Low interest rates, pent-up demand for growth, and major advances in IT infrastructure have made it easier for software companies to start up and scale. As Marc Andreessen predicted, software has eaten the world, gobbling up a massive share of private and public markets alike, and generating strong performance for investors in the process.1 As a result, the last decade has been very good to the venture capital (VC) industry. Venture-backed software and internet companies now account for seven of the 10 largest companies in the world. Returns have improved markedly over the prior decade and are now largely outperforming buyouts. Investments and exits are at all-time highs. Can it last?

We tend to think so. Despite the excesses of the tech market and the parallels to the dot-com bubble, risk-reward in VC has actually improved. We believe the rise of software and SaaS as a business model explain why: They have offered high margins, recurring revenues, and opportunities to apply artificial intelligence to monetize data. There are also more investment strategies than ever for LPs to consider.

We expect software to continue penetrating other sectors of the economy. This growth opportunity and the resiliency of the SaaS business model should enable VC to outperform, powering the IPO, M&A, and buyout markets in the process.

The VC Boom

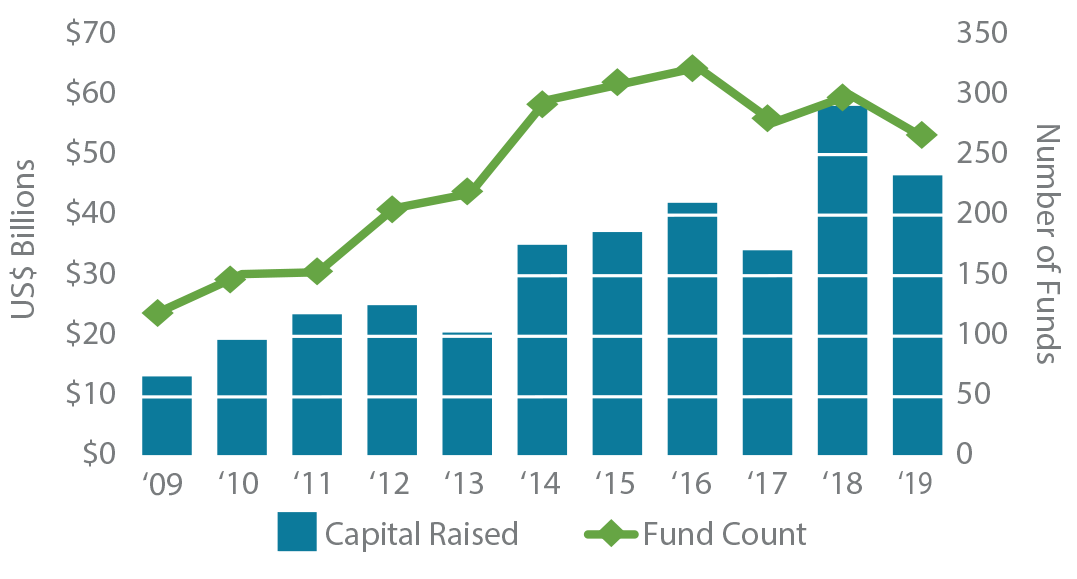

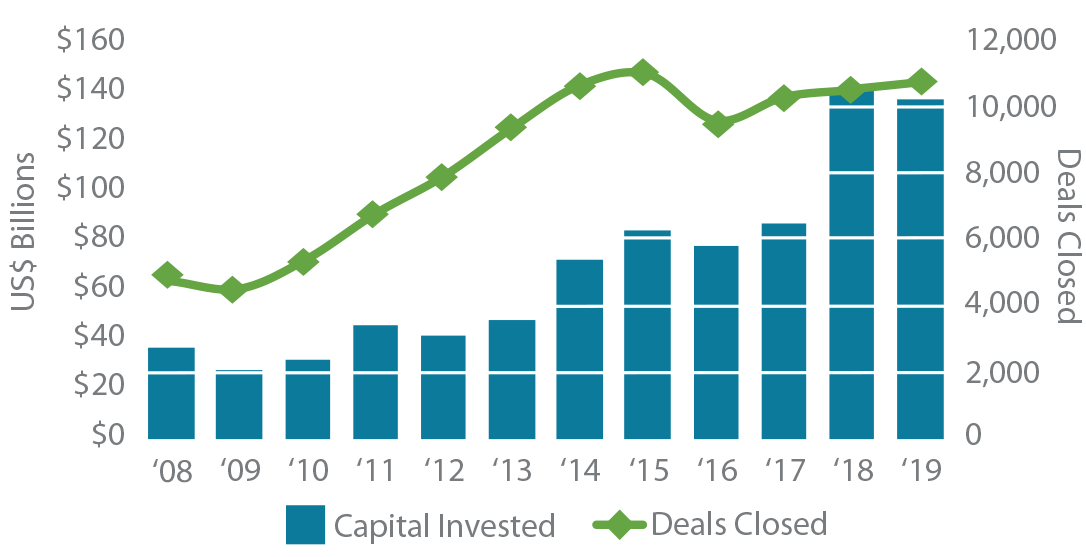

A decade of expansion in VC has led to a number of recent milestones, including a record amount of capital invested in VC-backed companies in 2018 and a record amount of liquidity in 2019. It has clearly been a golden era for VC.

As seen in Figures 1–3, 2018 was a banner year, and that momentum largely continued into 2019. The IPOs of high-profile companies Uber, Zoom, Slack, Pinterest, and Lyft led the way for what was a record year for exit value. This is certainly a welcome development for the LPs that have waited a decade or more to realize these gains and have been constrained in their ability to commit more capital to the asset class.

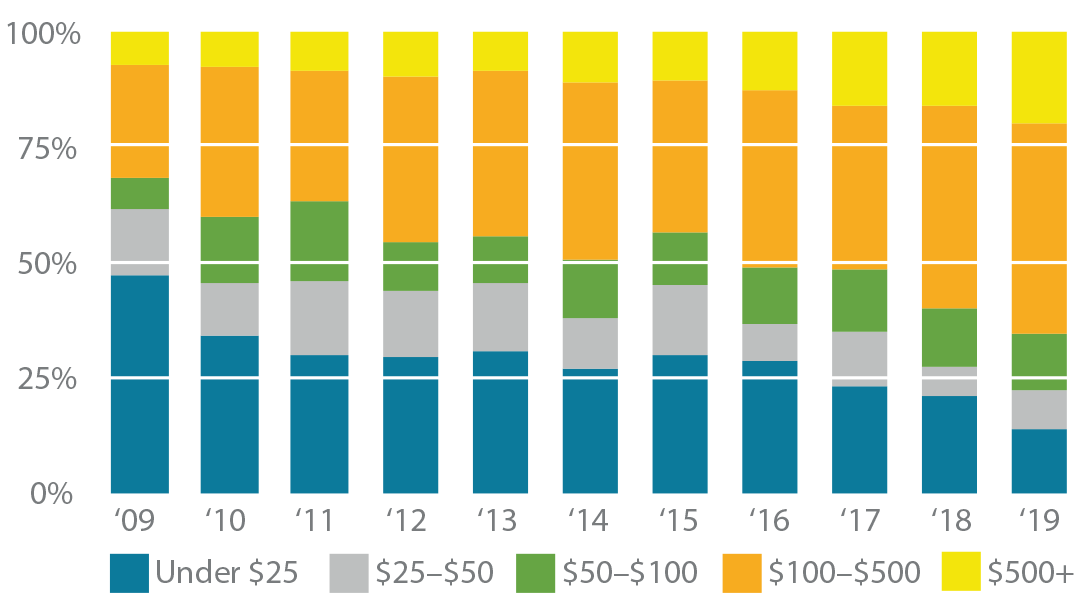

A clear separation between the “haves” and “have nots” has emerged. The 25 largest VC managers have collectively raised more than 50% of all LP commitments over the last decade (even excluding the US$100 billion SoftBank Vision Fund). At the same time, hundreds of new seed funds have emerged. In 2018, funds smaller than US$250 million may have accounted for 74% of all new VC funds raised, but they represented only 16% of the total dollars raised. By contrast, funds larger than US$500 million accounted for 12% of new funds raised, but represented 66% of the total capital raised.2

One consistent concern among venture GPs and LPs has been the massive rise in valuations. This inflation of pre-money values has occurred at every stage, but it is most apparent in the late-stage market (Figure 4). In prior eras, many of the late-stage, high-valuation companies would have pursued IPOs much earlier in their life cycle; today these “unicorns” are happy to raise money on more favorable terms in private markets while avoiding the glare of the public markets.

FIGURE 1 | US VC FUNDRAISING

Source: PitchBook, December 2019.

FIGURE 2 | US VC EXIT ACTIVITY

Source: PitchBook, December 2019.

FIGURE 3 | US VC DEAL ACTIVITY

Source: PitchBook, December 2019.

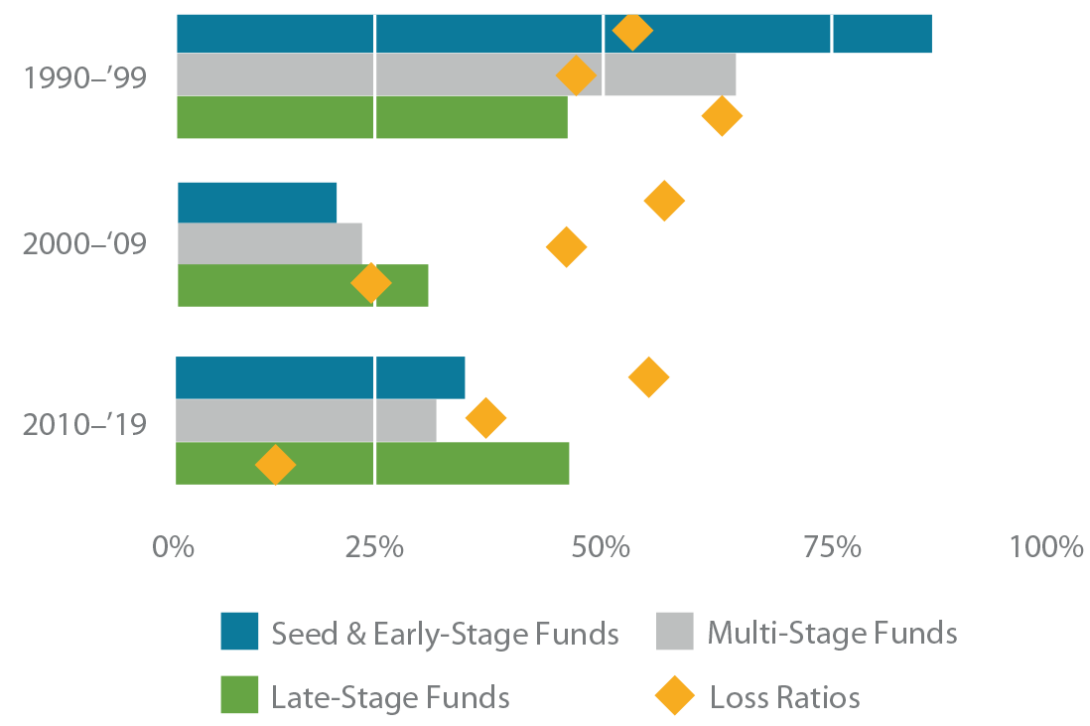

Loss rates for late-stage venture have declined sharply since 2000.

FIGURE 4 | US MEDIAN PRE-MONEY VALUATION (US$M)

Source: PitchBook, December 2019.

BIGGER EXITS BUT LONGER TIME TO LIQUIDITY

Although overall exit activity has improved in VC, the time to liquidity for technology companies has soared. Unlike in the late 1990s, the companies going public today are older and much larger (Figure 5). According to Jay Ritter of the University of Florida, the median revenue at IPO for tech companies in 2018 was US$167 million versus a mere US$17 million in 1999.

Changes in the market and regulatory environment since 2000 are among the reasons companies have to meet a higher standard before they can go public. Rules like Sarbanes-Oxley and Regulation Fair Disclosure have raised the cost of being a public company. The abundance of private capital, epitomized by the massive SoftBank Vision Fund, has made it more attractive for companies to remain private for longer; they can continue to raise capital on attractive terms from a variety of late-stage investors including mega funds, crossover funds, corporates, and sovereign wealth funds.

Although the time to liquidity has extended significantly, thankfully, exit values have also increased for VC-backed companies. In 2019, VC-backed exits generated nearly US$260 billion across 882 transactions in the US alone (Figure 6). Total exit value for the year was 162% higher than the rolling five-year average even though there were 11% fewer deals.

FIGURE 5 | MEDIAN AGE OF TECH COMPANIES AT IPO (YEARS)

Source: Jay Ritter, 2016.

FIGURE 6 | US VC EXIT ACTIVITY BY SIZE (US$M)

Source: PitchBook, December 2019.

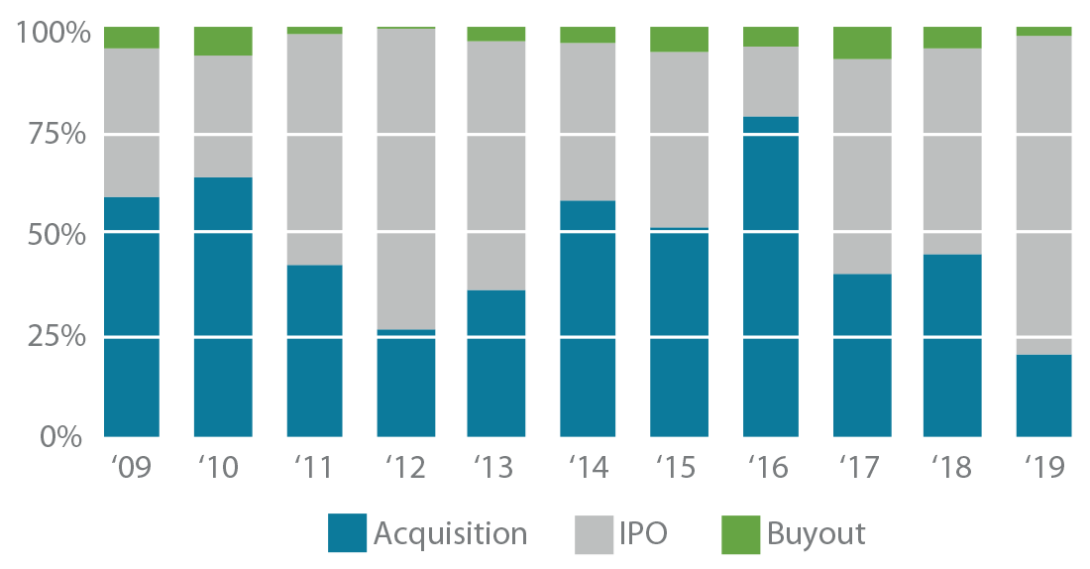

FIGURE 7 | US VC EXIT VALUE BY TYPE ($B)

Source: PitchBook, December 2019.

As in the LP fundraising market, there has been a greater concentration of value in a handful of the largest exits, and the value is disproportionately coming from IPOs. More than 80% of exit value through 1H19 has come from IPOs (Figure 7).

VC RETURNS HAVE IMPROVED

After a decade of underperformance, top quartile VC funds have largely outperformed buyouts (Figure 8). Despite this strong performance, liquidity in VC has lagged the buyout sector. Many LPs have not been rewarded with returns commensurate with the risks they have undertaken. VC remains a game of outliers, with a handful of massive outcomes generating the majority of returns each vintage year. The dispersion of returns is greater in VC than in any other asset class. Manager selection is critical.

FIGURE 8 | NET IRR BY VINTAGE YEAR

Source: StepStone Private Markets Intelligence, 2019.

EMERGING MANAGERS DRIVE OUTPERFORMANCE

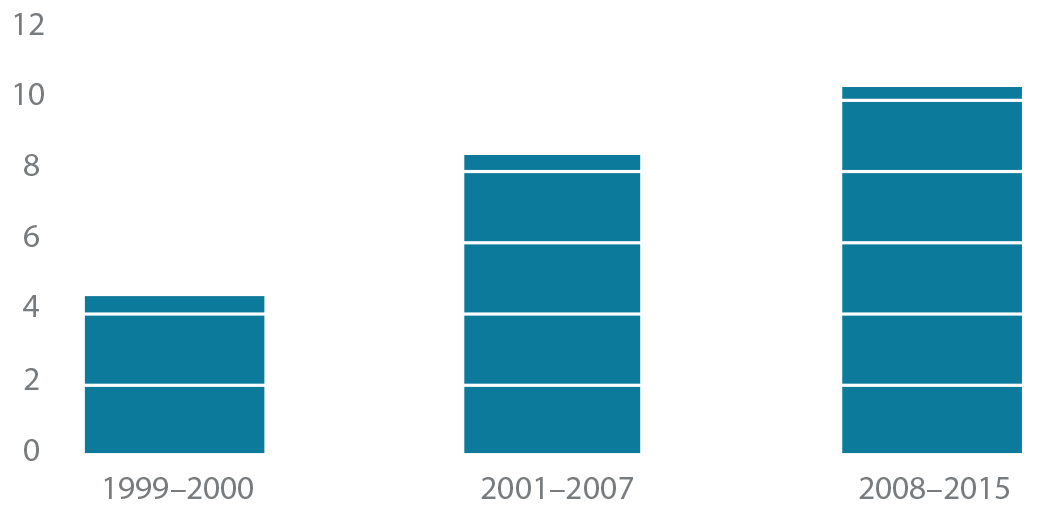

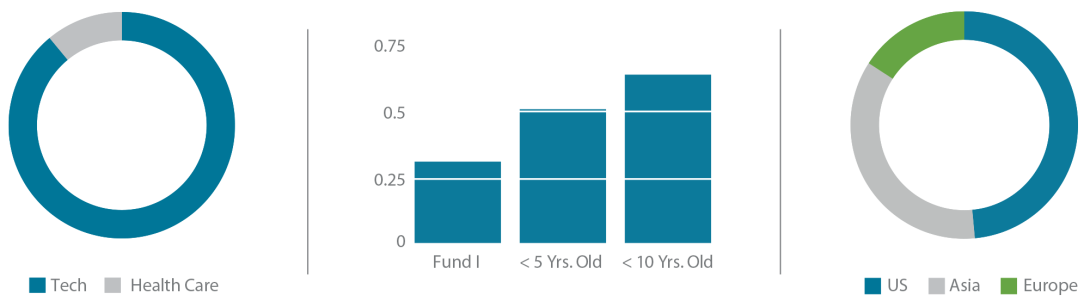

We analyzed the age, sector and geographic characteristics of the Top 5 performing VC funds of each vintage from 2007 to 2015. First-time funds accounted for nearly a third of the top performing funds (Figure 9).

Overwhelmingly, Top 5 funds focused on the technology sector. That shouldn't come as a surprise; that more than half of the best performing funds were raised by non-US GPs may.

FIGURE 9 | CHARACTERISTICS OF TOP PERFORMING VC FUNDS (2007-2015)

Source: Preqin, StepStone, September 2019.

GLOBALIZATION OF THE VENTURE INDUSTRY

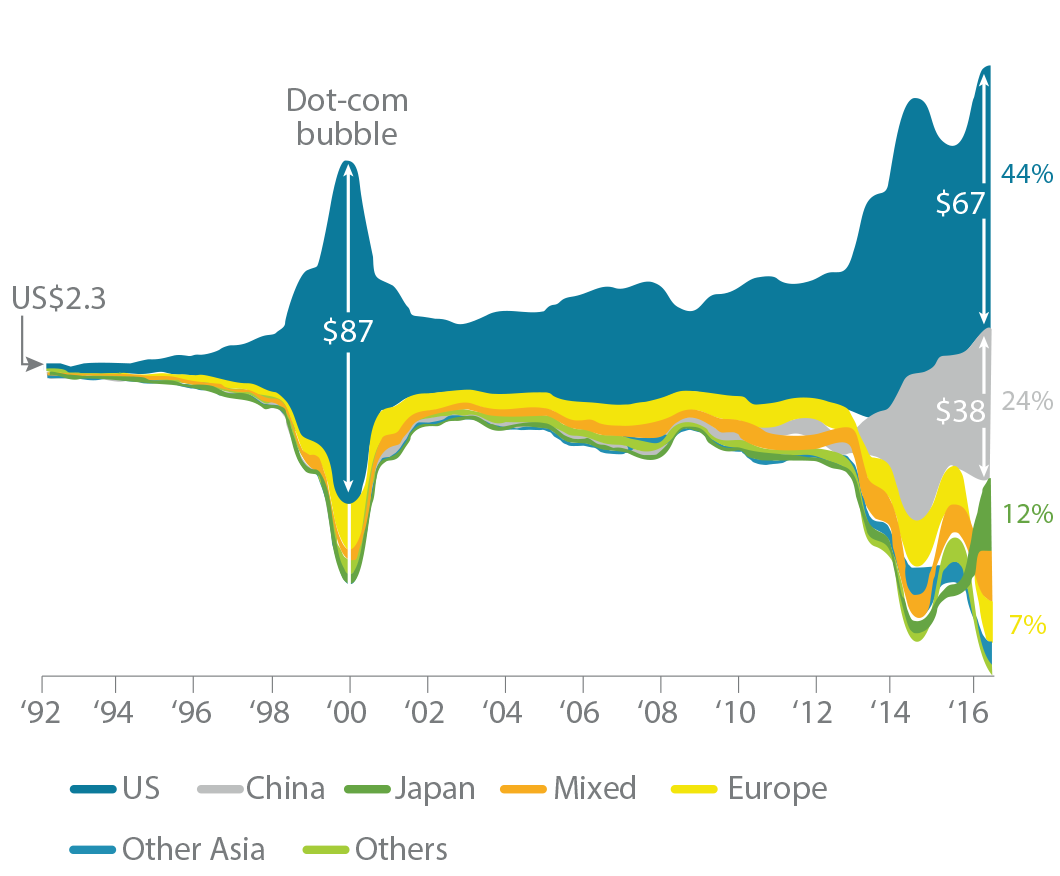

As seen in Figure 10, VC has become a global asset class. Driven in large part by China and Japan, Asia VC has grown swiftly alongside the region's major economies where an affluent middle class and the rise of mobile technologies have converged to create a flourishing start-up community.

FIGURE 10 | VENTURE CAPITAL BY PLACE OF ORIGIN (US$B)

Source: The Wall Street Journal, April 2018.

Note: SoftBank is the bulk of the Japan total.

WIDER SPECTRUM OF VC STRATEGIES

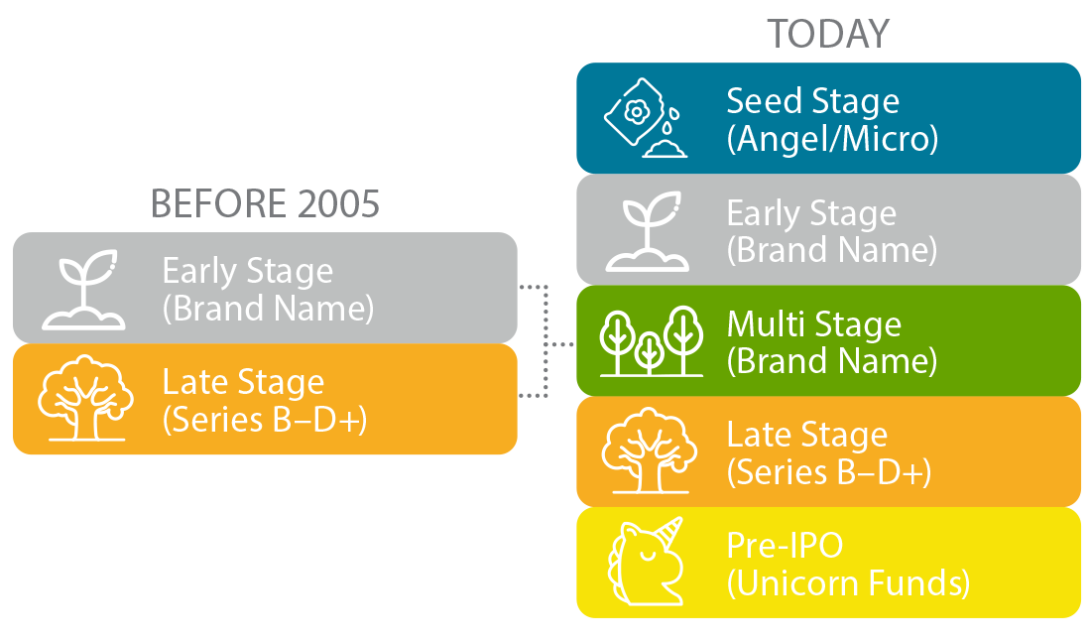

Twenty years ago, there were two primary types of VC strategies available to LPs; early-stage funds focused on Series A rounds, and late-stage funds investing in Series B or later (Figure 11). Over the last 15 years, new types of venture capitalists have emerged including seed funds (e.g., First Round Capital), accelerators (e.g., Y Combinator), incubators (e.g., Rocket Internet), and crowdfunding platforms (e.g., AngelList). Advances in cloud computing, open source software, and mobile networks have dramatically reduced the cost of starting new software businesses, which has driven an explosion of new startups. This new IT infrastructure has reduced the cost of failure; companies no longer have to invest significant capital in hardware, servers, and proprietary software to launch their businesses. Instead they can leverage Amazon Web Services for computing resources and Apple iOS and Android for distribution.

FIGURE 11 | WIDER SPECTRUM OF VC STRATEGIES

Source: StepStone, 2020.

Despite the clear benefits of this new infrastructure, we found that loss rates in seed and early-stage VC have remained steady at more than 50% over the last three decades. Seed-stage VC was particularly compelling a decade ago when pre-money valuations were typically less than US$5 million, and there were fewer funds active in the space. Today pre-money valuations on seed rounds have more than doubled to US$7.6 million, and hundreds of small funds are writing first checks to startups. Furthermore, as exit values have become concentrated in a handful of large IPOs, the number of small M&A exits has declined, damaging the prospects for seed funds that were accustomed to selling companies to Google or Facebook.

The rising challenges in the seed space notwithstanding, the potential for an LP to generate a 3x net multiple on a seed VC fund commitment is still greater than with larger funds. Our data indicate that 25% of the deals pursued by sub–US$100 million funds have delivered a 3x return or greater, whereas only 15% of deals pursued by funds in the US$500 million to US$1 billion range have generated at least 3x (Figure 12). Although the returns in seed VC have been attractive over the last cycle, many LPs choose to not focus on the category. Deploying capital at scale remains challenging, and low barriers to entry have allowed many new players to enter the space.

FIGURE 12 | GROSS TVM OF VC DEALS BY FUND SIZE

Source: StepStone Private Markets Intelligence, 2019.

The long hold periods and winner-take-all market dynamics inherent in IT have in many ways shifted the advantage to larger “brand name” VC funds, which have the capacity to invest in their best companies throughout their life cycle. These larger funds focus on Series A rounds but have the flexibility to invest from seed to pre-IPO. Premium fees and massive fund sizes often require these GPs to effect multiple US$10 billion+ outcomes per fund, something that very few have been able to do consistently.

Although our data show seed and early-stage loss rates have remained above 50% over the last 30 years, loss rates for late-stage venture have declined sharply since 2000 (Figure 13). We believe a large driver of this is the rise of software as a dominant VC category. Advances in IT infrastructure have reduced the cost of failure at the early-stage, and the high visibility that recurring-revenue SaaS business models affords is enabling later-stage investors to avoid throwing good money after bad. This improvement in the risk-reward dynamic helps explain the ongoing boom in late-stage VC.

FIGURE 13 | GROSS IRR & LOSS RATIOS BY ERA

Source: StepStone Private Markets Intelligence, 2019.

Note: Gross IRR will ultimately be reduced by management fees, carried interest, taxes, and other fees and expenses.

Investments from late-stage GPs (typically Series B or later) have outperformed seed, early-stage, and multi-stage VC funds on average, with a higher gross IRR and TVM and a lower loss ratio. Whereas loss ratios for early-stage VC have held steady at about 50% on average over the last three decades, the loss ratios for late-stage investments have decreased significantly from 59% in the 1990s to 15% in the 2010s.

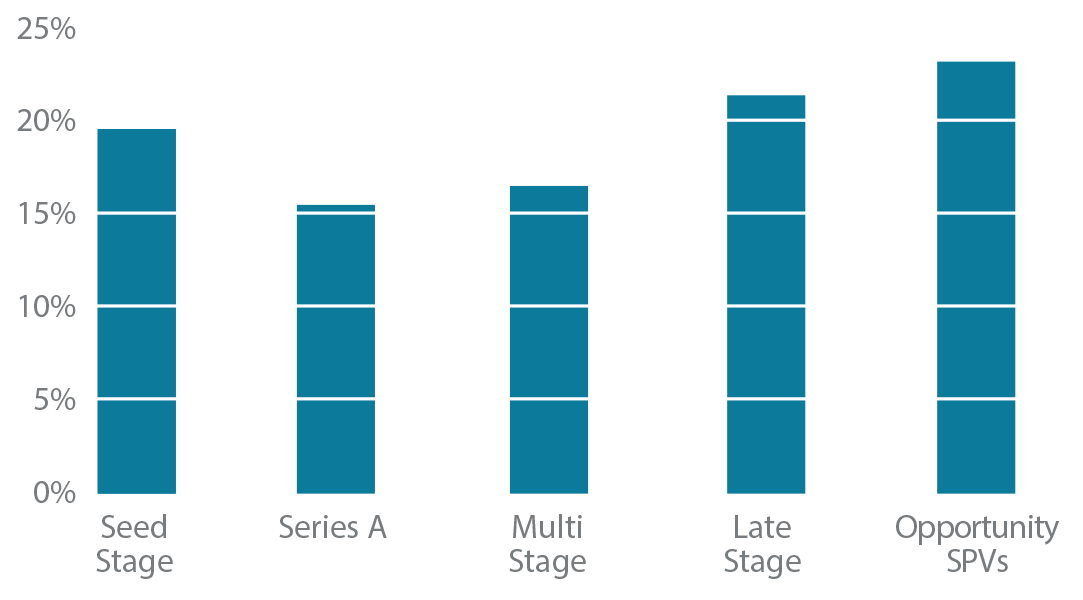

We analyzed net return data for 462 venture and growth equity funds raised since 2005. As seen in Figure 14, the top performers were late-stage VC and opportunity funds, which target late-stage companies.

FIGURE 14 | MEDIAN NET IRR BY STAGE

Source: StepStone Private Markets Intelligence, January 2020.

These data help explain why the amount of capital deployed in late-stage rounds has exploded over the last several years. Recurring-revenue software companies that have achieved product-market fit and maintain low customer churn, represent compelling investment opportunities at all stages. The high visibility afforded by SaaS business models has revolutionized VC, with company selection seemingly becoming much easier. The best “platform” companies have extreme product-market fit and are growing rapidly thanks in part to network effects and the barriers to entry they provide. Accessing these companies, however, is easier said than done; everyone wants a piece of these clear winners. Most VC funds no longer take on technical risk. Instead they seek to deploy capital into proven companies. This dynamic is reverberating throughout the sector, affecting VC strategies at all stages.

For example, most seed funds now prefer revenue-stage businesses, and the majority of VC funds have become “momentum” investors, avoiding technical risk and targeting companies with products in market. This is of course a byproduct of the significant advances in IT infrastructure over the last 15 years (e.g., cloud computing, and DevOps). It is now much cheaper to start a software company. Reaching the scale, however, to meet global demand requires a lot of growth capital, the provision of which has become the raison d’être of the venture industry.

This dynamic helps explain the rise of mega multi–stage VC funds, new entrants to the late-stage market (e.g., SoftBank Vision Fund), opportunity funds, and special purpose vehicles (SPVs), which enable early-stage investors to continue to deploy late-stage capital into their best companies.

Most VC funds no longer

take on technical risk.

OPPORTUNITY FUNDS, SPVS AND LP CO-INVESTMENT

In exchange for taking on the risk inherent in seed and Series A rounds, early-stage funds receive meaningful pro rata rights to invest in later rounds. But their smaller fund sizes and higher return targets are often not a fit for higher-valuation late-stage rounds. Opportunity funds, SPVs, and LP co-investments allow early-stage GPs to continue backing their best companies. They also offer LPs a compelling way to scale their relationships with these smaller funds. In our view, the most interesting opportunity funds are those with significantly reduced (or no) management fees and a clear pipeline of investment opportunities.

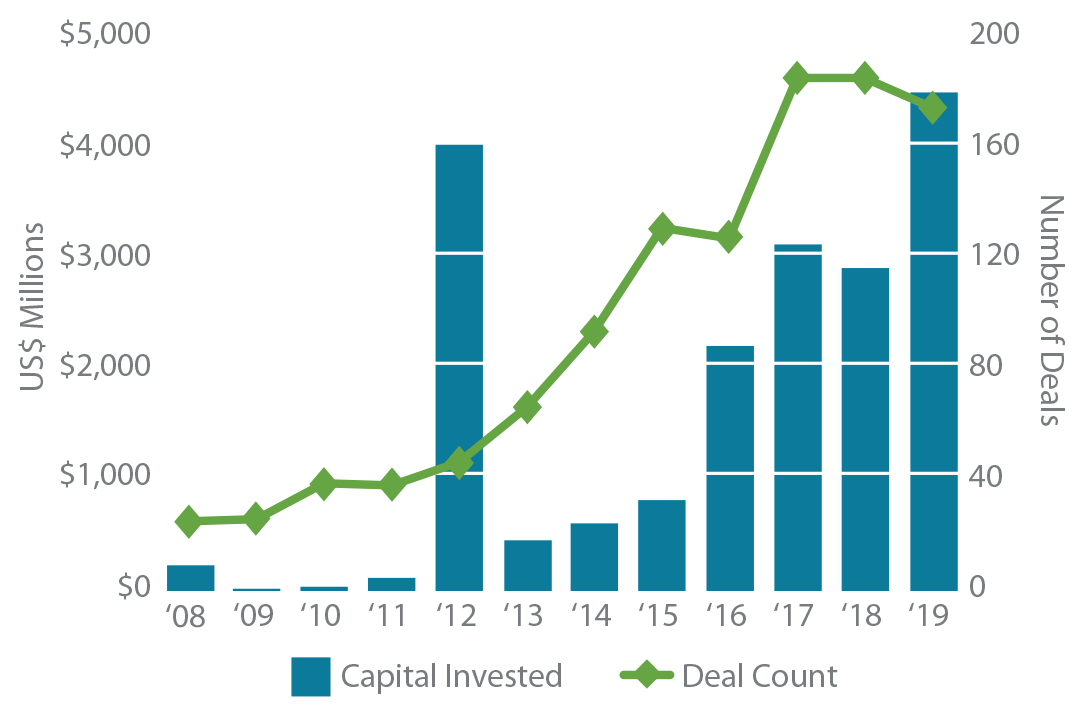

RISE OF THE SECONDARY MARKET

With hold periods in the best VC-backed companies often exceeding a decade, secondaries have become a critical liquidity component for GPs, LPs, and employees; they provide yet another way to gain exposure to blue-chip companies. VC funds generally trade at a greater discount than buyout funds since the values of the underlying assets tend to be more volatile and the time to liquidity less certain. For LPs seeking to build VC exposure, secondaries can be a less risky way to access the VC market.

Although separate from LP secondaries, the direct secondary market has also been growing rapidly (Figure 15). As many of the most important pre-IPO companies have waited 10 or more years to go public, their shareholders are seeking liquidity for their stakes.

FIGURE 15 | GLOBAL SECONDARY TRANSACTIONS IN VC-BACKED COMPANIES

Source: PitchBook, January 2020.

Looking Ahead

Despite the warning signs, we believe the future is bright for VC. Revenue multiples are likely to decline substantially if and when market sentiment worsens. At the same time, quality software companies with market-leading products, recurring revenues, and low customer churn could weather an economic downturn and gain market share. Software and SaaS business models have transformed the technology industry, and we expect software to continue eating the world. Financial services, health care, agriculture, and energy remain underpenetrated by software and are undergoing technology disruption and rapid change. With the pace of technological innovation continuing unabated, and trends such as artificial intelligence, automation, and blockchain powering a new wave of companies, we believe the future is bright for VC.

Conclusion

Although high valuations and greater competition at every stage might suggest VC is peaking, StepStone believes the sector remains attractive for LPs willing to devote the time and effort to construct the right portfolio. Seed and earlystage funds still offer the best path to outsize returns, but LPs must grapple with volatility and long hold periods. Latestage strategies have become more attractive as the time to liquidity for the best companies has lengthened. There are more data than ever to evaluate young companies; network effects are creating barriers to entry. As such, late-stage investing has become less about company selection and more about accessing companies that appear to be on a path to an IPO.

Quality software companies with market-leading products, recurring revenues, and low customer churn should be well positioned to weather an economic downturn. As software continues to penetrate all sectors of the economy, and new waves of innovation such as artificial intelligence and blockchain disrupt the incumbents, we expect VC to continue driving significant value in the economy and for LPs.

1 Andreessen, Marc. 2011. “Why Software Is Eating the World.” The Wall Street Journal, August 20.

2 Rowley, Jason D. 2019. "There Are More VC Funds Than Ever, But Capital Concentrates At The Top." Crunchbase, March 7.

Read the full article here

This document is for information purposes only and has been compiled with publicly available information. StepStone makes no guarantees of the accuracy of the information provided. This information is for the use of StepStone’s clients and contacts only. This report is only provided for informational purposes. This report may include information that is based, in part or in full, on assumptions, models and/or other analysis (not all of which may be described herein). StepStone makes no representation or warranty as to the reasonableness of such assumptions, models or analysis or the conclusions drawn. Any opinions expressed herein are current opinions as of the date hereof and are subject to change at any time. StepStone is not intending to provide investment, tax or other advice to you or any other party, and no information in this document is to be relied upon for the purpose of making or communicating investments or other decisions. Neither the information nor any opinion expressed in this report constitutes a solicitation, an offer or a recommendation to buy, sell or dispose of any investment, to engage in any other transaction or to provide any investment advice or service.

Past performance is not a guarantee of future results. Actual results may vary.

Each of StepStone Group LP, StepStone Group Real Assets LP and StepStone Group Real Estate LP is an investment adviser registered with the Securities and Exchange Commission (“SEC”). StepStone Group Europe LLP is authorized and regulated by the Financial Conduct Authority, firm reference number 551580. Swiss Capital Invest Holding (Dublin) Ltd (“SCHIDL”) is an SEC Registered Investment Advisor and Swiss Capital Alternative Investments AG (“SCAI”) (together with SCHIDL, “SwissCap”) is registered as a Relying Advisor with the SEC. Such registrations do not imply a certain level of skill or training and no inference to the contrary should be made.

Manager references herein are for illustrative purposes only and do not constitute investment recommendations.