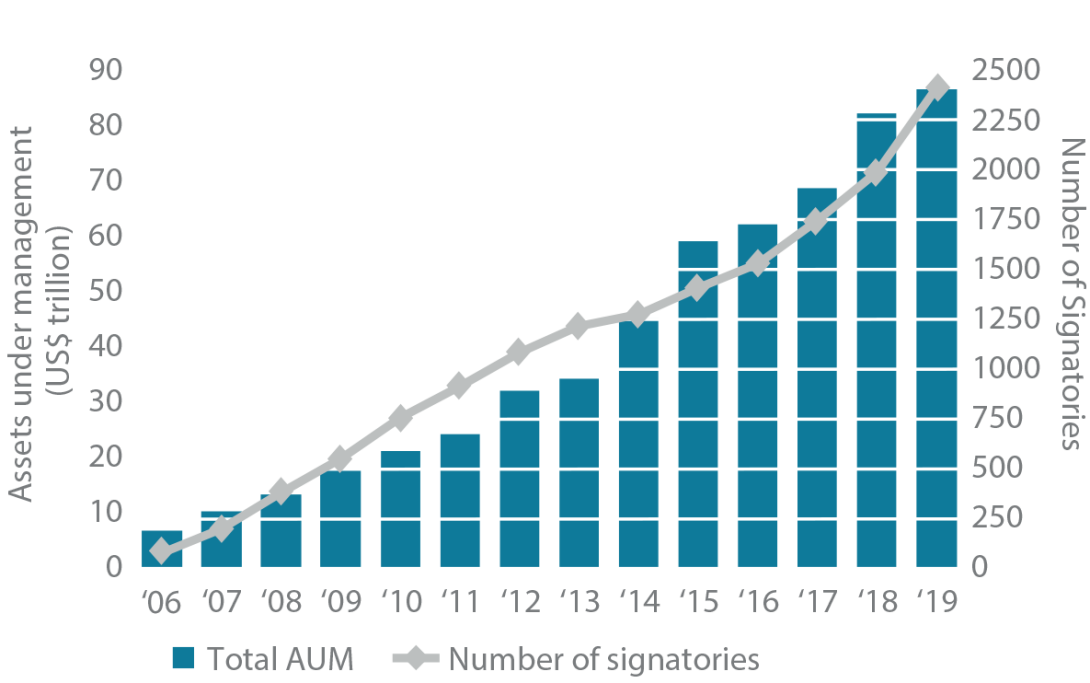

The UNPRI consists of six principles designed to align investors with “broader societal goals.” These principles form the conceptual scaffold around which signatories might build their internal ESG processes. The adoption of these principles has been noteworthy: from 100 at the outset to more than 2,300 today, including some of the largest asset managers in the world (Figure 1). While today’s headlines reflect plenty of disagreement about what the “broader societal goals” should be, the growth in adherents to the UNPRI mirrors a broader consensus that market failures are not as uncommon as some investors might like to believe.

FIGURE 1 | PRI SIGNATORY GROWTH

Source: United Nations, March 2019.

Secretary-General Annan was not the first to suggest companies could do well by doing good. The search for a relationship between ESG and corporate financial performance (CFP) traces back to the 1970s. Scholars and investors have published more than 2,000 empirical studies and several review studies on this relation since then. One paper has reviewed the findings of nearly all of them.1 Roughly 90% of studies reviewed reported a positive relationship between ESG and CFP. Moreover, the positive ESG impact on CFP appears stable over time.

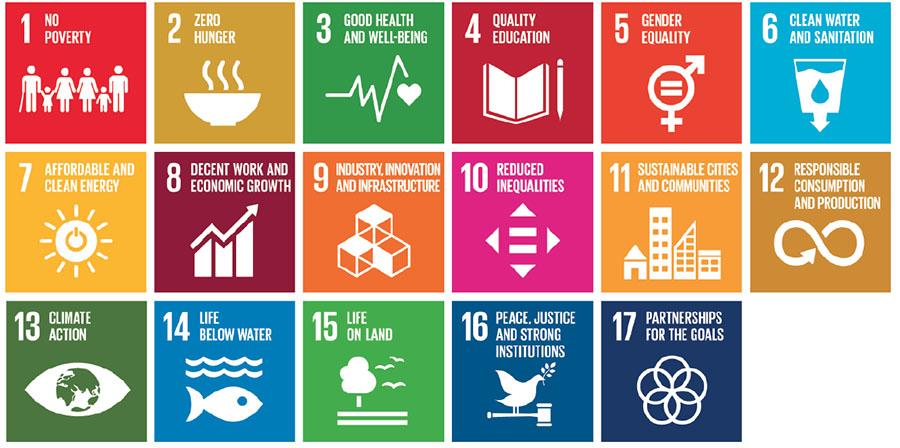

Eleven years after Who Cares Wins, all UN member states adopted the 2030 Agenda for Sustainable Development. This document provides a “shared blueprint for peace and prosperity for people and the planet.” At its heart lie 17 Sustainable Development Goals (SDGs), which are based on the premise growth can better be achieved by alleviating poverty, reducing inequality, addressing climate change, and transitioning to a low-carbon economy (Figure 2). In essence: Growth needn’t be a zero-sum game.

The revolution in information and communication technologies has resulted in more and better data becoming available. These data allow us to view the complex world of ESG issues with greater clarity, to pinpoint where markets are failing to match costs with benefits. In the past we might have argued these externalities did not exist, were too complex to price, or were best resolved through a market-based pricing mechanism (e.g., carbon pricing).

Today a generational change is occurring. Millennials outnumber Baby Boomers, and a US$30 trillion intergenerational wealth transfer is underway. Armed with greater political power and financial resources, Millennials are elevating their values and seeking out offerings that match. Pension fund portfolios are no exception. Their members do not want nameless investments; increasingly, they want to understand the story behind the investment and to see concrete results—whether tackling climate change, preserving woodlands and waterways, or empowering marginalized groups. According to one recent study, sentiment for responsible investing among public pensions grew to 92% in 2019 from 70% the year prior; among corporate pensions, sentiment rose from 56% to 86%.2

Information technology increases awareness of market failures, such as pollution, climate change, social injustice, and corporate malfeasance. A growing population of voters and consumers takes note of these issues. The power of social media allows influencers to galvanize grass-roots support for change in a way that simply wasn’t possible even 10 years ago. Swedish teenage activist, Greta Thunberg inspiring millions to march for climate change is a case in point. The combined effect of these forces has engendered a number of movements to shed light on these complex issues.

FIGURE 2 | SUSTAINABLE DEVELOPMENT GOALS

Source: United Nations.

» Britain’s Modern Slavery Act of 2015 brought social issues to the forefront and served as a model for other countries to pass laws that aim to eliminate forced or coerced labor. Australia followed in 2018. Still, an estimated 40 million people are living in modern slavery today.

» An Intergovernmental Panel on Climate Change special report compelled greater efforts to limit temperature rise to 1.5 degrees Celsius (versus 2.0 degrees).3 Together, with the Task Force for Climate-Related Financial Disclosures, the two groups have kept environmental considerations front of mind for investors.4

» In September 2019, the UN issued the Inevitable Policy Response. It forecasts governments will be forced to accelerate their action on climate change—an inevitability that has so far gone unaccounted in asset prices.

» Matters of governance received renewed attention when the Business Roundtable declared corporations should be the benefactors of all stakeholders, not just shareholders.5 This alters the focus of the corporation from the purist mantra of shareholder value creation that has dominated thinking in listed and unlisted companies alike.6

» The acquisition of Vigeo Eiris by ratings agency Moody’s heralds a formal move to price ESG factors into asset values.7

Read section: Responsible Investing in Motion here

StepStone Philosophy

Just as we have gone back to the powerful root concepts laid out in Mr. Annan’s seminal Who Cares Wins, we believe it is important to explain the foundation of our approach. We share Mr. Annan’s belief that effective management of ESG issues increases shareholder value. We also believe regulators, markets, and consumers are going to find ways to recognize externalities and more effectively allocate costs and benefits. Externalities are market inefficiencies. Historically they have persisted because of the lack of information or market mechanisms to recognize them. As this information becomes more available, private markets are well positioned to benefit from the arbitrage of these inefficiencies—identifying them and working to eliminate them. GPs and LPs ignore these factors at their peril.

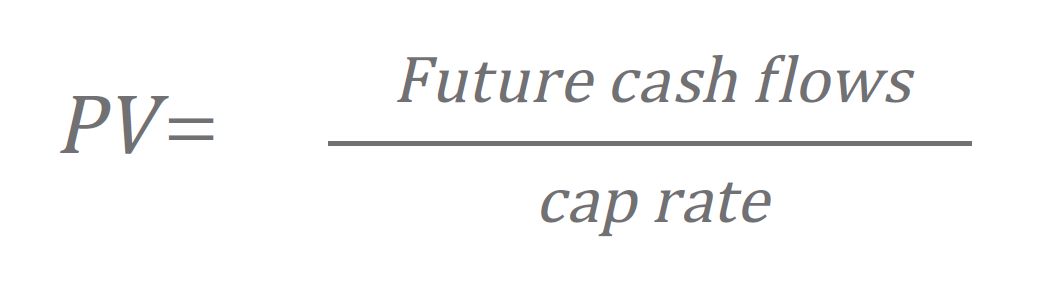

Our philosophy can be reflected through the equation for the value of a perpetuity, which states the present value of an asset reflects the net present value of its future cash flows:

Where the cap rate is the difference between the discount rate and the growth rate.

Typically, private market investors think about ESG as affecting the numerator—reducing waste in inputs increases profits; reducing pollution avoids potential environmental liability; or worker safety and labor relations trade higher costs in the short term against more stable and productive workforces in the long term. These are important considerations that fall well within the value-creation mindset of active shareholders. The bigger impact on value, however, is in the denominator. This is where multiples are determined. Understanding how ESG can affect the discount rate is the key. For example:» In the retail sector, businesses with sophisticated supply chains that “track to source” and do not work with vendors that use forced or coerced labor are more highly rated.

» In response to consumer demand, large American fast food companies discarded battery chickens in favor of the freerange variety. A frenzy of asset purchases in the agriculture sector ensued as supply chains were reorganized. Suppliers of free-range eggs and hens were rerated while assets associated with battery chickens were priced as stranded.

» Upgrading an office building to LEED Platinum requires significant investment, reducing cash flow in the near term. But as weather becomes more extreme, energy costs rise, and consumer preferences shift, demand for LEED Platinum offices increases, reducing the cap rate for the property.

» Analyzing a port's climate-change preparedness may identify risks to the port's business and operations. Rising sea levels, for example, will affect the port's physical assets, as well as its catchment area. Investors weigh the extent to which ports have invested in climate resiliency, requiring a higher cap rate for ports that have underinvested or are located in areas that are particularly susceptible to rising sea levels.Some ESG factors (e.g., climate change) can be thought of as distinct risk factors, similar to inflation or interest rates. These are the most powerful ESG factors; they affect valuation multiples and cap rates, not just annual profit and loss statements. Incorporating these factors into investment underwriting is certainly not trivial, but the payoff to those who are able to could be significant.

As is the case with any risk decomposition, distinguishing ESG risks from some of the other risk factors can be tricky. For example, governance risk factors may be high in an emerging market country. In such a case, both sovereign and governance risks would be elevated. It is important not to double count or confuse what is driving risks. For example, Brazilian companies caught up in the Carwash scandal that started in 2014 would have exhibited both elevated governance and sovereign risks. Scrupulous companies that avoided the scandal would only register sovereign risk factors. The inefficiency comes when the market confounds the two; a careful private market investor would recognize the scrupulous company through careful ESG review. The market would price an investment in the company incorporating both governance and sovereign risk in the discount rate; however, as the competition was eliminated through the anti-corruption movement, the scrupulous company would increase its market share, and be rerated with a higher multiple. This is the type of inefficiency that a functioning ESG program can turn into superior financial returns.

The discount or hurdle rate also introduces a time consideration. In private markets, holding periods are often counted in years or even decades, rather than days or minutes. This is particularly important as we consider ESG factors, some of which manifest over an extended period. Pricing in such factors is important because they can materialize within the holding period. Investments made today could still be on the books a decade hence, when temperatures are expected to peak (hopefully). How resilient will such assets be under hotter conditions? How will the asset’s business strategy need to change? Whereas public markets may sell out of assets requiring a complex strategy shift to decarbonize their business plan, private ownership affords the opportunity for stewardship. Longer holding periods provide the opportunity to build revenue opportunities like carbon sequestration or a complete shift to renewables, which benefit from a long view of ESG factors.

As long-term investors, we need to recognize climate change, pollution, income inequality, and corruption as the externalities they are: a skew requiring future generations to subsidize the present through lower quality of life, higher taxation, and increased socio-political instability. As these externalities become more transparent, they will become easier to internalize—creating a link between ESG factors and financial returns.

We need to recognize climate change, pollution, income inequality, and corruption as the externalities they are.

GP Perspectives on ESG

If an investor has an ESG policy at all (many do not), they are likely to fall into one of the following buckets when it comes to ESG integration.

THE COST OF DOING BUSINESS

Some investors regard ESG integration as an additional task that is akin to a compliance cost. This can lead to a “tick-the-box” mentality, whereby ESG issues are not considered until the end of the due diligence to “tidy up” investment memos. In such cases, it is not uncommon to see ESG functions falling under the purview of the head of compliance.

HAPHAZARD APPLICATION

Other investors might give due consideration to ESG factors, but their approach lacks any systematic application. They do not label such considerations as ESG factors and may even go so far as to resist such nomenclature. Perhaps a root cause of this perspective is the mistaken belief that ESG considerations dilute profits or amount to a negative screen that reduces the manager’s investment opportunity set. This perspective may also be a residual effect from schools of thought that wrongly conflate ESG integration with concessionary impact investing (i.e., accepting a discount to commercial returns to achieve a non-financial objective). Some investors also confuse values with responsible investing, believing a moral compass is the same as ESG integration.

INTEGRATED APPROACH

Fortunately, a growing cohort of investors is embracing a structured ESG framework and working hard to integrate ESG factors into their investment processes. Yet even with this mindset, this group is encountering a number of challenges.

Challenges

In Who Cares Wins, measurement and disclosure are prominent themes. As the saying goes, “what gets measured, gets done.” Metrics are tangible. They create a feedback loop and quantify the externality. Without them, it is very difficult to effect change. But herein lies the rub: There is a natural tension between metrics that are tailored to specific business goals and standardization, which allows for peer group benchmarking.

We expect there to be greater standardization over time, particularly for headline metrics. Work to do so is already underway. For example, a landmark 2019 EU report establishes 67 criteria capital markets can use to determine whether an investment might mitigate climate change.8 Parsimony is not one of bureacracies’ virtues, as can be seen in the 17 SDGs and this complex taxonomy. This complexity, however, inures to the benefit of private market investors who can take the time to dig into the particulars.

Related to the challenge of deciding what to measure is the task of tracking and reporting on the chosen metrics. Data and process auditing is another ordeal entirely.

This discussion on metrics and measurement is very relevant to private markets, which have a long history of effecting change in their portfolio assets through active engagement. One of the dominant trends over the last five years within private equity is the rise of teams specializing in operational value add. Residing within the GP, these groups are akin to consulting firms. They are increasingly a critical component of the pitch private equity managers make to the companies they are targeting. A similar trend is underway in the infrastructure sector as well.

ESG slots well into active management because it provides a richer framework across which to drive operational change and improvement. The focus needn’t be limited to governance and strategic improvements. As private markets continue to become more competitive, improving, say, energy efficiency, will be more than a "nice to have." It will be a way to reduce costs and anticipate future policy responses to climate change and pollution.

As noted above, deciding on what to measure is fraught. Creating the systems to monitor and measure the chosen metrics has been lagging. The ability of GPs to measure a diverse array of metrics across their portfolios, as well as conduct benchmarking and scenario analysis is clunky and time consuming. But change is coming, and more service providers are moving into this space to help with this data management. Just as fiduciaries pushed their investment managers to make ESG a priority, they will push for better monitoring and reporting, which will characterize the next phase of responsible investing.

Conclusion

It has taken almost two decades for responsible investing to spill into the mainstream. We see no signs of the momentum abating and are hopeful that in another 20 years responsible investing will be the norm. Part of this optimism is rooted in the generational wealth transfer that is underway; future retirees will demand stewards of their capital contribute to a sustainably-managed society.

The other factor is the increased allocations to private markets where long holding periods and a proclivity for active management dovetail with the ESG agenda. As regulators, grass-roots activists, and other stakeholders uncover externalities, private market investors will be well positioned: Arbitraging inefficiencies is what we do. As capital markets both public and private become more efficient, thoughtful investors will want to care more about ESG as a way to identify inefficiencies to arbitage. As foreseen by Mr. Annan, who cares about ESG wins higher financial returns.

1 Friede, Funnar, Busch, Timo and Bassen, Alexander. 2015. “ESG and Financial Performance: Aggregated Evidence from More Than 2000 Empirical Studies.” Journal of Finance & Investments 210–233.

2 Aon. 2019. "2019 Global Perspectives on Responsible Investing."

3 IPCC. 2018. “Special Report: Global Warming of 1.5° C.”

4 UNPRI and TCFD have linked hands in the effort to drive adoption, both sharing a similar conceptual framework and recognizing the benefit of requiring signatories of UNPRI to adopt TCFD and vice versa.

5 Business Roundtable. 2019. “Statement on the Purpose of a Corporation.”

6 We would be remiss if we did not acknowledge that in Germany, the concept of Mitbestimmung—i.e., worker participation in a firm’s decision-making process—was codified in 1976.

7 Vigeo Eiris offers specialized research and decision-making tools for sustainable and ethical investments.

8 EU Technical Expert Group on Sustainable Finance. 2019. "Financing a Sustainable European Economy."

Read the full article here

This document is for information purposes only and has been compiled with publicly available information. StepStone makes no guarantees of the accuracy of the information provided. This information is for the use of StepStone’s clients and contacts only. This report is only provided for informational purposes. This report may include information that is based, in part or in full, on assumptions, models and/or other analysis (not all of which may be described herein). StepStone makes no representation or warranty as to the reasonableness of such assumptions, models or analysis or the conclusions drawn. Any opinions expressed herein are current opinions as of the date hereof and are subject to change at any time. StepStone is not intending to provide investment, tax or other advice to you or any other party, and no information in this document is to be relied upon for the purpose of making or communicating investments or other decisions. Neither the information nor any opinion expressed in this report constitutes a solicitation, an offer or a recommendation to buy, sell or dispose of any investment, to engage in any other transaction or to provide any investment advice or service.

Past performance is not a guarantee of future results. Actual results may vary.

Each of StepStone Group LP, StepStone Group Real Assets LP and StepStone Group Real Estate LP is an investment adviser registered with the Securities and Exchange Commission (“SEC”). StepStone Group Europe LLP is authorized and regulated by the Financial Conduct Authority, firm reference number 551580. Swiss Capital Invest Holding (Dublin) Ltd (“SCHIDL”) is an SEC Registered Investment Advisor and Swiss Capital Alternative Investments AG (“SCAI”) (together with SCHIDL, “SwissCap”) is registered as a Relying Advisor with the SEC. Such registrations do not imply a certain level of skill or training and no inference to the contrary should be made.

Manager references herein are for illustrative purposes only and do not constitute investment recommendations.