Recent proposed rule changes from the National Association of Insurance Commissioners (NAIC) could alter the regulatory treatment of securitized assets—long a staple of US insurance companies’ core portfolios. It’s crucial for asset allocators to understand the potential magnitude, direction and timing of the first significant changes since 2008 as they consider portfolio positioning.

While the proposed updates to risk-based capital (RBC) charges on collateralized loan obligations (CLOs) have attracted the most attention so far, they’re certainly not the only changes. We review four key pillars of the potential regulatory updates and what they might mean for insurers’ securitized exposure.

1) CLO Risk Assessment and the Impact on NAIC RBC Charges

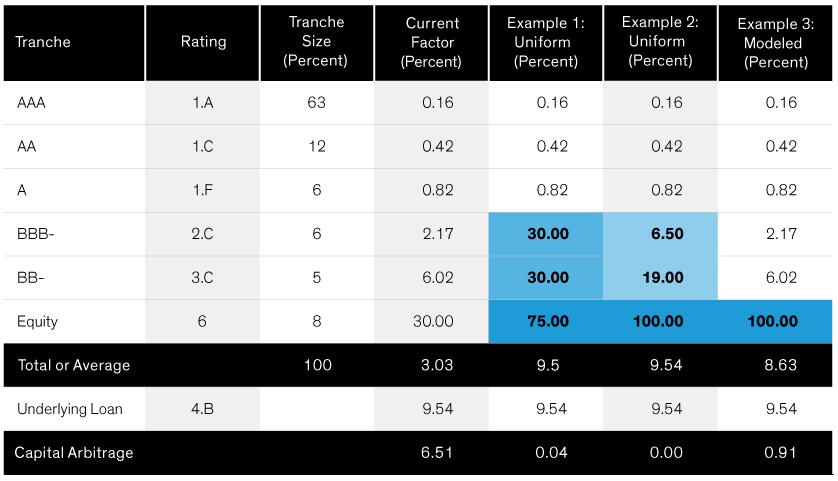

The NAIC is seeking to reduce or remove the perceived risk-capital-arbitrage opportunity stemming from holding a higher-rated CLO versus the underlying loan collateral. As the Display below illustrates, the current weighted-average risk factor for an entire sample CLO structure is 3.03%, while the underlying collateral’s risk factor is 9.54%—assuming B-rated loans. That’s a sizable difference of about 6.5%.

A few ideas are being considered to address the discrepancy. One is to uniformly increase risk factors applied to BBB and BB rated CLO tranches (examples 1 and 2 below). Another idea is to expand NAIC category 6 into three subcategories (A, B and C), with risk factors of 30%, 75% and 100%, respectively; today, the category carries a flat 30% factor. In example 3, increasing NAIC 6 charges to 100%, while keeping charges on categories 2.C and 3.C the same, would bring average RBC charges to 8.63%, about 90% of charges under 4.B. Expanding the NAIC 6 categories and increasing RBC charges would likely be the most impactful approach.

Addressing Capital Arbitrage in CLOs

Percentage Factors Under Current and Potential Frameworks

Current analysis does not guarantee future results.

As of August 15, 2022

Source: Bank of America, Citigroup, NAIC and AllianceBernstein (AB)

Our Assessment: This provision would likely take some time to implement. No official proposal exists yet and changing the NAIC factors would affect insurers’ RBC filings, requiring updates from vendors. Adopting a modeled approach could expedite the process and enable high-quality tranches to benefit from an RBC designation upgrade. But this could also mean significant capital increases from downgrades to BBB and lower-rated tranches, including equity.

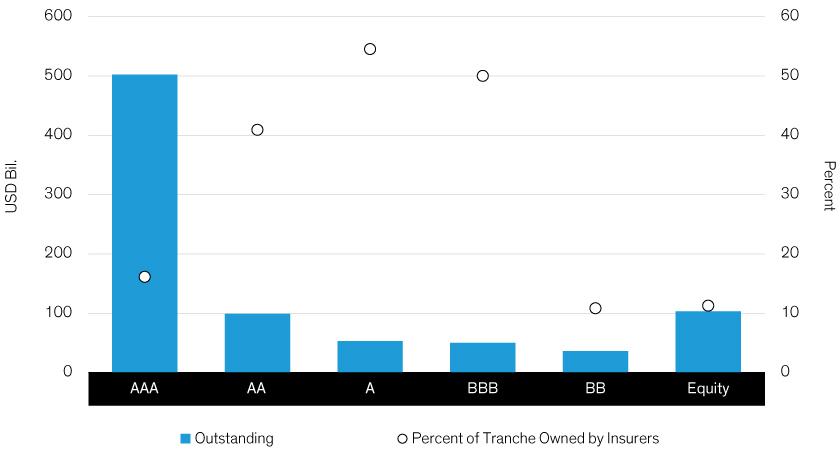

We believe that a modeled approach could benefit certain insurers, especially those preferring high-quality tranches (Display). If that approach is adopted, we would expect marginal net-positive impacts to RBC for AA and most A rated tranches, because their low expected losses would likely lead to NAIC ratings upgrades. Some BBB and BB rated tranches would face rating downgrades of an uncertain magnitude. Equity holdings would face steep risk-factor increases if the NAIC adopts the new 6.A, 6.B and 6.C categories.

Insurers are Large Holders of Investment-Grade CLOs

Comparison of Outstanding CLO Amounts and Insurance Ownership

Current analysis does not guarantee future results.

As of August 15, 2022

Source: Bank of America, Citigroup, NAIC and AB

2) Changes to Expected Loss Thresholds and Effect on RMBS and CMBS Ratings

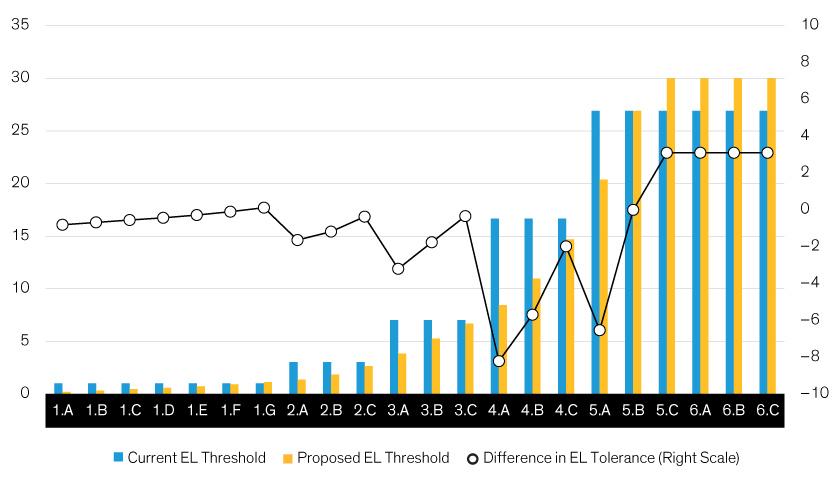

Expanded NAIC categories and factors were adopted in 2021, and there’s a belief that technical updates are needed to reflect consistent references to the “NAIC designation category” and the additional price points needed to determine categories. This revision would create more granular expected loss (EL) thresholds, which should translate into more granular NAIC rating categories for insurers’ holdings of commercial mortgage-backed securities (CMBS) and residential mortgage-backed securities (RMBS).

Our Assessment: This revision could happen quickly. However, it might be timed to roll out in conjunction with a potential increase in the number of macroeconomic scenarios used in CMBS and RMBS modeling, which we’ll examine in the next section. Expanded ratings tiers would likely increase the capital requirement for eligible CMBS and RMBS mezzanine tranches with weaker credit enhancements (Display).

Changes to Expected Loss Threshold Could Hurt Mezzanine Tranches

Current and Proposed Expected Loss (EL) Thresholds by Category (Percent)

Current analysis does not guarantee future results.

As of August 15, 2022

Source: NAIC and AB

For example, an eligible CMBS with an NAIC expected loss of US$1 per US$100 of par value would be designated NAIC category 1.G assets by the end of this year instead of its current 1.A. We believe that mezzanine tranches of CMBS and RMBS, as well as on-the-run (2020–2021 vintage), last-cash-flow and M1 tranches of credit risk–transfer securities (CRT), would be most vulnerable to the revisions. This is especially true in light of the possible expansion of macroeconomic modeling scenarios.

3) More Granular Macro Scenarios for CMBS and RMBS Modeling

The NAIC is considering increasing the number of macroeconomic scenarios used to model CMBS and RMBS from the current four: Optimistic, Base, Conservative and Stress. The proposal would double the number of scenarios, essentially inserting a new scenario—including an extreme tail case—between each of the existing scenarios to make scenarios more granular.

A quick analysis illustrates that the probability-weighted average of the indices used in scenario analysis would likely decline versus year-end 2021 across the three-, five- and 10-year horizons (Display). In the case of the Home Price Index (HPI), rather than gaining 1.8% in the three-year scenario, the HPI would increase by only 0.9%; over a five-year horizon, the gain would drop from 1.6% to 0.3%. These adjustments could negatively impact modeled RMBS.

Our Assessment: This change could also happen rapidly, though it might be linked with the update to CMBS and RMBS expected loss thresholds. A more granular set of macro scenarios could make mezzanine tranches of CMBS and RMBS more vulnerable to NAIC downgrade and could lead to a higher risk factor. The NAIC’s stated intent is to reduce tail probabilities and increase probabilities near the middle of the outcome distribution but, as noted, the change could push probability-weighted price indices used in modeling to lower levels.

Estimating the Impact to Property Valuations

Percent Gain/Loss of Modeling Index Under 2021 Tear-End and Proposed 2022 Guidance (Percent)

Current analysis does not guarantee future results.

As of August 15, 2022

NPI indicates the NCREIG Property Index, a national measure of property-level returns on real estate assets used in CMBS scenatios. HPI represents the Case-Shiller Home Price Index, a measure of home prices used in RMBS scenarios.

Source: NAIC and AB

4) Impact of Revised Bond Definitions on Private/Esoteric ABS

The NAIC intends to establish principles-based guidance for determining whether or not a security should be categorized as a bond. The intent is to address the increasing financial innovation by providing regulators and other financial statement users with more transparency on the risks in an insurer’s investment portfolio. A bond would be defined as any security that represents a creditor relationship with a fixed schedule for at least one future payment, and which qualifies as either an issuer credit obligation or an asset-backed security (ABS).

Our Assessment: This change would likely be gradual; the current target for implementing it is year-end 2024 or year-end 2025. However, we expect increased focus from regulators, industry participants and the media. According to the draft document released in June, securities backed by financial assets (CMBS, RMBS and CLOs) were specifically referred to as “Financial Asset-Backed” ABS. For these instruments, the NAIC bond definition is based on whether a security has a “substantive credit enhancement.” Securities that don’t meet the criteria would be treated as equities, not bonds. Overcollateralization and subordination both count as enhancements, but the NAIC hasn’t yet determined the threshold for enhancements to be considered “substantive.”

As for instruments not backed by financial assets, the proposal mostly targets private and esoteric ABS and, in our view, certain credit tenant lease securities. Bond classification would require securities to satisfy a “meaningful cash flows” test, defined as bonds for which less than 50% of the contracted principal and interest payments rely on refinancing or a sale of the collateral assets.

A one-size-fits-all definition of “substantive credit enhancement” might create unintended consequences for financial asset-backed instruments. For example, prime-auto ABS have meaningfully less subordination than subprime auto ABS, yet both would be categorized the same way. The test could also spur questions about the accounting of instruments backed by assets other than financial, including CMBS and corporate bonds, which rely on refinancing at maturity.

The Big Picture: What Could the Changes Mean for Insurers’ Portfolios?

The NAIC’s recent focus on securitized assets illustrates its desire to proactively review and regulate risk in insurers’ securitized-asset holdings. If the changes are partly or fully implemented, they would likely result in a net increase in RBC C1 charges.

For example, US life insurers were well capitalized heading into 2022, with an industry average Company Action Level RBC Ratio of 443%. That ratio could fall by 10–20 percentage points from the change in CLO capital treatment alone, depending on the NAIC’s ultimate approach. That’s a substantial amount for an asset class that generally comprises about 3% of the average life insurer’s portfolio. We wouldn’t be surprised if some life insurers, especially those more sensitive to RBC constraints, reconsider allocations to lower-rated CLO tranches ahead of the implementation.

What can insurers do as the NAIC changes move from proposal to ultimate implementation?

•Monitor and assess the proposed changes, provide comments and actively participate in the industry’s discussion. The changes are still in flux, with much more information to be presented and debated before final rules are issued, and modifications can substantially alter the playing field.

•Emphasize cross-sector, capital-adjusted relative value when optimizing insurance portfolios. Insurers need to build or acquire tools and models that enable them to be nimble in reevaluating “what if” scenarios and in re-optimizing portfolios under alternative capital-rule outcomes.

•Re-evaluate portfolio design as C1 charges shift, weighing the trade-off between deploying RBC into assets versus channeling them to other parts of the business or the balance sheet. Opportunities in the reinsurance market might also be another tool for capital management.

Gary Zhu is Director of Insurance Portfolio Management and Head of Multi-Sector Insurance at AllianceBernstein (AB). Dmytro Mukhin is North America Senior Insurance Strategist for AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Authors

Gary Zhu

Dmytro Mukhin