Elizabeth Bakarich, CFA | Portfolio Manager—Emerging Market Corporate Debt

Download PDF

What You Need to Know

Once a backwater of the bond world, emerging-market (EM) corporate debt has grown into a full-fledged asset class that investors can tap to diversify their EM allocation and boost their return potential.

$2.3T

EM corporate debt outstanding as of June 30, 2019

>600

Number of corporate bond issuers included in the J.P. Morgan CEMBI Index

16.7%

The difference in 2015 annual returns for hard-currency EM corporates and local-currency EM sovereigns.

For years, when institutional investors talked about the composition of their EM bond portfolios, they were talking about currency. Some bonds would be denominated in US dollars or another “hard” currency, others in the local currency of the issuing country—Mexican pesos, Turkish lire, Chinese renminbi. But nearly all of them were government-issued sovereign bonds.

EM corporate bonds have historically been relegated to the periphery of fixed-income portfolios—if they’re represented at all. There was US$113 billion benchmarked to J.P. Morgan’s EM corporate indices as of June 30, about one-sixth of the amount tied to its hard- and local-currency sovereign indices.

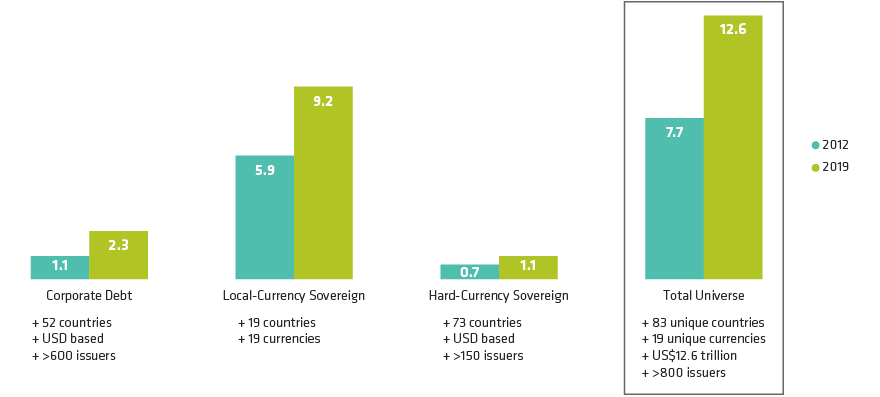

This underallocation may have been understandable a decade ago, when the outstanding debt stock was lower and less diversified. It isn’t anymore. The total EM corporate debt stock doubled between 2012 and 2018 to US$2.3 trillion, which is about twice the amount of outstanding hard-currency EM sovereign debt. And the standard EM corporate benchmark, the J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI), encompasses bonds from more than 600 corporate issuers in 52 different countries (Display).

A Bigger Pond to Fish In: EM Debt’s Growing Opportunity Set

Total Debt Stock (USD Trillions)

As of June 30, 2019

For informational purposes only. There can be no assurance that any investment objectives will be achieved.

Corporate Debt: J.P. Morgan CEMBI Broad Diversified; Local-Currency Sovereign: J.P. Morgan GBI-EM Global Diversified; Hard-Currency Sovereign: J.P. Morgan EMBI

Global Diversified

Source: J.P. Morgan Markets and AllianceBernstein (AB)

Widening the Opportunity Set

An allocation to corporate debt provides diversification through exposure to more countries and to different parts of the credit cycle. It also gives investors access to a wider range of issuers in different sectors, often with a spread pickup over EM sovereign debt.

Corporate debt provides diversification through exposure to more countries and to different parts of the credit cycle.

How investors add EM corporates to an existing fixed-income allocation will depend to some extent on their individual needs and comfort level.

EM corporate bonds aren’t entirely without risk, of course. While corporate governance, transparency and protections for creditors and shareholders have improved over the last decade, they still lag standards in developed economies. This is why it’s so important to choose the right manager for your EMD allocation.

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.