DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

U.S. real estate performed remarkably well in 2021. Although the year began tepidly amid a surge of COVID infections, the steady rollout of vaccines unleashed a resurgence of economic, leasing, and transactions activity in the spring and summer. By the third quarter, overall vacancy rates had dropped to nearly their lowest levels in more than 30 years.1 Net Operating Income (NOI) increased 9% year-over-year, a rate eclipsed only once (during the dot-com boom) since 1983.2 Transaction volume of $462 billion in the first three quarters of 2021 was the highest in at least 20 years.3 Finally, the fund-level ODCE real estate index delivered its strongest total returns in history (since 1978).4

A flood of capital, reflected in compressing cap rates, played a role in pushing values higher. Yet the rebound was largely driven by fundamentals. The apartment sector absorbed 251,000 units in the third quarter — more than the annual average over the past decade (208,000).5 Absorption of nearly half a million units in the first three quarters shattered annual totals back to 1996.6 Industrial absorption of 432 million SF was the highest since at least 1989.7 Even the retail sector, which suffered well-documented pressure from e-commerce as well as mandated store closures, registered its fifth consecutive quarter of positive net demand.8 In all three sectors, vacancy rates dropped to their lowest levels in history, underpinning solid year-over-year rent growth (about 10% in the case of apartments and industrial buildings; 2% for retail centers).9

Amid last year’s upswing, the office sector stood out as a notable exception. To be sure, valuations held steady, and the market displayed scant signs of distress (office CMBS delinquencies of 2.4% in October were below pre-pandemic levels and a fraction of their 10%+ Global Financial Crisis (GFC) peaks).10 Regardless of whether they were using their space (national office usage remained mired at 40% in December), tenants generally continued to meet their lease obligations, keeping NOIs stable.11 Yet a second year of negative absorption reduced office demand by a cumulative total of 100 million SF, more than twice as much as in 2009 (40 million SF), driving vacancies to dot-com and GFC era highs.12

We believe that U.S. real estate is poised to sustain its strong momentum, courtesy of an unusually favorable set of macroeconomic and financial conditions. Fueled by extraordinary fiscal stimulus (approximately $5.5 trillion, equivalent to 25% of GDP), we estimate that the economy expanded by about 5.5% in 2021.13 In our view, we are unlikely to see similar levels of fiscal support in 2022. Nevertheless, we believe that a strong labor market and elevated asset prices ((home prices and the stock market are up 25% and 35%, respectively, since before the pandemic) will motivate consumers to release at least some of the $2.5 trillion (12% of GDP) in surplus savings that they accumulated during the pandemic.14 GDP growth may slow toward 4%, but this would still rest well above trend levels (about 2%) and cap the fastest two-year expansion since the early-1980s.15 Consistent with last year, we expect that strong economic growth (characterized by healthy job, wage, and business revenue gains) will fuel robust leasing activity across most types of residential and commercial property.

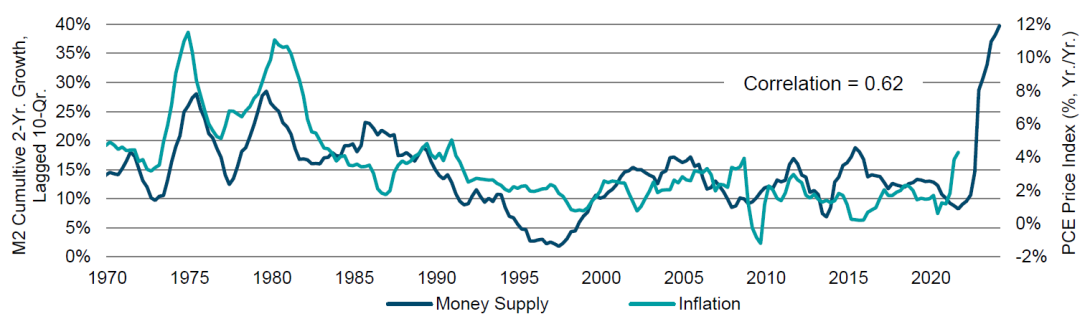

As the economy has recovered, inflation concerns have taken center stage. Consumer prices soared 7.1% year-over-year in 2021, the most since the early-1980s; the Federal Reserve’s (Fed) preferred measure, which strips out surging food and energy prices, jumped the most since 1989 (4.7% year-over-year in November 2021).16 There has been a raging debate about whether inflation is transitory or more persistent. We believe that transitory supply-side issues have played a role. Yet it is also worth noting that the Federal Reserve has more than doubled its balance sheet, creating more than $4 trillion in base money.17 While the Fed embarked on a similar program during the GFC without igniting inflation, this latest iteration differs in two respects: First, it amounts to roughly twice the stimulus over a third of the time (two years instead of six). Second, unlike during the GFC, when much of the liquidity was trapped in a broken financial system, this time it has entered circulation via debt-financed fiscal channels. The result: Broad (“M2”) money supply has jumped 40%, an order of magnitude above anything seen in more than 50 years (see Exhibit 1).18 Experience from the 1970s suggests that money growth can feed inflation with a lag of two to three years.19 Regardless of the catalyst, once ignited, inflation can become self-perpetuating if it is embedded in expectations, spawning a wage-price spiral.

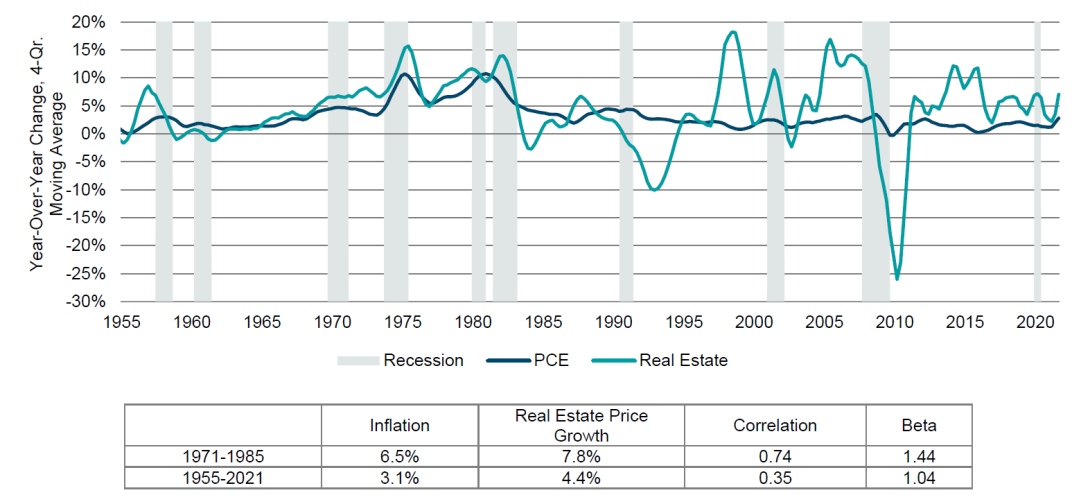

Sources: U.S. Bureau of Labor Statistics, U.S. Board of Governors of the Federal Reserve System as of December 2021. The “transitory versus persistent” debate has not been conclusively settled. However, it has rekindled interest among investors in strategies to mitigate inflation risks. Property has traditionally been viewed as an inflation hedge, and for good reason: Commercial real estate has historically exhibited a strong correlation and an even stronger sensitivity (or “beta”) to rising price levels (see Exhibit 2).20 These relationships appeared even more powerful during the 1970s and early-1980s, when inflationary pressures were more acute. There are two mechanisms through which inflation feeds into real estate prices: Rising (nominal) wages and sales can augment renters’ spending power. Higher construction costs can also constrain competitive supply. Materials prices soared 35% year-over-year in November, while a broader measure that includes wages increased 14% — the fastest increases in 50-70 years.21 Over time, real estate prices have tracked replacement costs, which are directly tied to inflation.

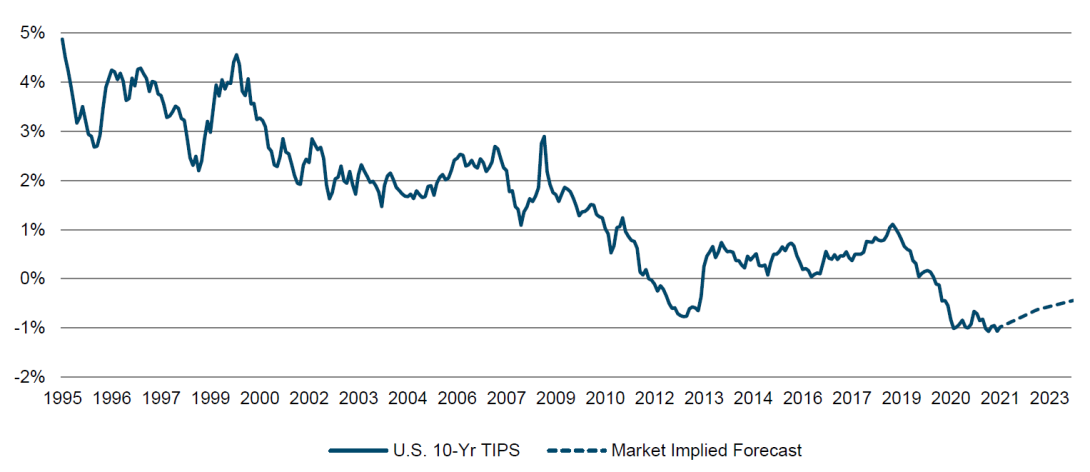

Sources: U.S. Bureau of Labor Statistics, U.S. Board of Governors of the Federal Reserve System as of December 2021. With inflation mounting, the Federal Reserve has signaled its intention to suspend asset purchases in March and lift short-term interest rates several times in 2022. Some investors may wonder whether higher interest rates will undermine real estate valuations. We do not believe so, for several reasons. First, monetary tightening will not necessarily translate into higher long-term interest rates. Second, even if long-term rates were to increase, they should not be divorced from the inflationary context. Given that property is a real asset whose cash flows and intrinsic value increase with inflation (unlike nominal Treasuries), we believe that its valuations are driven more by real interest rates. Real yields (measured by the 10-year Treasury Inflation Protected Security (TIPS)) have hardly moved from their record lows of about -1%, and futures markets imply that they will remain below -60 basis points through 2022 (see Exhibit 3).22 Third, the spread between cap rates and TIPS yields, about 500 basis points (bps), is well above its long-term average (400 bps), suggesting that there is room for real estate to absorb any upward pressure on real rates.23

Sources: U.S. Board of Governors of the Federal Reserve System, Bloomberg as of December 2021.

There are risks to the outlook. In the near-term, the COVID Omicron variant introduces risks to the economy and therefore leasing fundamentals. We believe that any disruption is unlikely to derail the expansion: Americans have learned to manage through COVID flare-ups; vaccines, boosters, and therapies promise at least a partial antidote; and there appears to be limited political appetite to impose draconian restrictions. Nevertheless, more adverse scenarios cannot be ruled out. Over the medium-term, there is a risk that the inflationary rebound currently underway may ultimately necessitate a more forceful Fed response, reminiscent of the early-1980s under Chairman Paul Volcker, that would tip the economy into recession. Still, today’s upward-sloping yield curve suggests that recession risks are several years off. For now, we believe that robust economic growth, elevated inflation, and low real interest rates set the stage for a strong real estate market in 2022 and likely beyond.

1 NCREIF. As of September 2021.

2 NCREIF. As of September 2021.

3 Real Capital Analytics. As of September 2021.

4 NCREIF. As of September 2021.

5 CBRE-EA. As of September 2021.

6 CBRE-EA. As of September 2021.

7 CBRE-EA. As of December 2021.

8 CBRE-EA. As of December 2021.

9 CBRE-EA. As of December 2021.

10 NCREIF (valuations); Moody’s Analytics (CMBS delinquencies). As of October 2021.

11 Kastle (office usage); NCREIF (NOI). As of December 2021.

12 CBRE-EA. As of December 2021.

13 Moody’s Analytics (fiscal stimulus); DWS (GDP growth). As of December 2021.

14 Case-Shiller (home prices); S&P 500 (stock prices); DWS (savings). As of December 2021.

15 DWS. As of December 2021.

16 Census Bureau (consumer prices); Bureau of Economic Analysis (Fed’s preferred personal consumption expenditure price index). As of December 2021.

17 Federal Reserve. As of December 2021.

18 Federal Reserve. As of December 2021.

19 Federal Reserve (money supply); Bureau of Economic Analysis (inflation); DWS. As of December 2021.

20 Federal Reserve (commercial real estate prices); Bureau of Economic Analysis (inflation); DWS. As of December 2021.

21 Census Bureau (construction materials costs); Engineering News-Record (building costs). As of November 2021.

22 Bloomberg. As of December 2021.

23 NCREIF (cap rates); Federal Reserve (TIPS); DWS (spreads). As of September 2021.

Kevin White, CFA Global Co-Head of Real Estate Research

This information is subject to change at any time, based upon economic, market and other considerations and should not be construed as a recommendation. Past performance is not indicative of future returns. Forecasts are not a reliable indicator of future performance. Forecasts are based on assumptions, estimates, opinions and hypothetical models that may prove to be incorrect. Investments come with risk. The value of an investment can fall as well as rise and your capital may be at risk. You might not get back the amount originally invested at any point in time. Source: DWS Investment GmbH The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services. There may be references in this document which do not yet reflect the DWS Brand. Please note certain information in this presentation constitutes forward-looking statements. Due to various risks, uncertainties and assumptions made in our analysis, actual events or results or the actual performance of the markets covered by this presentation report may differ materially from those described. The information herein reflects our current views only, is subject to change, and is not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have opined herein. Marketing Material. In EMEA for Professional Clients (MiFID Directive 2014/65/EU Annex II) only; no distribution to private/retail customers. In Switzerland for Qualified Investors (art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). In APAC for institutional investors only. Australia and New Zealand: For Wholesale Investors only. In the Americas for Institutional Client and Registered Rep use only, not for public viewing or distribution. Israel: For Qualified Clients (Israeli Regulation of Investment Advice, Investment Marketing and Portfolio Management Law 5755-1995). *For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda.

IMPORTANT INFORMATION

For North America: The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services. This material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only. It does not constitute investment advice, a recommendation, an offer, solicitation, the basis for any contract to purchase or sell any security or other instrument, or for DWS or its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Neither DWS nor any of its affiliates gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Except insofar as liability under any statute cannot be excluded, no member of the DWS, the Issuer or any office, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered by the recipient of this document or any other person. The views expressed in this document constitute DWS Group’s judgment at the time of issue and are subject to change. This document is only for professional investors. This document was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. No further distribution is allowed without prior written consent of the Issuer. Investments are subject to risk, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount originally invested at any point in time. An investment in real assets involves a high degree of risk, including possible loss of principal amount invested, and is suitable only for sophisticated investors who can bear such losses. The value of shares/ units and their derived income may fall or rise. War, terrorism, economic uncertainty, trade disputes, public health crises (including the recent pandemic spread of the novel coronavirus) and related geopolitical events could lead to increased market volatility, disruption to U.S. and world economies and markets and may have significant adverse effects on the global real estate markets. For Investors in Canada. No securities commission or similar authority in Canada has reviewed or in any way passed upon this document or the merits of the securities described herein and any representation to the contrary is an offence. This document is intended for discussion purposes only and does not create any legally binding obligations on the part of DWS Group. Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation relating to the transaction you are considering, and not the [document – may need to identify] contained herein. DWS Group is not acting as your financial adviser or in any other fiduciary capacity with respect to any transaction presented to you. Any transaction(s) or products(s) mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand such transaction(s) and have made an independent assessment of the appropriateness of the transaction(s) in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DWS Group, you do so in reliance on your own judgment. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates, and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on a number of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Past performance is not a guarantee of future results. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. You may not distribute this document, in whole or in part, without our express written permission.

For EMEA, APAC & LATAM: DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they do business. The DWS legal entities offering products or services are specified in the relevant documentation. DWS, through DWS Group GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) are communicating this document in good faith and on the following basis. This document is for information/discussion purposes only and does not constitute an offer, recommendation, or solicitation to conclude a transaction and should not be treated as investment advice. This document is intended to be a marketing communication, not a financial analysis. Accordingly, it may not comply with legal obligations requiring the impartiality of financial analysis or prohibiting trading prior to the publication of a financial analysis. This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models, and hypothetical performance analysis. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements. Past performance is no guarantee of future results. The information contained in this document is obtained from sources believed to be reliable. DWS does not guarantee the accuracy, completeness, or fairness of such information. All third-party data is copyrighted by and proprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notify the recipient in the event that any matter stated herein, or any opinion, projection, forecast, or estimate set forth herein, changes or subsequently becomes inaccurate. Investments are subject to various risks. Detailed information on risks is contained in the relevant offering documents. No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. DWS does not give taxation or legal advice. This document may not be reproduced or circulated without DWS’s written authority. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, including the United States, where such distribution, publication, availability, or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions. © 2022 DWS International GmbH Issued in the UK by DWS Investments UK Limited which is authorised and regulated by the Financial Conduct Authority (Reference number 429806). © 2022 DWS Investments UK Limited In Hong Kong, this document is issued by DWS Investments Hong Kong Limited and the content of this document has not been reviewed by the Securities and Futures Commission. © 2022 DWS Investments Hong Kong Limited In Singapore, this document is issued by DWS Investments Singapore Limited and the content of this document has not been reviewed by the Monetary Authority of Singapore. © 2022 DWS Investments Singapore Limited In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission. © 2022 DWS Investments Australia Limited For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation. For investors in Taiwan: This document is distributed to professional investors only and not others. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed, and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction, or transmission of the contents, irrespective of the form, is not permitted.

© 2022 DWS Group GmbH & Co. KGaA. All rights reserved. (1/22) 080949_3

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in