DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

On 17 December 2020, the European Insurance and Occupational Pensions Authority (EIOPA) published its final opinion on the 2020 review of the Solvency II framework, which had been requested by the European Commission (EC). EIOPA opines that whilst Solvency II works well overall, evolutionary improvements can be made in several areas.

This paper mostly focuses on the market related aspects of the opinion, including:

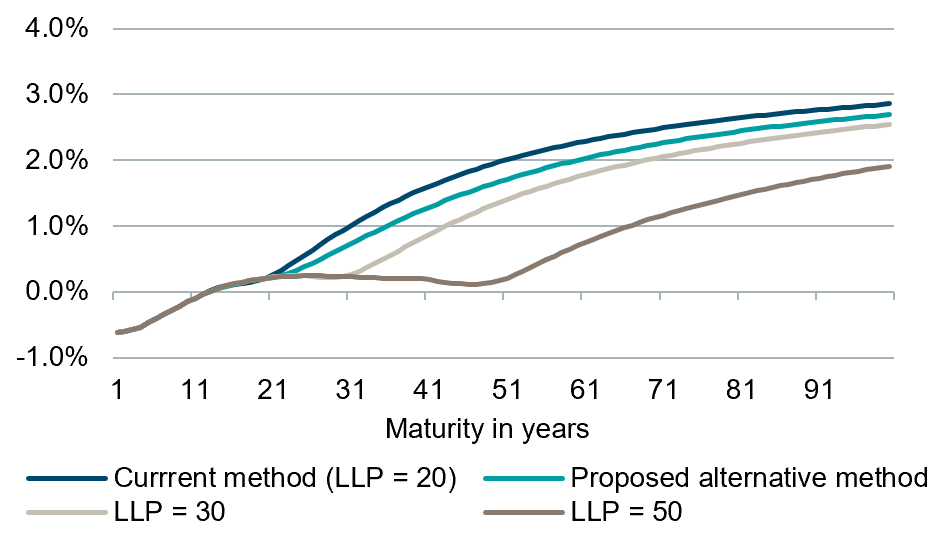

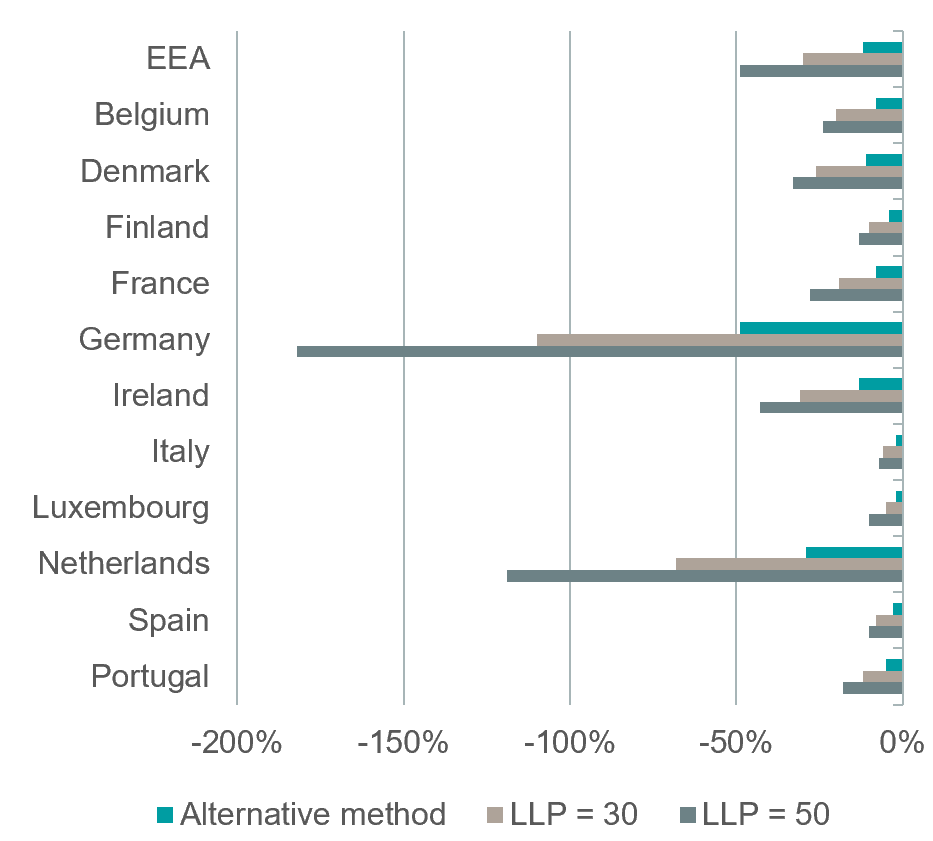

1. Extrapolation of the risk-free interest rates. The final recommendation includes only a moderate adjustment towards the lower benchmark swap rates reflecting the substantial impact this would otherwise have.

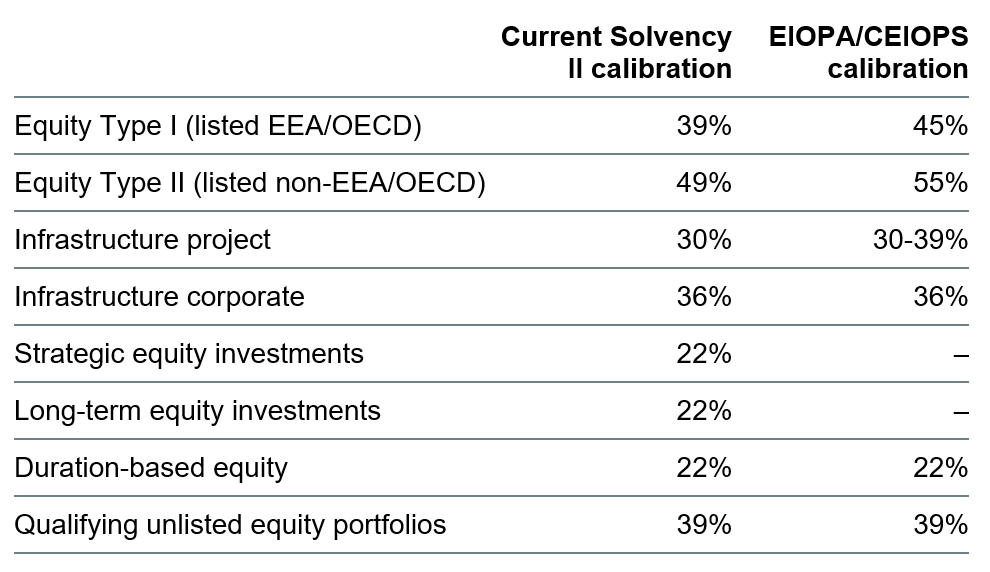

2. The Standard Formula for Solvency Capital Requirements (SCR). Notable changes include a more permissive long-term equity treatment, clarifications around strategic participations, widening the symmetric adjustment, and likely having the most quantitative impact, removing the interest rate down-shock zero floor.

3. Long-term guarantee measures. The Volatility Adjustment is substantially updated to be more relevant and less volatile while the Matching Adjustment is updated to allow diversification and clarify repacks.

Background

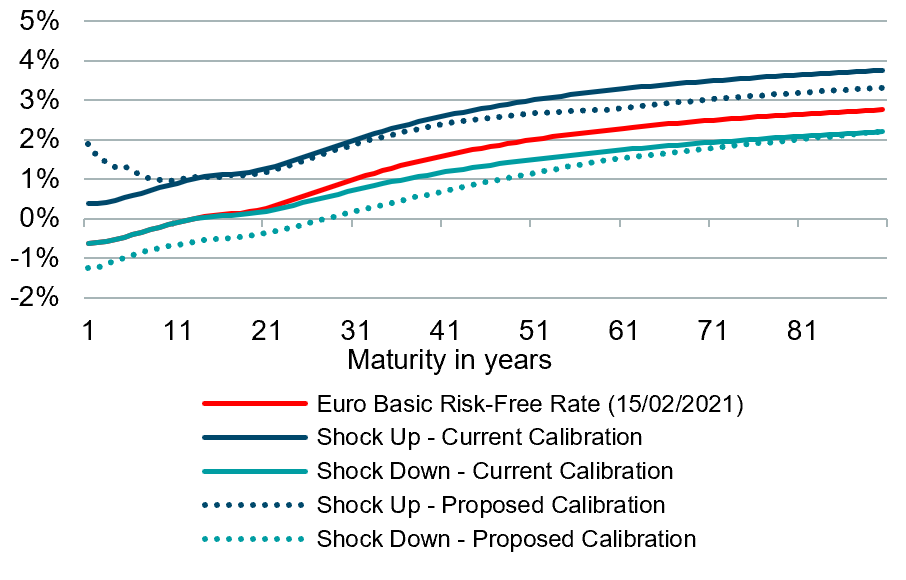

One of the most substantial changes in the publication relates to the calculation of the risk-free interest rate curve used in the valuation of liabilities. In general, the economic view of an insurer’s balance sheet is that policy obligations should be valued as if there were little to no possibility that the insurance company might default, i.e. to the system, they are risk free. Thus, from a theoretical perspective, all liabilities should be valued at a market risk free rate. The many practical problems of applying this theory directly has led to the adoption of the current method which blends market rates with a target long-term rate.

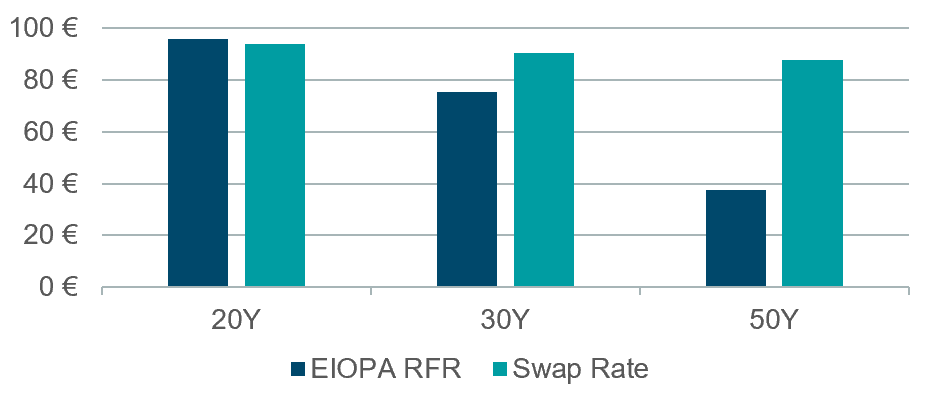

Under the current method, the Euro risk-free rates for maturities before the last liquid point (LLP) of 20 years are directly derived from swap rates. But after the LLP, interest rates are smoothly extrapolated towards a constant ultimate forward rate (UFR). Since swap market information past the LLP is not taken into account in this extrapolation, there can be a significant divergence (in particular, in today’s low interest rate environment) between the extrapolated rates and the actual swap rates. This divergence and the associated concern that the value of liabilities are severely underestimated (see Figure 1) is the basis for supervisory concern and EIOPA’s review.

In March 2019, the EC introduced a lower capital charge for specific long-term investments in equities. In order to qualify for the long-term equity (LTE) investment treatment, an equity investment must meet several requirements.

In fact, the LTE investment category can be considered as a revision of the duration-based equity risk (DBER) sub-module as both concepts aim to capture the risk of equity investments that are held for a longer period. In particular, the DBER sub-module can only be applied by life insurance companies that provide certain occupational retirement provisions or retirement benefits and that meet further criteria, such as a holding period of at least twelve years.

In contrast, the concept of LTE investments is less restrictive while in fact substantively capturing the same type of type of equity risk as the DBER sub-module. Hence, in order to reduce complexity, EIOPA suggests phasing out the DBER sub-module and refining the requirements for LTE investments (without imposing the same restrictions as for DBER investments) to accommodate this type of risk.

EIOPA proposes following changes and additions to the requirements for LTE investments, which may allow a broader and easier use of the LTE concept:

For life companies, EIOPA advises that the assigned portfolio of assets must back liabilities with high or medium illiquidity (see Volatility Adjustment) and that the Macaulay duration of these liabilities should exceed 10 years. Insurance Europe has criticizes this target duration as it is not in line with the average duration of most European insurers (6-7 years).

Non-life insurers have to demonstrate a sufficient liquidity buffer for the portfolio of non-life insurance liabilities and the assigned portfolio of assets. This is considered demonstrated if the ratio of high-quality liquid assets (backing all non-life liabilities and applying a defined liquidity haircut) to the non-life best estimate liabilities (net of reinsurance) is greater than one.

In addition to the general framework assessment for LTE, EIOPA also performed a quantitative calibration assessment of the reduced risk charge of 22%. This reduced charge had been set by the EC based on, among other things, the CEIOPS calibration of the DBER sub-module in 2010. However, when EIOPA used an adjusted version of this work for LTE investments, it could not corroborate the 22% charge. Despite this, EIOPA does not explicitly propose a change to capital charge.

Background

Like LTE investments, strategic equity investments can also benefit from a reduced capital charge of 22%. However, the motivation and justification for the lower capital charge is different. Whereas the motivation for the LTE charge reflects the idea that equities might hold lower risk over a longer investment period, the charge for strategic equity investments is based on the idea that it has some form of lower short-term risk. This can be both the nature of the investment and the influence exercised by the investor (the insurance company) over the related company. However, it has been difficult for insurance companies to demonstrate this reduced volatility.

Conclusion and Analysis

EIOPA suggests extending the ‘beta method’ already used for unlisted equity portfolios to strategic equity investments as one method to make this demonstration. The beta method is a static formula applied to fundamental data of target equity investments which estimates a market “beta”, or degree of sensitivity to general market movements.

Besides adding the beta method, EIOPA suggests the following clarifications:

Finally, since there was a concern that this would be viewed as the benchmark method instead of only one-of-many, EIOPA suggests introducing the beta method via additional guidance instead of a change in the legal text.

Technical details

For the beta approach, a strategic equity investment has a sufficiently lower risk if it has a calculated beta below 0.5641 for type 1 equities (22% over 39%) and below 0.4590 (22% over 49%) for type 2 equities. EIOPA specifies that the application of this method is restricted to investments in companies established in the EU or EEA with a majority of revenues generated in EEA or OECD countries. Additionally, it should have been larger than small-sized enterprises, as defined by the Commission Recommendation (2003/361/EC), for the last three years.

Background

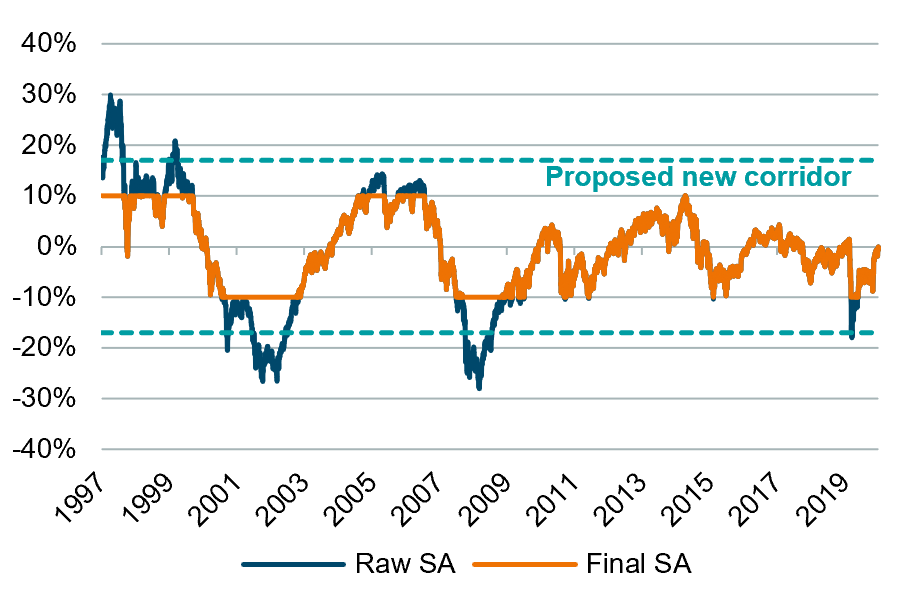

The symmetric adjustment is an additional variable capital charge published by EIOPA on a monthly basis ranging between +/-10%. The objective of the measure is to dampen the volatility of own funds resulting from changes in equity prices, thereby in particular reducing the risk of procyclical investment behavior of insurance companies (e.g. “fire sales”).

Conclusion and Analysis

EIOPA assessed both the calibration of the symmetric adjustment and the reference portfolio from which the adjustment is calculated.

EIOPA advises to widen the corridor boundaries of the symmetric adjustment from +/- 10% to +/- 17% and to introduce a floor of 22% to the equity capital charge. This was based on a positive qualitative assessment of the performance of the symmetric adjustment through the COVID-19 pandemic as an effective measure allowing flexible reaction in case

of deterioration of insurers’ financial position and a quantitative calibration review since the beginning of 2020 (see

Figure 5).

EIOPA concluded that there is no need to change the current reference index composition due to the high overall correlation among the main stock markets in Europe. Although the country weights of the index, which were set in 2015 based on the composition of the average equity holding of European insurance companies at that time, now have changed, it was not views as material due to the high correlations.

Source: EIOPA, DWS International GmbH. As of: 15 February 2021

Background

For bonds and loans, the spread risk SCR is determined as a function of the credit quality step (CQS) and modified duration with charges increasing both with CQS (i.e. deteriorating quality levels) and with duration. EIOPA evaluated the option to introduce a framework for lower capital charges for specific long-term investments in bonds and loans with similar conditions as for long-term equity investments.

Conclusions and Analysis

Ultimately, EIOPA does not propose any changes to the spread risk sub-module.

EIOPA concludes that there is no need to further incentivize (long-term) fixed income investments as:

Currently, Solvency II sets a uniform risk charge of 25% for all real estate investments irrespective of the type of property or its location. Due to limited market data available, the 25% capital requirement was calibrated solely based on data for the UK real estate market, which is deemed to be the most volatile property market in Europe. Hence, this was viewed as overly conservative and not representative for other real estate investments outside the UK.

Overall, EIOPA shares this view but does not see a sufficient improvement in availability of granular historical data, which would allow for a re-calibration of the existing shock for different real estate markets. Additionally, the impact of COIVD-19 would be expected to increase volatility, but EIOPA finds it difficult to quantify the potential impact on prices for residential and commercial real estate.

Background

Under the VA, insurance companies can add a spread to the risk-free discount curve in order to stabilize their Solvency II balance sheet in times of higher spread volatility. For each currency, the VA spread is derived from a representative portfolio of assets, which is updated by EIOPA on an annual basis largely using the average asset allocation of European insurance companies. The spread is calculated on a monthly basis and is adjusted by a fundamental spread, a spread measure that should reflect the long-term average default and downgrade risk of the underlying fixed income instruments in the representative portfolio (and not short-term liquidity effects or similar). Ultimately, 65% of the residual (i.e. risk-adjusted) spread is added to the risk-free discount curve. In times of a significant spread widening in a specific country, a higher VA spread based on a country-specific reference portfolio is applied. Overall, EIOPA has identified key shortcomings in the current design of the VA:

Conclusions and Analysis

Firstly, EIOPA advises to split the VA into a permanent VA and a macro-economic VA, which under the current framework correspond to the currency-specific VA and country-specific VA, respectively.

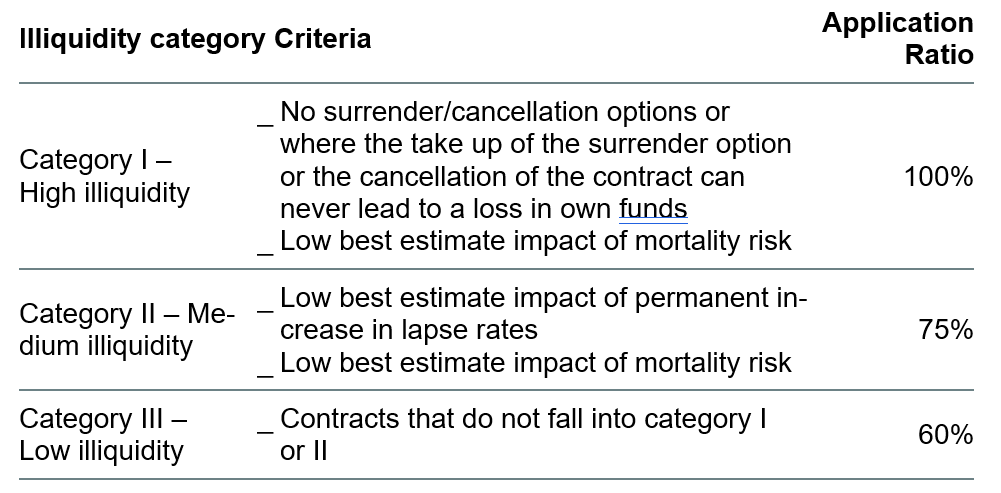

The permanent VA should become more company-specific by taking into account the illiquidity of liabilities and asset-liability matching features of the individual insurer. This is done by the means of two firm-specific application ratios. The first application ratio measures the degree of illiquidity of liabilities of a company, clustered into three categories of high, medium and low illiquidity (see Figure 7). Companies with a larger share of less liquid liabilities are allowed to make greater use of the VA.

Source: EIOPA. As of: December 2020

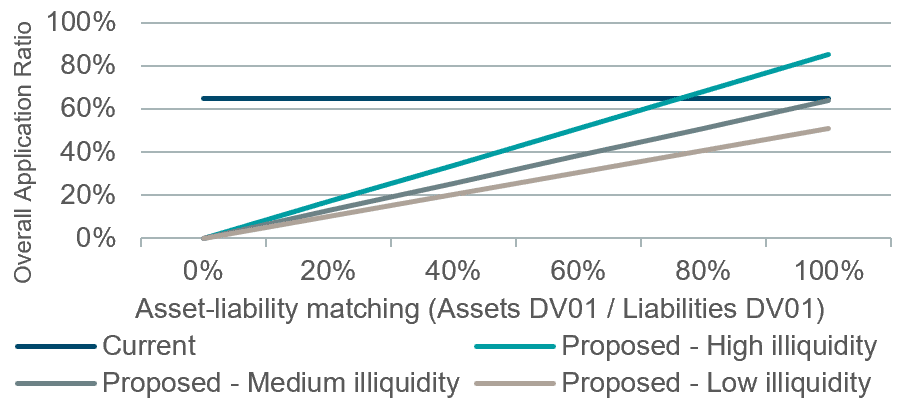

The second application ratio is based on the asset-liability spread-sensitivity matching of a company to reduce potential “overshooting” effects of the VA. Companies with well-matched sensitivities are allowed to benefit more of the VA. Since the introduction of the two firm-specific application ratios reduces some of the uncertainties and risks inherent in the VA, EIOPA suggests to increase the general application ratio for the VA from 65% to 85%. As outlined in Figure 8, only companies with a very high share of highly illiquid liabilities and well-matched assets and liabilities can benefit from a higher overall application ratio compared to the current general application ratio of 65%. Based on data provided by EIOPA, the average overall application ratio across Europe would be around 59%. The average illiquidity application ratio and the average asset-liability application ratio is 76% and 91% respectively. Especially, the illiquidity ratios differ significantly across countries. For example, very high values can be observed for Germany, France and Italy while low values are observed for the Netherlands in particular.

Source: DWS International GmbH. As of: February 2021

The macro-economic VA is a revised version of the country-specific VA. Under the current design of the VA, the country-specific VA is activated if the spread on the country-specific reference portfolio exceeds the spread on the currency-specific reference portfolio by 200% (relative trigger) and the country-specific spread is at least 85 bps over the risk-free rate (absolute trigger). In that case, the currency-specific VA is increased by 65% of the amount of the relative trigger spread (i.e. in excess of 200%).

Under the new macro VA, the relative trigger is reduced to 130% of the scaled risk-adjusted currency spread (the scale is based on the proportion of fixed income assets in the representative portfolio). The absolute trigger is reduced to 60 bps after which a linear activation of the country-specific VA starts. The full activation occurs at spreads over 90 bps. Overall, these proposed changes would make the macro-economic VA more likely to be activated due to lower triggers as well as more stable as the absolute trigger leads to a gradual activation rather than a binary outcome.

Finally, EIOPA proposes two other changes. First is a change in the current design of the risk correction. They propose decoupling the risk correction from the fundamental spread since analysis indicates a “sticky” risk correction with less reflection of recent changes in credit risks. Hence, they propose the risk correction be calculated as a fixed percentage of current spread levels but with an allowance for a higher VA impact when spreads exceed their long-term average. Overall, the new design of the VA would partially limit the benefit of the VA in times of widening spreads.

Second, EIOPA proposes that standard model users should not be allowed the usage of the dynamic VA. However, internal model users may still use the dynamic VA. This might disproportionately impact insurers whose asset allocation differs significantly from the reference portfolio.

In contrast to the VA, the MA has received relatively little attention under the Solvency II review. The MA is currently only used by insurance companies in the UK and Spain.

An MA portfolio is a separated portfolio of assets and liabilities in which cash flows are matched and assets assigned to that portfolio are exclusively devoted to cover the best estimate of the liabilities included in the portfolio. Like LTE portfolios, MA portfolios are subject to a “ring-fencing light” but not to a legal ring-fencing. Nevertheless, under current treatment, MA portfolios and legally ring-fenced funds are treated in the same way by not taking into account diversify-

cation benefits when aggregating the SCR across those and other portfolios.

EIOPA noted that this ring-fencing is not symmetric; while it is true that the assets in the MA portfolio cannot be used to cover losses outside the MA portfolio, other outside assets can be used to cover losses from the MA portfolio. Additionally, the assets in the MA portfolio only have to cover expected losses (best estimate) but not unexpected losses, which are covered by assets that back the risk margin and the SCR. Hence, EIOPA opines that a higher SCR resulting from limited diversification benefits cannot be justified and may discourage insurers from using the MA. In fact, there are examples where the loss of diversification in the SCR exceeds the increase in own funds resulting from the use of the MA in the calculation of the liabilities. Therefore, EIOPA advises to remove the limitations to the diversification between the assets in the MA portfolio and other assets in the SCR calculation. This is also in line with the methodology of most internal model users.

Besides changes to the diversification benefits, EIOPA has also reviewed the MA eligibility of restructured assets (i.e. assets that may have been restructured specifically to meet the MA cash flow requirements) and of assets with an uncertain timing of cash flows, such as callable bonds.

With respect to restructured assets (e.g. securitisation structures), EIOPA proposes to introduce a look-through approach to assess the eligibility of those assets. More specifically, restructured assets must meet the following conditions in order to be eligible for inclusion in a MA portfolio

Besides this, EIOPA also evaluated the option to allow MA eligibility for assets with uncertain timing of cash flows given that the MA benefit will be calculated based on the yield-to-worst. However, EIOPA decided to not follow this approach as it remains detrimental to the principle of cash flow matching.

Overall, EIOPA describes the proposed changes to the market risk module as an evolution rather than a revolution.

We would agree to this statement. In many aspects the review lacks revolutionary elements.

Nevertheless, some changes will still have a significant impact on the Solvency II balance sheet of European insurers. In our view, the most material changes relate to interest rates. Even though the proposed methodology for extrapolating the risk-free interest rate curve is only a small step towards greater realism of lower interest rates, it will still have a severe impact on the solvency position of insurance companies with long-dated liabilities. Additionally, the proposed increase of the downwards interest rate shock will result in a significant increase in SCR for companies that run larger duration gaps. Consequently, affected insurers will likely further increase their efforts in narrowing their duration gap by either increasing their asset duration and/or shortening their liability duration for new business and, where possible, for in-force business. For increasing the asset duration, companies may rely on both traditional asset classes such as government bonds or high-rated corporate bonds as well as on alternative assets such as infrastructure debt, government-guaranteed loans or residential mortgages.

A sound asset-liability management will also be encouraged by the proposed design of the VA, which will make this measure more effective for companies with well-matched assets and liabilities. However, the suggested changes to the risk correction may dampen the effect to a certain degree and will make the VA probably more volatile.

Besides this, potential changes to the long-term equity investments treatment may allow a broader and easier use of this concept across Europe instead of only the few countries, which have favourable liability structures. This may encourage further passive equity investments and in particular private equity investments where the capital benefit is the highest and the holding period is anyway rather long-term by nature given the illiquidity.

Nevertheless, in the end it is worth noting that EIOPA’s opinion is not binding. As we have already seen in the past, the European Commission (EC) may decide – e.g., for political reasons – not to follow EIOPA’s guidance in certain areas. In particular we have seen this with regard to changes to the interest rate shock previously.

The current proposal would bind up further more capital in the fixed income instruments, which is contrarian to the positioning of the EC with regard to the Capital Markets Union (CMU) where they would want to foster stronger allocations to Equity markets from the Insurance Industry.

Therefore, it remains to be seen if the considered changes will be adopted as proposed by EIOPA.

We have looked at the effects on asset-liability management from the changes and show the impact on own funds and strategic asset allocation. Please reach out for more information to your DWS Sales representative or to the authors of this paper.

Disclaimer

DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they operate their business activities. The respective legal entities offering products or services under the DWS brand are specified in the respective contracts, sales materials and other product information documents. DWS, through DWS Group GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) are communicating this document in good faith and on the following basis.

This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by DWS Group, are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not constitute an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice.

The document was not produced, reviewed or edited by any research department within DWS and is not investment research. Therefore, laws and regulations relating to investment research do not apply to it. Any opinions expressed herein may differ from the opinions expressed by other legal entities of DWS or their departments including research departments.

The information contained in this document does not constitute a financial analysis but qualifies as marketing communication. This marketing communication is neither subject to all legal provisions ensuring the impartiality of financial analysis nor to any prohibition on trading prior to the publication of financial analyses. This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward looking statements expressed constitute the author‘s judgment as of the date of this document. Forward looking statements involve significant elements of subjective judgments and analyses and changes thereto and/ or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements or to any other financial information contained in this document. Past performance is not guarantee of future results.

We have gathered the information contained in this document from sources we believe to be reliable; but we do not guarantee the accuracy, completeness or fairness of such information. All third party data are copyrighted by and proprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notify the recipient in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

Investments are subject to various risks, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount origi-nally invested at any point in time. Furthermore, substantial fluctuations of the value of any investment are possible even over short periods of time. The terms of any investment will be exclusively subject to the detailed provisions, including risk consider-ations, contained in the offering documents. When making an investment decision, you should rely on the final documentation relating to any transaction.

No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. DWS or persons associated with it may (i) maintain a long or short position in securities referred to herein, or in related futures or options, and (ii) purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation.

DWS does not give taxation or legal advice. Prospective investors should seek advice from their own taxation agents and lawyers regarding the tax consequences on the purchase, ownership, disposal, redemption or transfer of the investments and strategies suggested by DWS. The relevant tax laws or regulations of the tax authorities may change at any time. DWS is not responsible for and has no obligation with respect to any tax implications on the investment suggested.

This document may not be reproduced or circulated without DWS written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States.

This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they operate their business activities. The respective legal entities offering products or services under the DWS brand are specified in the respective contracts, sales materials and other product information documents. DWS, through DWS Group GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) are communicating this document in good faith and on the following basis.

This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by DWS are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not constitute an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice.

The document was not produced, reviewed or edited by any research department within DWS and is not investment research. Therefore, laws and regulations relating to investment research do not apply to it. Any opinions expressed herein may differ from the opinions expressed by other legal entities of DWS or their departments including research departments.

The information contained in this document does not constitute a financial analysis but qualifies as marketing communication. This marketing communication is neither subject to all legal provisions ensuring the impartiality of financial analysis nor to any prohibition on trading prior to the publication of financial analyses.

This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward looking statements expressed constitute the author‘s judgment as of the date of this document. Forward looking statements involve significant elements of subjective judgments and analyses and changes thereto and/ or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements or to any other financial information contained in this document. Past performance is not guarantee of future results.

We have gathered the information contained in this document from sources we believe to be reliable; but we do not guarantee the accuracy, completeness or fairness of such information. All third party data are copyrighted by and proprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notify the recipient in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

Investments are subject to various risks, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of any investment are possible even over short periods of time. The terms of any investment will be exclusively subject to the detailed provisions, including risk considerations, contained in the offering documents. When making an investment decision, you should rely on the final documentation relating to any transaction.

No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. DWS or persons associated with it may (i) maintain a long or short position in securities referred to herein, or in related futures or options, and (ii) purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation.

DWS does not give taxation or legal advice. Prospective investors should seek advice from their own taxation agents and lawyers regarding the tax consequences on the purchase, ownership, disposal, redemption or transfer of the investments and strategies suggested by DWS. The relevant tax laws or regulations of the tax authorities may change at any time. DWS is not responsible for and has no obligation with respect to any tax implications on the investment suggested.

This document may not be reproduced or circulated without DWS written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States.

This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

Issued in German under DWS Investment GmbH and DWS International GmbH.

© 2020 DWS International GmbH /DWS Investment GmbH

Issued in the UK by DWS Investments UK Limited which is authorised and regulated by the Financial Conduct Authority (Reference number 429806).

© 2020 DWS Investments UK Limited

In Hong Kong, this document is issued by DWS Investments Hong Kong Limited and the content of this document has not been reviewed by the Securities and Futures Commission.

© 2020 DWS Investments Hong Kong Limited

In Singapore, this document is issued by DWS Investments Singapore Limited and the content of this document has not been reviewed by the Monetary Authority of Singapore.

© 2020 DWS Investments Singapore Limited

In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission.

© 2020 DWS Investments Australia Limited

For investors in Bermuda

This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

© 2021 DWS Group GmbH & Co. KGaA. All rights reserved. I-081650-1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in