DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

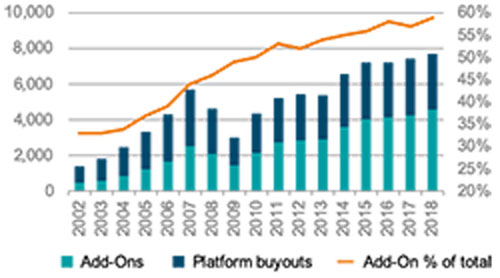

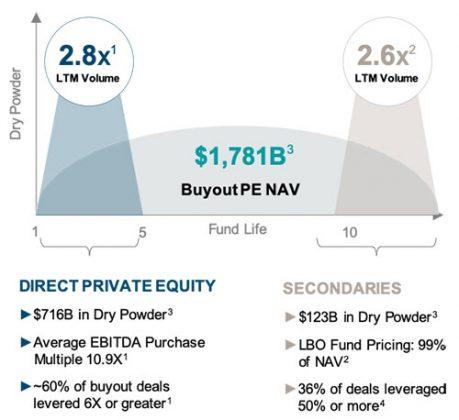

By any metric, it has been a great run in buyout PE over the past 20 years. Strong performance relative to public markets over this period has driven impressive industry growth with buyout NAV at $1.7T as of the end of 20181. The performance has attracted a wave of capital. Dry powder in the space in excess of $700B represents almost 3X the LTM deal volume2. Rising PE allocations have driven valuations up as more capital competes for deal flow. As a result, it has been a great “seller’s market” with consistently strong investment returns. But what happens when a sponsor is not a seller but a committed “buyer” of a portfolio investment they have been managing for a few years? An approach often utilized to further invest in performing assets is to scale platform companies with acquisitions. While this approach has been around since the early days of PE, it’s use has grown strongly in popularity. Add-ons have grown from representing about 35% of buyout transactions in the early 2000’s to almost 60% in 20181. See exhibit 1.

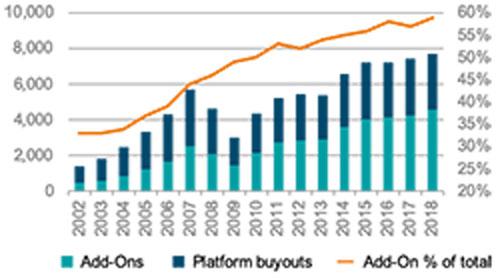

Further, 26% of add-ons in 2018 represented the 4th or later add-on acquisition for a platform company2. The appeal of the approach is clear. In the current environment of robust valuations, often the strategy can be a way to average down the entry valuation of the portfolio company by taking advantage of the markets tendency to assign larger companies higher multiples. See exhibit 2.

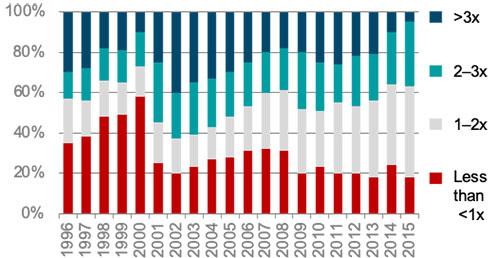

Seeking ways to capture more of the return potential from emerging performers remains a priority for sponsors. Examining buyout performance at the deal level helps explain why. Over the past 20 years, 29% of deals have been either written down or written off3. We believe this is a reflection of the inherent information asymmetry which characterizes the initial acquisition of a portfolio company – it is very difficult to fully capture the risk profile of a company until you have owned it for a few years. On the other hand, around 30% of deals have generated a return on invested capital of 2X or greater, and close to 20% have generated a 3X return to investors. See exhibit 3.

Another emerging trend is to extend the holding period for strong performing assets. One example of this trend is the increasing popularity of partial exits. In an environment characterized by robust valuations and strong competition for deals, GPs are reticent to sell a company they believe may have further upside potential. Partial exits allow the GP to take some of their chips off the table while booking a partial return and distribute capital to LP’s. Further, the sponsor is able to maintain their control stake in the asset and continue to execute on their value creation thesis.

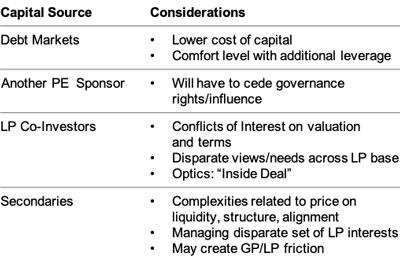

While there are a variety of capital sources available to sponsors to support these transactions, funding has primarily been sourced from platform company operating earnings and additional debt, supplemented by fund reserves set aside by the sponsor. Each of the traditional external capital sources has unique advantages but also certain disadvantages that may limit the attractiveness to the sponsor.

One of the obvious sources of follow-on capital to continue backing emerging performers early in the life of the fund would be the LPs in that fund. After all, they know the sponsor as well as the company.

Among the challenges associated with this option is the conflict in setting the valuation on a transaction between a sponsor and the LPs invested in the platform via the fund. Even a LP with a distinct co-investment and/or secondary

vehicle may struggle with the conflict of negotiating with an affiliated entity that has a LP position. In speaking with sponsors, these opportunities are often missed as a result of their discomfort with the embedded conflict and optics of what looks like an “inside deal”.

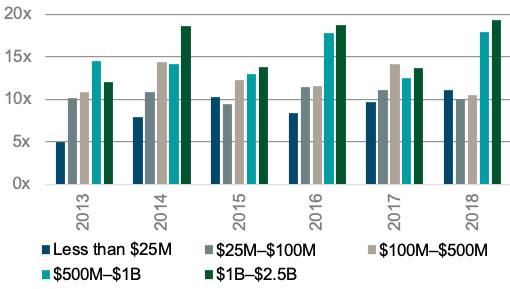

Another alternative may be to invite a competitor (another buyout sponsor) to invest in the asset. Sponsors are often hesitant to pursue that alternative due to the need to share governance rights and potential misalignment on exit timeframes. See exhibit 4.

We believe this may be one of the factors driving the growth of full exits represented by sales to other sponsors. In 2018, almost 1/3 of buyout exits were sponsor-to-sponsor sales – often a smaller sponsor selling a strong performer to a larger sponsor able to further invest in the asset. See exhibit 5.

A sponsor contemplating the full exit of an asset that they believe has further upside potential presents an attractive opportunity. Providing incremental non-control capital backing strongly performing assets to fund add-ons and/or partial liquidity can enable a sponsor to further invest in and extend their hold period in their emerging performers in order to capture more of the return potential of their best assets.

From the perspective of the capital provider, the strategy may have key risk mitigating elements:

• Reduced information asymmetry associated with investing in seasoned platforms backed by incumbent control sponsors

• A shorter path to exit as a result of investing in the asset “mid-hold”

• The ability to negotiate a transaction structure that bridges the potential misalignment of interests associated with coming into a strongly performing asset at a stepped up valuation and balances the interests of all parties – the sponsor, the fund LP’s, the platform as well as the capital provider.

In the current environment, the large silos of dry powder backing traditional primary buyout investments and end-of-life focused secondary strategies are driving robust valuations and strong competition for deal flow. In our view, focusing on opportunities between these silos to invest in performing mid-life portfolio companies is an attractive emerging opportunity in a less competitive space in the private market ecosystem. Effectively, this is a strategy that allows a manager to navigate into strongly performing private market companies with material further upside. Further, we expect to see opportunities of this character increase further still in a downturn as sponsors seek to support their best assets in a more capital constrained environment. See exhibit 6.

For control sponsors, the appeal of investing further in emerging performers is stronger than ever. A sponsor we visited with recently stated “we would prefer to continue to invest in our best assets than exit and reinvest capital in the current valuation environment.” Providing sponsors the capital to pursue that strategy is, in our view, a compelling opportunity which we expect to scale meaningfully, supported by the secular industry trends of increasing add-on activity and sponsor-to-sponsor exits.

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in