Inigo Fraser Jenkins | Co-Head—Institutional SolutionsAlla Harmsworth | Co-Head—Institutional Solutions; Head—Alphalytics

Additional Contributors: Robertas Stancikas, Harjaspreet Mand and Maureen Hughes

Introduction

In this note, we explore four key issues that asset owners will need to face in 2023, rather than a typical list of forecasts for market outcomes in the year ahead. They relate to more strategic problems—but ones that asset owners will need to grapple with this year.

Any macro discussion can never stray too far from inflation. We won’t discuss forecasts directly as one of our themes—instead, we address inflation’s impact on asset allocations. The US breakeven inflation rate dropped abruptly in the latter part of 2022, as investors adjusted their expectations of how hawkish the Federal Reserve would be. Whatever inflation forecasts one may have had six months ago are presumably lower now, given the Fed’s commentary.

However, the Fed’s current actions impact inflation over the next one to two years, not the next decade, and we continue to believe that long-term equilibrium inflation will be higher, given that the post-pandemic era represents a new regime. Different long-term forces are at work on inflation—notably deglobalization, demographic changes and environmental, social and governance (ESG) considerations.1 It will take a lot of work from investors to adjust strategic asset allocation to a higher-inflation world.

In our view, the key allocation questions include the appropriate weight of private assets and the near-term outlook for risk assets, such as equities. We think the topic of liquidity will be much more prominent, and that changes in funding levels and inflation expectations will drive very large differences in risk attitudes among investors. Another relevant theme we won’t discuss here is the impact of geopolitical risk on allocations, since we’ve addressed it elsewhere. We’ll end this note with a comment on what we see as the diverging outlook for supply and demand for equities and bonds over the next five years.

Theme One: What weight to place on private vs. public assets?

There’s probably no question of strategic allocation that ranks higher on CIOs’ to-do list than public versus private asset allocations, specifically: Should allocations to private assets continue growing?

In our client conversations, we find very different views. We spoke recently at a Canadian pension plan conference, where 70% of those in the room said they intend to increase their private-asset exposure over the next year. In the UK and Holland, by contrast, some pension plans have been trying to offload private assets.

Based on the asset allocations of 10 of the 20 largest US state pension plans with published and updated asset-allocation data in 2023 shows that the average allocation to private equity exceeds the medium-term allocation target by more than 3% (Display 1).

Display 1: Pension Private Equity Allocations Are Above Target

US State Pension Fund Allocations to Private Equity versus Target

Historical analysis and current forecasts do not guarantee future results.

In all cases, current private-equity allocations were below the maximum allowed, so this does not imply a need to sell.

As of December 20, 2022

Source: Public Plans Database and AB

In previous research, we’ve detailed2 why the allocation to private assets should be higher than historical levels: 1) expected returns are lower on many assets compared to the average the past 40 years; 2) diversification is needed if bonds are not as effective in that role; 3) inflation protection is needed and; 4) there’s a dearth of young, high-growth companies launching initial public offerings.

All of those forces remain in place, but the case for private assets must be translated into a very different context today. In recent years, return expectations were very depressed and central banks were providing plenty of liquidity. Now, two specific headwinds are set against the positive case for private assets.

The first is the risk of a liquidity problem, which we’ll examine later in this note. The second is the “denominator effect” of the relative move in public and private asset valuations, given the abrupt market repricing of 2022. Public equity and debt markets have quickly reflected the changed monetary policy backdrop, but there hasn’t been an equivalent marking to market of most private segments.

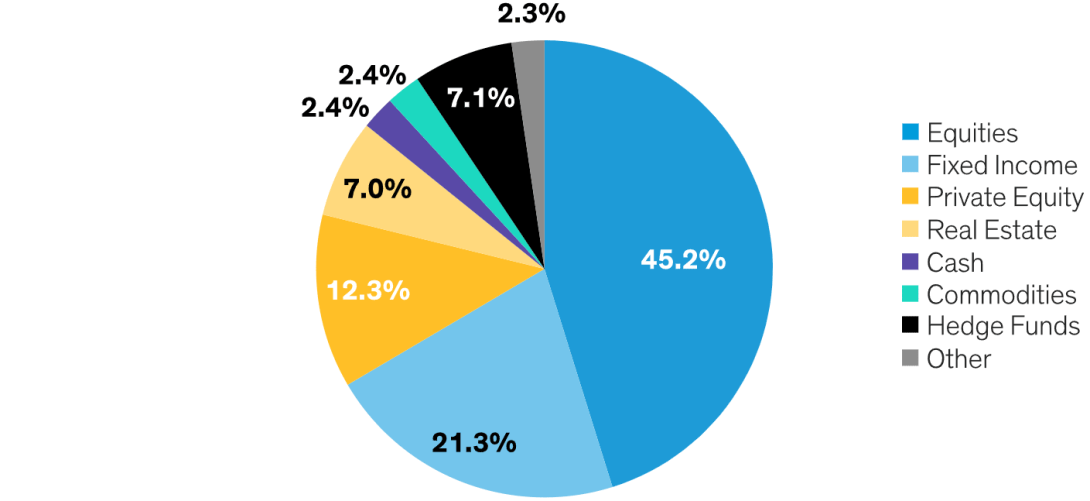

One could argue that if public market losses will be rapidly re-traced, no adjustment is necessary. But if the growth downturn is set to be more prolonged, a mark-to-market adjustment in private assets may be needed. Meanwhile, this situation has boosted portfolio allocations to private markets: the aggregate asset-allocation of US public pension plans, pro-rated for 2022 returns, suggests an overall 12.3% allocation to private equity (Display 2).

Display 2: Substantial Private Equity Allocation for US State and Local Pension Plans

Historical analysis and current forecasts do not guarantee future results.

Asset-allocation data for 2021 pro-rated with2022 returns. Equities: S&P 500 Index, fixed income: 10-year US government bond returns, real estate: US public REIT returns, Commodities: Bloomberg Commodities Index, hedge funds: asset-weighted HFRI index. For private equity, the latest available data is as of June 2022 for Cambridge Associates US Private Equity Index. Other assets represented by returns of Cliffwater Private Debt Direct Lending Index through September 2022.

As of December 31, 2022

Source: Bloomberg, Cambridge Associates, Cliffwater, HFRI, Public Plans Database, Thomson Reuters Datastream and AB

In theory, a year which sees a large move in marked assets shouldn’t immediately lead to a reassessment of strategic asset allocation—by its nature, it usually should not be at the mercy of short-term volatility. However, the recent experience of UK pension plans in the liability-driven-investing (LDI) crisis of 2022 and the awareness of liquidity needs make this more of a near-term concern.

In our view, this should be a long-term question and only addressed in a staggered way. However, if the current allocation appears overweight private assets compared with target allocations, it may raise questions about whether this should limit additional near-term allocations to private assets.

The bottom line is that despite the changes in the liquidity environment and starting valuations, we think a case for higher private asset allocations remains for many investors. That has become more finely balanced, though, so the pace of allocating to private markets in will slow in aggregate, and at the individual investor level will depend on liquidity needs.

There’s also a question of whether expectations for the average return on the average private equity investment have gone too far; we outline our forecast for private equity in the following section. We expect the net-of-fee return on the average private equity investment—one that assumes no alpha component—to be in line with returns for public equity. This suggests that marginal flows into private assets would head for other areas, and with inflation protection still a preeminent concern, we suggest that those areas will be private debt, private natural-resources assets, real estate and infrastructure.

Download Full White Paper