WRITTEN BY The Loomis Sayles Private Credit Team

The opportunity set in private fixed income is large and growing as the asset class evolves beyond its roots in the conventional private placement market into new sectors, geographies and structures.

On balance, private fixed income offers potential diversification benefits, attractive yields and stronger lender protections compared to public bonds, along with attendant liquidity and/or complexity risks. In this paper we examine the distinctive characteristics of this asset class and the additive role it can play in insurance company portfolios.

Why Insurance Companies Seek Private Fixed Income

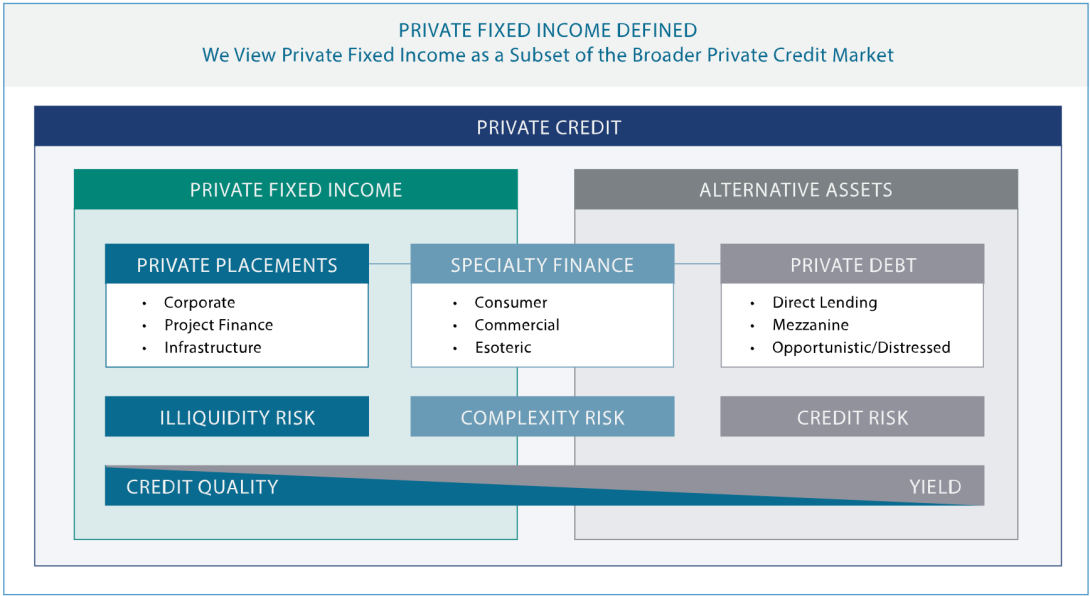

Over the past several decades, the search for yield and diversification has made private credit an increasingly important part of the portfolios for many insurance companies. As the market has evolved and expanded, private fixed income (PFI), a subset of private credit, has emerged as a particularly compelling asset class, in our view. PFI consists of predominantly fixed-rate, non-registered investment grade fixed income securities with tenors ranging from two to 30 years. The rise in demand for PFI from insurance companies and other institutional investors has coincided with the growth and maturation of the private credit markets overall. As private credit has expanded, specialty finance opportunities have been filling the gap between traditional private placements and private debt (i.e., direct lending). We believe this has created an opportunity set that goes beyond the traditional core of corporate, infrastructure and project finance debt into areas of specialty finance, which offer investors potentially higher yields and differentiated risk exposures across sectors, issuers, geographies and deal structures. Despite increased institutional allocations to PFI, misconceptions remain. These misconceptions may be preventing investors from taking advantage of the potential yield premia, structural protections and diversification benefits that we believe this asset class offers.

Views and opinions expressed reflect the current opinions of the authors only, and views are subject to change at any time without notice. Other industry analysts and investment personnel may have different views and opinions. Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal. Please see Key Investment Risks at the end of this paper for additional important disclosure.

Defining Characteristics of Private Fixed Income

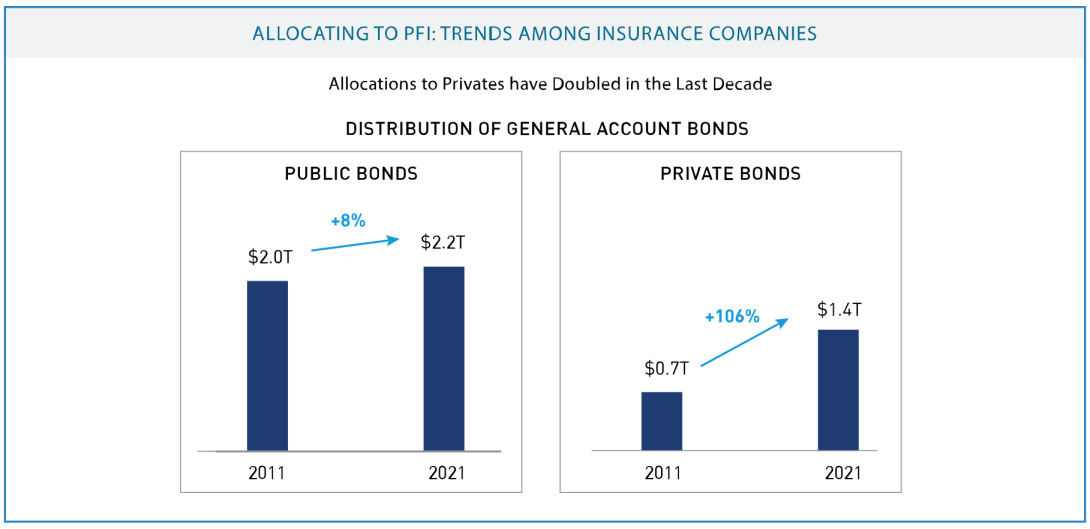

As a subset of private credit, PFI is a vast and diverse asset class with an estimated $1 trillion outstanding and more than $100 billion in estimated annual issuance.1 Its key distinguishing characteristics include:

- Predominantly fixed-rate bonds

- Not SEC-registered (private placements, loans and some 144A securities)

- Primarily investment-grade, although high-yield issuance has been growing due to increased demand and regulatory changes in the US insurance market

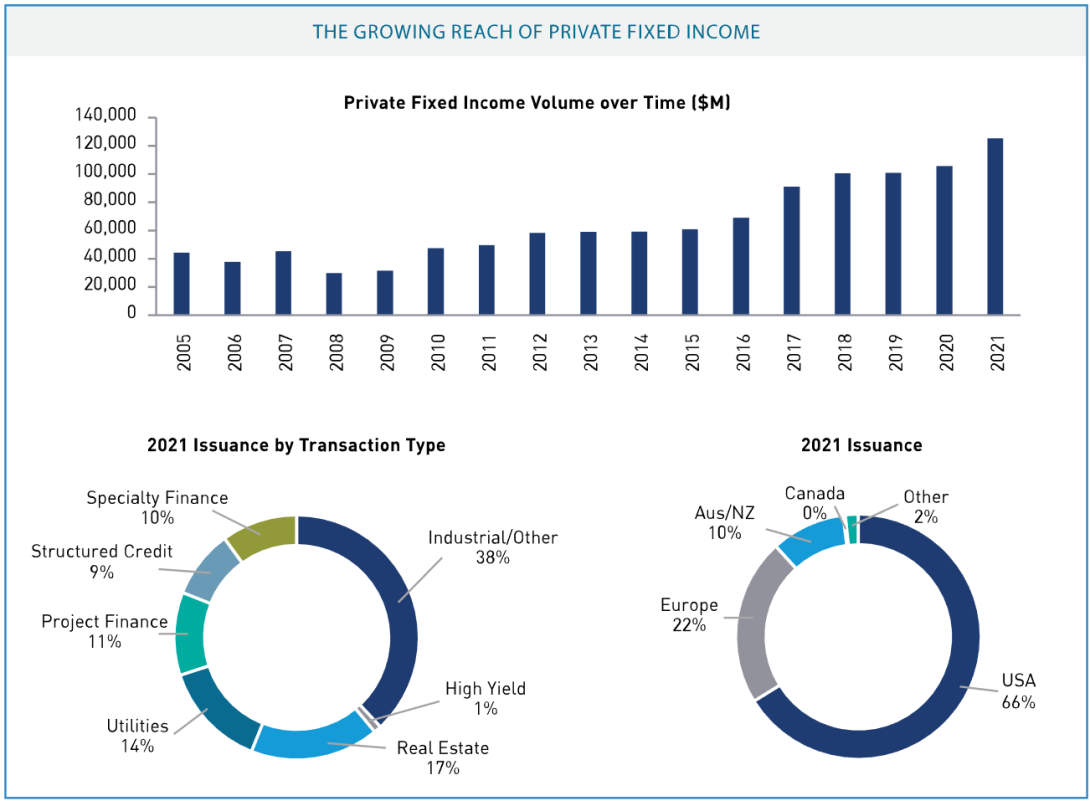

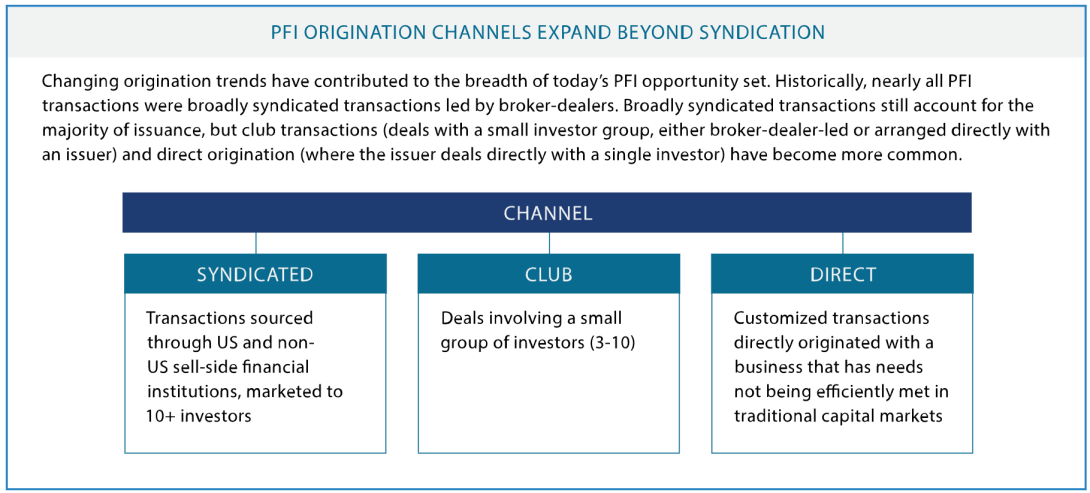

Sources: Private Placement Monitor, BofA Securities. Data as of 31 December 2021. This material is for informational purposes only and should not be construed as investment advice Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. Evolution of the Private Fixed Income Marketplace The evolution of PFI since the global financial crisis has been largely driven by the retreat of traditional commercial bank lenders, which, faced with increased regulation, have curtailed lending to certain market sectors. Non-traditional, private lenders filled the void, and the PFI opportunity set grew to include new sectors and new geographies beyond the US and Europe. Historically, the private placement space, consisted mostly of investment-grade corporate bonds; however, the past decade saw the emergence first of project finance and infrastructure opportunities and then private asset-backed transactions. In recent years, specialty finance transactions, which typically consist of secured, non-corporate consumer, commercial or esoteric lending, have come to the forefront, offering investors opportunities for additional yield potential and lower correlation versus more traditional private fixed income sectors. The growth and evolution of the PFI market continues to accelerate, driven by both supply and demand. On the demand side, insurers (historically, the main source of PFI funding) appear to have grown increasingly comfortable with the asset class and turned to it for enhanced yield and diversification potential. On the supply side, more (and increasingly diverse) issuers have sought private markets for reasons ranging from confidentiality to speed and certainty of execution, resulting in a growing variety of deal structures, covenants and collateral sources. We expect this trend will continue, particularly if non-insurance investors increase allocations to this asset class.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal. There is no guarantee that the investment objective will be realized or that the strategy will generate positive or excess returns. PFI's Value Proposition We believe PFI’s value proposition for investors rests on three pillars, each of which can be a possible source of excess portfolio return.

PFI’s Role in Insurance Company Portfolios

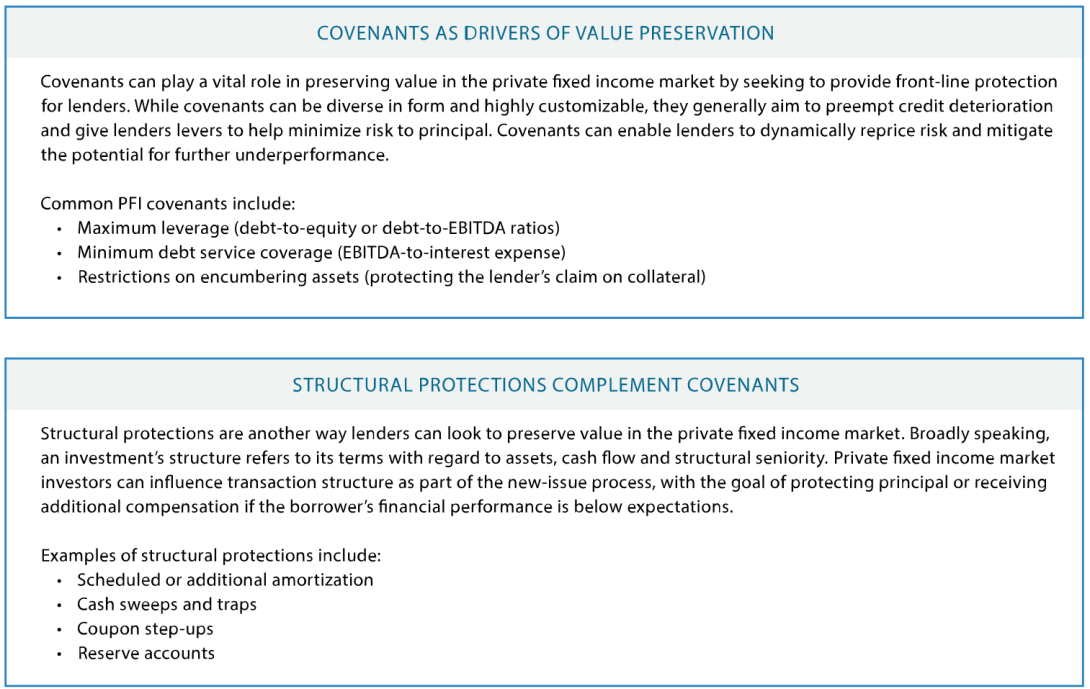

There are multiple reasons why PFI can play an important role in the portfolios of various types of insurance companies. First, the PFI universe consists of a range of fixed-rate obligations across a wide duration spectrum, providing the potential for insurers to match both long- and short-dated liabilities alike. Second, diversity in the issuer opportunity set and transaction structures can give insurers access to a broad and differentiated range of underlying risk factors for their investment portfolios beyond what is available in the public markets. Finally, covenants may be able to provide both additional lender protections in downside scenarios (higher recoveries vs. public bonds) and potential yield enhancement via fee income. Covenants also help mitigate against the downward migration of credit ratings, which can be beneficial for capital reserve requirement reasons. Considerations for Allocating to PFI When considering the role PFI can play in a portfolio, investors should focus on several factors. The following are our key views:

- Yield premia are dynamic. PFI’s yield advantage is comprised of an illiquidity premium and a complexity premium. The complexity premium is typically more constant, being a function of deal structure, while the illiquidity premium fluctuates as market conditions change. Hence, we think it is important to stay invested through the market cycle and avoid attempts at market- timing. Additionally, PFI can offer value through the cycle, not just when illiquidity premiums are high. In our view, it should not be seen as only a yield play. Covenants may be able to provide downside mitigation when it is needed most, and the asset class is a source of significant diversification potential. For these reasons, we believe PFI should be a staple allocation in an insurance company’s portfolio, not an opportunistic play.

- PFI’s liquidity profile may align well with insurers’ balance sheets. Insurers and other liability managers may underestimate the liquidity of the PFI market and overestimate the liquidity of the public bond market. PFI liquidity varies considerably by sector, origination type and other factors. Asset managers with PFI expertise can help investors appropriately size individual investments and make informed decisions about illiquidity risk. Liquidity needs for insurers can also be institutionally supported, if necessary. For example, the Federal Home Loan Bank system, which counts over 400 insurance companies as members, is a reliable and low-cost source of working capital for insurers.

- Focus on the risk exposures and potential return drivers PFI can add to the portfolio. PFI has distinct risk profiles from other alternative asset classes, and PFI and other private assets should not be grouped together into a single “private assets” bucket. One of the primary benefits of PFI is that it can bring a high level of idiosyncratic risk to the portfolio. PFI transactions need to be analyzed case-by-case and evaluated for their correlation with other assets in the portfolio and their impact on overall portfolio risk.

- Determining an appropriate PFI portfolio allocation should be a bottom-up exercise. Peer averages should not be the guiding principle in determining PFI allocations, in our view. This decision should be a function of the many factors that are specific to each insurer. Key variables include leverage, overall asset duration, loss trends on the liability side of the balance sheet and potential liquidity needs under various economic conditions. The evolving regulatory landscape is another factor, given capital reserve requirements. Insurers need to monitor regulators’ ongoing scrutiny of specific deal structures, capital formulae and sourcing of credit ratings. Based on this information, we believe insurers need to evaluate the potential portfolio impacts of regulatory change to determine their appropriate allocations to PFI.

Source: ACLI Life Insurers Fact Book 2022. Data available through 31 December 2021. This material is for informational purposes only and should not be construed as investment advice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

What to Look For in a PFI Manager

We believe managing PFI effectively requires resources and skills specific to the asset class.

- Strong relationships and a deep origination pipeline. The ability to source distinct opportunities is a differentiator in PFI. A wide network and credibility with both broker-dealers and issuers helps a manager get a first look at new transactions and a stronger position in the origination pipeline. Seeing a large volume of potential transactions can enable a manager to be highly selective, which we feel is essential to building a quality PFI portfolio.

- Independent research capabilities. PFI transactions are highly differentiated and issuer-specific, particularly in specialty finance sectors. Every deal carries idiosyncratic risk that may not be captured by the overall characteristics of the asset class. Furthermore, third-party credit ratings are important from a regulatory perspective but should not replace independent research. In our view, an effective manager will perform proprietary credit analysis and generate an independent view on credit risk and the appropriate covenant and structural protections. The manager should conduct fundamental research into the issuer and the industry and do a detailed analysis of the deal structure and risk exposures.

- Scale and infrastructure. Managing PFI is labor-intensive and multi-disciplinary; these investments take substantial resources and diverse expertise. The process begins with origination and underwriting. A manager should be prepared to manage every transaction through its life cycle. The manager will need to continually monitor portfolio risk exposures as market conditions change, track issuer financial performance over the deal’s life cycle and negotiate amendments if financial performance falls below expectations.

- Cross-functional expertise. Vetting and managing PFI effectively is a collaborative effort that requires a wide range of skills. Performing due diligence on incoming transactions and managing a PFI portfolio involves sector specialists, fundamental credit analysts, transaction attorneys, risk analysts, operational managers and portfolio managers with specific expertise in the asset class.

- Technological resources. Technology plays a central role because of the complexity of many PFI transactions and the high level of idiosyncratic risk they present. Technology allows a manager to thoroughly evaluate and prioritize deal flow, as well as monitor and track risk across highly differentiated portfolios throughout the transaction life cycle.

Putting PFI Best Practices to Work

The expansion of PFI into new deal structures, sectors and geographies presents a growing potential opportunity set for insurers and other institutional investors. By analyzing the trends driving the growth of the PFI market and by partnering with managers committed to the best practices of effective PFI management, investors can seek to harness the potential yield and diversification benefits of this growing asset class. PRIVATE FIXED INCOME AT LOOMIS SAYLES Loomis Sayles’ dedicated Private Credit Group is an investment team with an average industry tenure of more than 20 years. The team is backed by Loomis Sayles’ recognized expertise in fundamental research and its global reputation as a highly respected fixed income manager. Founded in 1926, Loomis Sayles provides research coverage across all major market sectors, industries and geographies. The Private Credit Group leverages these resources to explore the large and diverse opportunity set available in private fixed income, including corporate credit, infrastructure debt, project finance and specialty finance. In sourcing and managing PFI deals, the Private Credit Group taps a deep pool of cross-functional expertise within Loomis Sayles. This includes expertise in credit research, mortgage and structured finance, legal and compliance, actuarial science, distressed debt, restructuring, ESG, quantitative research, risk analysis, fundamental research, macro strategy, technology and operations. To learn more about our PFI capabilities, please contact Colin Dowdall or Gregory Ward.

Download PDF

Authors

Chris Gudmastad, CFA

Head of Private Credit

Colin Dowdall, CFA

Director of Insurance Solutions

Gregory Ward

Investment Director, Private Credit

Michael Meyer, CFA

Portfolio Manager and Managing Director, Private Credit

Endnotes 1 Source: Private Placement Monitor, as of 31 December 2021. Important Disclosure This paper is provided for informational purposes only and should not be construed as investment advice. Opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Other industry analysts and investment personnel may have different views and opinions. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted, and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice. Diversification does not ensure a profit or guarantee against a loss. Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal. Market conditions are extremely fluid and change frequently. Past performance is no guarantee of, and not necessarily indicative of, future results. LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office. Key Investment Risks Credit Risk The risk that the issuer or borrower will fail to make timely payments of interest and/or principal. This risk is heightened for lower rated or higher yielding fixed income securities and lower rated borrowers. Issuer Risk The risk that the value of securities may decline due to a number of reasons relating to the issuer or the borrower or their industries or sectors. This risk is heightened for lower rated fixed income securities or borrowers. Liquidity Risk The risk that the strategy may be unable to find a buyer for its investments when it seeks to sell them, which is heightened for high yield, mortgage-backed and asset-backed securities. Interest Rate Risk The risk that the value of a debt obligation falls as interest rates rise. Non-US Securities Risk The risk that the value of non-U.S. investments will fall as a result of political, social, economic or currency factors or other issues relating to non-U.S. investing generally. Among other things, nationalization, expropriation or confiscatory taxation, currency blockage, political changes or diplomatic developments can negatively impact the value of investments. Non-U.S. securities markets may be relatively small or underdeveloped, and non-U.S. companies may not be subject to the same degree of regulation or reporting requirements as comparable U.S. companies. This risk is heightened for underdeveloped or emerging markets, which may be more likely to experience political or economic stability than larger, more established countries. Settlement issues may occur. Currency Risk The risk that the value of investments will fall as a result of changes in exchange rates, particularly for global portfolios. Derivatives Risk (for portfolios that utilize derivatives) The risk that the value of the Strategy’s derivatives instruments will fall because of changes in the value of the underlying reference instrument, pricing difficulties or lack of correlation with the underlying investment. Leverage Risk (for portfolios that utilize leverage) The risk of increased loss in value or volatility due to the use of leverage, or obtaining investment exposure greater than the value of an account. Counterparty Risk The risk that the counterparty to a swap or other derivatives contract will default on its obligations. Prepayment Risk The risk that debt securities, particularly mortgage-related securities, may be prepaid, resulting in reinvestment of proceeds in securities with lower yields. An investment may also incur a loss when there is a prepayment of securities purchased at a premium. Prepayments are likely to be greater during periods of declining interest rates. Extension Risk The risk that an unexpected rise in interest rates will extend the life of a mortgage or asset-backed security beyond the expected prepayment time, typically reducing the security’s value. Equity Risk The risk that the value of stock may decline for issuer-related or other reasons. Non-Diversified Strategies Non-diversified strategies tend to be more volatile than diversified strategies and the market as a whole. Municipal Securities Risk The risk that municipal markets may be volatile and can be significantly affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal securities. Models and Data Risk The strategy may utilize quantitative model based strategies. This is the risk that one or all of the quantitative or systematic models used may fail to identify profitable opportunities at any time. These models may incorrectly identify opportunities and these misidentified opportunities may lead to substantial losses. Models may be predictive in nature and may result in an incorrect assessment of future events. Data used in the construction of models may prove to be inaccurate or stale, which may result in investment losses. General Risk Any investment that has the possibility for profits also has the possibility of losses, including loss of principal. MALR030469