The earth’s climate is always changing. In the last 650,000 years, there have been seven ice ages. When the last one ended about 11,700 years ago, the modern climate era began. It only took a temperature increase of 4–7°C to melt the ice sheets and create the conditions that would allow human civilization to flourish.

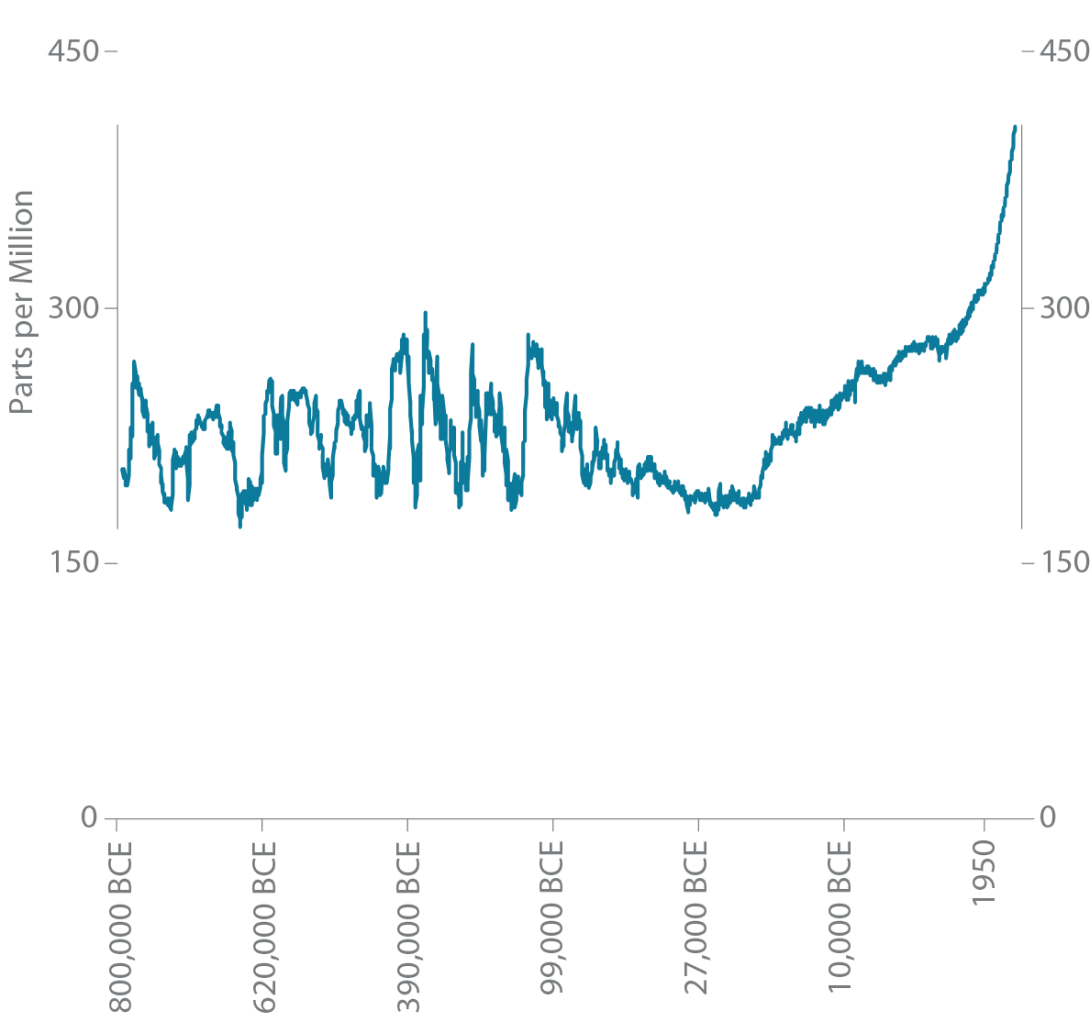

Climate scientists attribute these historical cycles to minute variations in the earth’s orbit, which change the amount of solar energy received. At the same time, the amount of CO2 in the atmosphere has never been greater (Figure 1), suggesting a strong correlation with rising temperatures and the extreme weather events that have become the norm. Bushfires rage with greater frequency. Hurricanes grow fiercer. At the rate glaciers are melting, the Arctic will be free of summer ice by 2050. By 2100, 1-in-20-year extreme heat days are projected to occur every other year.

Entire ecosystems are collapsing, accelerating the feedback loops that follow. As the ice caps melt, sea levels rise, methane— a greenhouse gas 20 times more powerful than CO2—is released, and the albedo effect, which describes the ability of the earth to reflect solar radiation, diminishes. Animals cannot adapt fast enough, and local communities are being forced to move. “Climate refugee” has entered the vernacular.

FIGURE 1 | GLOBAL CO2 CONCENTRATIONS

Source: National Oceanic & Atmospheric Administration, 2018.

Causal Debate

Despite mounting evidence, it was not until the late 1980s that the greenhouse effect and humanity’s role in causing it became broadly recognized. It started with the Montreal Protocol, which recognized industrial activity’s role in depleting the ozone layer. Yet after more than three decades, the complexity of climate-related data, coupled with entrenched political and economic interests, has protracted the debate on the causes of climate change. Rather than dig their heels in, several organizations are sidestepping the debate, taking actions to promote a decarbonized economy. A common thrust of these initiatives is improving the flow of information and disclosure on climate-related risks. Though a far cry from the much-needed globally coordinated regulatory response, these are critical precursors to a comprehensive market response.» Each report written by the Intergovernmental Panel on Climate Change (IPCC) hopes to compel governments and consumers to change their habits enough to keep the earth’s temperature from rising. Critically, its 2018 report emphasized the need to keep temperature rise below 1.5°C versus the previously recommended 2°C.1

» The United Nation’s Principles for Responsible Investment score their 2,300-plus signatories on how effectively they are implementing six principles designed to align the investment community behind a set of common objectives. It recently released a five-step framework for incorporating nonfinancial objectives (including climate considerations) into investment programs.2

» The UN’s Sustainable Development Goals (SDGs) positions climate change as the single biggest threat to development and the linchpin to attaining the remaining SDGs.

» The Task Force on Climate-related Financial Disclosures (TCFD) is pushing for greater transparency, highlighting the critical governance role of boards in providing strategic leadership on climate change.

» The EU Taxonomy promises to be one of the most comprehensive frameworks for defining sustainable investing and allocating capital toward decarbonization.

» Canada is developing its own taxonomy that is more suitable for resource-heavy economies.

That society has allowed atmospheric CO2 levels to rise so far represents a failure on the part of markets and regulators. As with any other pollutant, StepStone views the exponential rise in CO2 as a negative externality. And like any other externality, it can only be eliminated by pricing in its effect. To do so, the market needs the data that comprehensive disclosure and pricing frameworks can bring about. Better information will come, albeit slowly. Even then, markets will take time to unwind the externalities, reallocate costs, and reprice assets. In all likelihood, it will take decades to decarbonize the global economy. This is the investment opportunity, and it is huge.

Read section: The EU Taxonomy here

Regulatory Emissions Pricing

Several regulatory initiatives have been championed regionally, but climate change is a global challenge that can only be solved through a coordinated effort. Not all countries, however, are aligned. Historically, wealthy nations have enjoyed growth on the back of fossil fuels while not directly paying for the emissions externality or subsidizing poor nations that are now bearing the brunt of climate change. To date, 21 countries and several US states have a form of carbon pricing mechanism with variable levels of emission coverage.3 China, the largest emitter of CO2, is developing an emissions trading scheme (ETS) in concert with power sector reform. It is conceivable the Chinese will introduce an emissions cap within the next five years. That leaves the US. Almost a decade since its plans to instate a social cost of carbon faltered, the second-largest emitter still lacks a clear path to carbon pricing. It is no wonder an international regulatory regime remains a pipe dream. Hopefully where regulators fail, the markets will succeed.

Setting a price on carbon will also be instrumental in addressing the social inequities effected by climate change. Funding for education and housing solutions may well need to be linked to carbon pricing and decarbonization policies. Climate change is more than an environmental issue; any efforts to resolve it sustainably must embrace social considerations.4 To be truly sustainable, these efforts must be just.

Decarbonization Has To Be Just

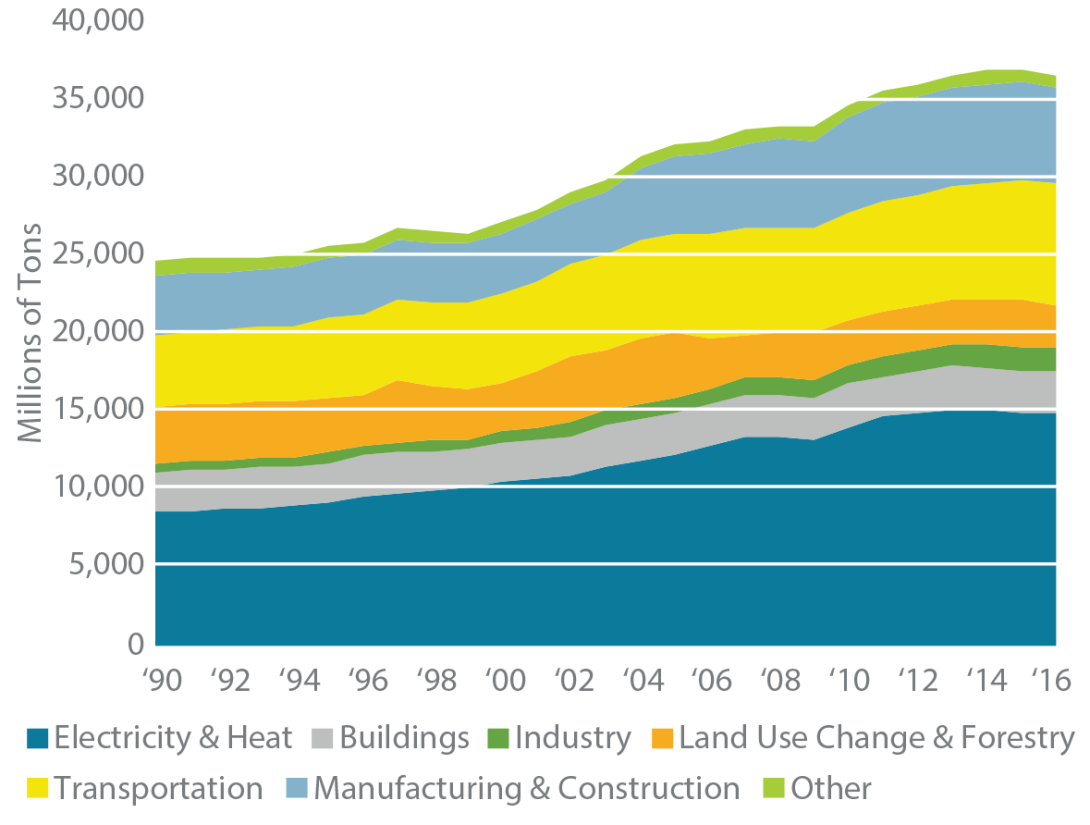

The rise in global temperatures is highly correlated to greater levels of atmospheric CO2. As a result, most efforts to fight climate change have focused on curbing additional emissions. Charts like the one in Figure 2 have played a major role in supporting the rise of renewable energy and alternative fuels in LP portfolios. They also explain why so many of the policy responses put forth by the world’s governments, including the EU, make these sectors a priority.

Politicians the world over, especially in Europe, are pushing decarbonization as a growth strategy capable of spawning new industries and generating new employment opportunities. Concurrently, our collective awareness of the consequences of structural shifts in the economy is growing.

FIGURE 2 | CO2 EMISSIONS BY SECTOR

Source: World Bank, 2016.

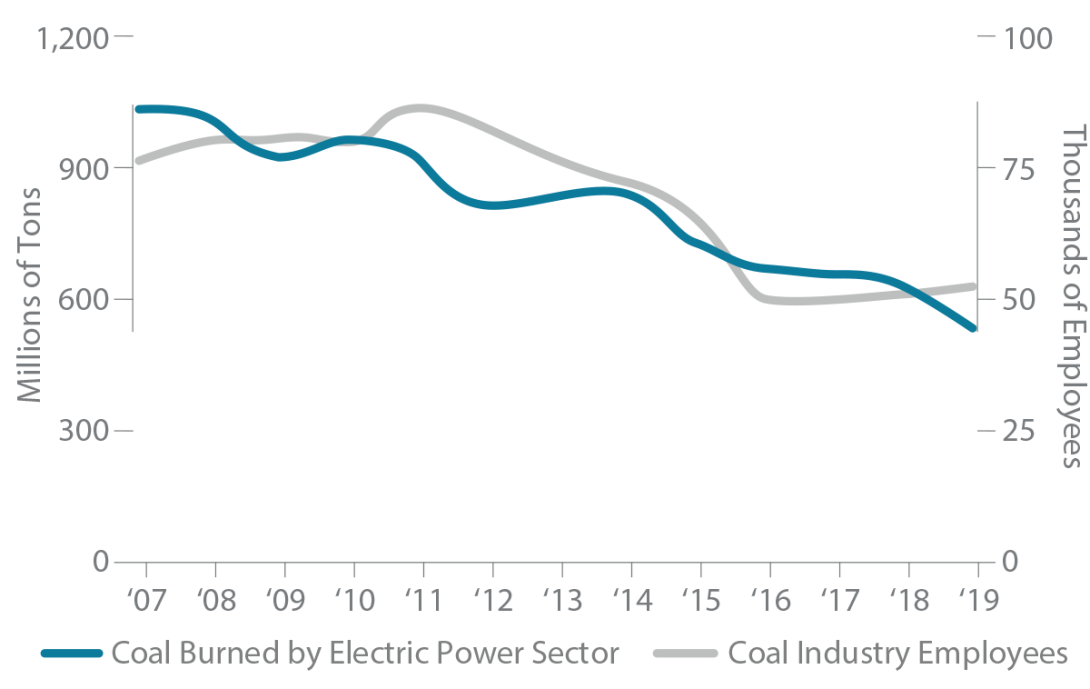

Take the shale-gas revolution that has redefined the American energy landscape, for example. Both coal and natural gas are fossil fuels, but a gas-fired power plant can emit half as much CO2.5 This at least partly explains why US CO2 emissions have fallen by 12% since 2007.6 Better air quality and improved health outcomes make this a success story. But as the amount of coal burned by American power plants fell by half, the number of people employed in coal mines is just 60% of what it was in 2007 (Figure 3).7 For the communities that relied heavily upon coal to fuel their economies, the results have been catastrophic. It is hard to argue in favor of the long-term environmental benefits before the communities still reeling today.

FIGURE 3 | COAL INDUSTRY DYNAMICS

Source: US Energy Information Administration; Federal Reserve Bank of St. Louis, May 2020.

With enough foresight, this inequitable outcome might have been avoided, the story flipped to one in which marginalized workers received greater access to opportunities to acquire new skills and affordable housing. Markets might well step in without any government intervention, but the path for doing so is still made easier if governments pave one.

This well-trodden example highlights what we aim to outline in this paper: There are enormous opportunities to support decarbonization. For this effort to be sustainable, investors need to support solutions that ensure no one is left behind. Social-equity considerations must go hand in hand with climate-change efforts.

The Emissions Externality

As discussed in our 2019 white paper “Responsible Investing: Internalizing the Externality,” climate change, like many other ESG considerations, is an externality. The lack of clear information and pricing signals allows the externality to persist, resulting in suboptimal resource allocation. A Goldman Sachs report indicates a great disparity between carbon pricing under existing ETS and the market’s imputed carbon price via voluntary schemes.8 An effective international carbon pricing scheme is sorely lacking, and until governments align to create one, a huge arbitrage opportunity will exist.

Over time externalities affect cap rates, valuation multiples, revenues, and costs. Integrating externalities into an underwriting process is easier said than done—especially with imperfect information on issues like emissions that manifest over decades. But the payoff—both in enhanced return and reduced risk—to those who are able to may be significant. As such, pricing in externalities should fall squarely in line with

fiduciary duties.

As the TCFD, the Non-Financial Reporting Directive (NFRD), the EU Taxonomy, and other efforts encourage climate-related information flows, and companies disclose the climate-related risks and opportunities in their operations, these externalities will become easier to price. Still, the issues are complex and this favors those with specialized expertise.

Asset managers will face a range of new categories of stranded assets. Thinking about the appetite of the next buyer to bear these climate risks is going to bring this dilemma into sharper focus. Take, for instance, midstream energy assets that could one day form the backbone of clean-energy hydrogen infrastructure. Should an investor purchase these assets today even though, for example, the EU Taxonomy does not recognize them as sustainable?

The investment opportunity exists in having the foresight to price in these issues before the broader market does. StepStone believes the investors who can isolate these risk factors, manage them, and build them into asset valuations will capitalize on the price dislocation created by those either too slow or unwilling to account for these factors.

Market-related risks are but one set of complicating factors. Regulatory uncertainty is another. To help the investment community navigate these risks, the UN (and others) sponsored the Inevitable Policy Response to consider the financial effects of yet unpromulgated regulations. An incongruous patchwork of regulatory regimes will only exacerbate the risks faced by businesses and investors as they navigate decarbonization. Private market investors, who are not hostage to daily price movements, should be well positioned to root out opportunities in such an environment. The long holding periods and active ownership structure that characterize private markets are well suited for climate adaptation and mitigation strategies alike. Around the world, investors are concluding that private markets are an excellent conduit for fulfilling a climate-change mandate.

Climate change will manifest in every aspect of our lives and every sector of the economy. Everything is at stake: where we live, what we eat, and how we communicate. On the surface, the breadth and magnitude of the impact may seem daunting, but for any investor intent upon building a climateresilient investment program, there are likely to be scores of opportunities across the risk-return spectrum. And private markets may well provide an ideal venue for capitalizing on them.

Information will never be perfect, the efforts of the TCFD and others notwithstanding. However, making sense of imperfect information has become second nature to private market investors whose experience vetting companies of various sizes, with varying degrees of operational sophistication, are suited to this challenge. As active shareholders, private investors are attuned to driving change within companies. Advocacy, engagement, and operational value-add are nothing new in private markets. But the opportunity to focus this expertise on a problem like climate change is without precedent.

Defining A Climate-Change Mandate

The breadth of the climate-change agenda is daunting. By seeking to restructure the global economy, opportunities are being created in almost every sector and industry. Having too many choices, however, is just as challenging as having too few. For example, should investors provide the capital necessary for a cement producer to reduce emissions or fund an engineering firm focused on sustainable design? Both could result in a substantial reduction in carbon emissions, and though it is difficult to calculate a priori which would result in the greatest lifetime reduction in carbon emissions, often there will be a bias toward “greener” companies. Generally the cement company loses out. Thus our concern is that too narrow an interpretation of a climate-change mandate ignores a wealth of opportunities.

Investment opportunities often aim to solve a specific problem. Take education software, for example. Most investors and entrepreneurs would regard this as a pure play on education that capitalizes on changing work habits. We would argue it could just as easily address communities negatively affected by the clean energy shift, and that it has a critical role to play in sustainable decarbonization. Part of the onus rests on the entrepreneurs to broaden the technology’s application. Fund managers and limited partners can help them do so. In the process, developers may identify an even more valuable market opportunity.

Similarly, seed manufacturers tend to home in on disease resistance. But reducing demand for fertilizers and pesticides can bring about a material emissions reduction. In our estimation, this agribusiness play will satisfy a climate-change mandate.

Often there is the need to look at second-order effects. Take, for example, certain carbon-intensive sectors that produce components that companies in other sectors rely upon to reduce their own carbon footprints. To generate electricity more efficiently, power companies need someone to design and forge better turbines. All too often climate-change mandates are inclined to favor innovation over heavy industrials.

Each of these examples requires investors to embrace the breadth of opportunities that a climate-change investment program implies. StepStone suggests that a climate-change mandate be defined as follows:

Exposure to investments that contribute to the sustainable reduction of greenhouse gas emissions.

This definition encompasses companies that curb their emissions, help others reduce theirs, or address the social challenges that a warming planet effects. Again, to be successful, decarbonization must be just.

Many large LPs have paid much attention to renewable energy. The decline in cap rates reflects how this industry has matured, moving through private equity into infrastructure over the last decade. Development and technology risks have been displaced by execution risks, which are the bread and butter of infrastructure operators. Renewables are an important component of the climate-change universe, but they do not define it. Large-scale investors are fortunate in that the four capital-intensive sectors that define the current economy will form the backbone of a decarbonized economy: food, energy, transportation, and communications (which includes data, sensors, and satellites).

As the cost of communication approaches zero, the lifestyle changes have been material. Just imagine trying to navigate Covid-19 without inexpensive telework, data storage, and on-demand home entertainment. Though it’s impossible to predict the exact outcomes, the benefits will be similar once energy and transportation costs begin to fall asymptotically. A climate-change agenda will drive this.

A Climate-Change Framework

We have developed a framework that our clients may find helpful as they ponder whether or how to structure their climate-change investment program. There are five considerations (Figure 4).

FIGURE 4 | CLIMATE-CHANGE INVESTMENT FRAMEWORK

For illustrative purposes only.

The process starts with the funnel of investment opportunities held at its widest. As each consideration is applied, the opportunity set thins out.

For example, setting a hurdle at net IRR of 17% leads the client toward private equity and greenfield infrastructure and real estate; a hurdle of 11% opens the door to private debt. Another decision with far-reaching consequences is how to fund the allocation. If a climate-change allocation is part of the investor’s strategic asset allocation, a multi–asset class solution tends to arise; a program devised at the asset-class level will be narrower.

This consideration is interlinked with how an institution defines its climate-change agenda and the nonfinancial outcomes it wishes to achieve. Is the institution focused on addressing social equity broadly or affordable housing specifically? Another governance consideration with acute consequences given the stage of development of the market, is that there are several first-time GPs with vehicles dedicated to climate change. Often, these funds are small, seeking less than U$100 million in commitments. For many LPs, the need to deploy capital at scale or an aversion to emerging managers will limit the opportunity set. Finally, we believe it is important to review legacy exposure: Most LPs have the makings of a climate-change investment program in their existing portfolios. Being aware of existing exposures allows investors to choose whether the new program should be independent or complementary.

Many investors are seeking to fulfill an agenda that meets both financial and nonfinancial objectives, which may or may not be linked to SDGs. As a consequence, it is becoming increasingly important for asset owners to establish a reporting protocol that measures how investments are contributing to the attainment of these nonfinancial objectives. Stakeholders can accept shortcomings, provided the investment community is honest, its commitment is genuine, and it makes progress.

While case studies are helpful, the need is increasing for GPs to provide data on nonfinancial considerations. Measuring the carbon footprint of their holdings, setting emission targets, and reporting on measurable change are the path forward. These are costly endeavors that require the expertise of specialist consultants. Notwithstanding, they will become compulsory. GPs will need to invest in suitable information systems to efficiently store and report on this information.

The next chapter in private markets is as exciting as it is complex. Working together, GPs and LPs are in a position to make real progress toward addressing climate change.

Conclusion

Stewards of private capital have the opportunity to preempt government action to provide critical leadership on climate change. Not only is private capital accustomed to the long-term mindset decarbonization requires, but the sector is accustomed to vetting and pricing assets, even in the face

of imperfect information. Similarly, private market investors are experts at engaging with corporate officers to advocate change at both the strategic and operational levels. These skills are well suited to perceiving best value in positioning businesses for a decarbonized world. LPs in particular have an important role in promoting better disclosure and reporting from GPs. This pressure will ripple through the entire chain driving improved data collection and transparency at the company level, which is critical for being able to target and deliver reduced emissions.

The cost to future generations of not mobilizing capital around climate change is too high to fathom. The investment community is perfectly positioned to benefit from one of the biggest investment opportunities in generations: decarbonizing the global economy. Enabled by smart, inexpensive communication systems, society can completely redesign our food, energy, and transportation systems. No sector will remain untouched. On our march to civilization, technology has been used to cocoon humankind from the elements. But with the information revolution—eyes in the sky and sensors in the soil, sea, and air—society cannot ignore what the data are saying: The earth is getting warmer. Society needs to solve it.

1 IPCC. 2018. “Special Report: Global Warming of 1.5° C.”

2 StepStone Group is a signatory to both the TCFD and the UN PRI.

3 International Carbon Action Partnership. 2020. “Special Report: Emissions Trading Worldwide.”

4 A belief we share, by the way.

5 A fact not lost on the EU. Its new taxonomy favorably regards efficient gas-fired plants.

6 US Environmental Protection Agency. 2019. Inventory of US Greenhouse Gas Emissions and Sinks 1990–2017.

7 To be fair, automation also played a role in job losses, and many of those who lost their jobs in coal found opportunities in shale gas.

8 Goldman Sachs. 2020. "Carbonomics: The Green Engine of Economic Recovery."

Read the full article here

This document is for information purposes only and has been compiled with publicly available information. StepStone makes no guarantees of the accuracy of the information provided. This information is for the use of StepStone’s clients and contacts only. This report is only provided for informational purposes. This report may include information that is based, in part or in full, on assumptions, models and/or other analysis (not all of which may be described herein). StepStone makes no representation or warranty as to the reasonableness of such assumptions, models or analysis or the conclusions drawn. Any opinions expressed herein are current opinions as of the date hereof and are subject to change at any time. StepStone is not intending to provide investment, tax or other advice to you or any other party, and no information in this document is to be relied upon for the purpose of making or communicating investments or other decisions. Neither the information nor any opinion expressed in this report constitutes a solicitation, an offer or a recommendation to buy, sell or dispose of any investment, to engage in any other transaction or to provide any investment advice or service.

Past performance is not a guarantee of future results. Actual results may vary.

Each of StepStone Group LP, StepStone Group Real Assets LP and StepStone Group Real Estate LP is an investment adviser registered with the Securities and Exchange Commission (“SEC”). StepStone Group Europe LLP is authorized and regulated by the Financial Conduct Authority, firm reference number 551580. Swiss Capital Invest Holding (Dublin) Ltd (“SCHIDL”) is an SEC Registered Investment Advisor and Swiss Capital Alternative Investments AG (“SCAI”) (together with SCHIDL, “SwissCap”) is registered as a Relying Advisor with the SEC. Such registrations do not imply a certain level of skill or training and no inference to the contrary should be made.

Manager references herein are for illustrative purposes only and do not constitute investment recommendations.