Benign Defaults to Buoy European High Yield

- As the European economy slides into a likely recession, investor concerns naturally turn to the consequent increase in corporate debt defaults. Indeed, some forecasts anticipate an uptick from their historically low levels—but corporate fundamentals start from a position of strength.

- Our second post in a series on the European high yield sector demonstrates that these concerns and forecasts require context regarding the macro backdrop and how these projections are constructed.

- Unlike many other forecasts, our scenario-based corporate default analysis combines a top-down macro/sector assessment with a bottom-up issuer analysis of the index that results in only a moderate increase in defaults.

- Furthermore, this year’s significant increase in yields provides more than adequate compensation for expected default losses.

Weathering the economic slowdown

At PGIM Fixed Income, we expect a Eurozone recession in the coming quarters, and we anticipate real GDP growth of 3.2% in 2022 will contract to -1.4% in 2023. Despite this projection, as we show in the subsequent sections, we expect high-yield default rates to only rise moderately. Importantly, at current spread levels, European high yield more than compensates investors for the anticipated default losses.

Given the weakening economic backdrop, many credit analysts expect corporate high-yield default rates will slightly rise from their historically low levels (Figure 1). For example, European default rates averaged 2.9% between 2010 through 2021 (inclusive), compared to 3.6% in U.S. high-yield bonds over the same period, according to Moody’s Investors Service.

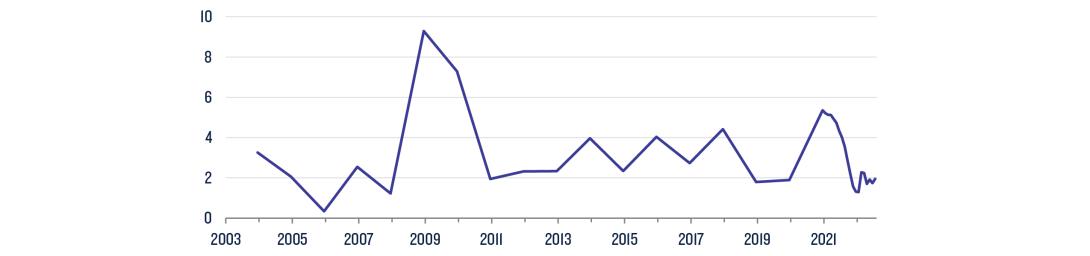

Moving to the more volatile period in 2022, European default rates remain contained, with the latest 12-month trailing default rate at 2.1% (Figure 2). Yet, nearly all of this year’s defaults are Russian or Ukrainian issuers as the Western European-only universe has recorded default rates of only 0.4%.

Figure 1: When looking to 2023, Moody’s anticipates a default rate of 3.2%, while Fitch Ratings expects a 2.5% rate (%)

Source: PGIM Fixed Income, Fitch (June 2022), Moody’s Investor Service (July 2022), Deutsche Bank (June 2022), Credit Suisse (June 2022), JPMorgan (June 2022).

Figure 2: Historical European High Yield Rolling 12 Month Default Rate (%)

Source: Moody’s as of August 2022.

Some of the more pessimistic scenarios with stickier inflation and a deeper recession estimate a default rate of up to 4.0% in 2023, which is still well below the 8.3% average during the Global Financial Crisis of 2008-09. We provide context to our scenario-based forecasts in a subsequent section.

Drivers behind a decade of low defaults

The preceding forecasts also warrant perspective as they are constructed on a on a top-down basis, which applies default rates from previous cycles to individual credit rating categories (i.e., BB, B, and CCC). Hence, we look at some historical drivers of credit performance in prior cycles and how they have evolved through this year.

Quantitative easing since 2015 has kept default rates low by lowering borrowing costs (which boosted cash flows) and supporting valuations (which kept loan-to-value ratios under control). In addition, European high-yield bonds have benefited from a robust profit backdrop. Furthermore, recent defaults don’t typically mean that bond issuers run out of liquidity or fail to pay. Instead, defaults are mostly restructurings that involve investors accepting a partial “haircut” on the debt and/or swapping debt for equity.

In addition, the ratings quality of the European high-yield index has improved in recent years: 69% of the market is now rated BB, versus 59% in 2010, and 5.1% is rated CCC, versus 12.0% in 2010. That improved quality supports the expectation of lower default rates in the future. Even during the pandemic, defaults remained limited: governments cushioned the shock with widespread fiscal support and capital markets helped issuers with liquidity needs.

PGIM Fixed Income’s bottom-up default analysis

While the prior forecasts may indicate the direction of travel for default rates as the cycle evolves, they provide little information about the prospects of individual issuers or the health of their balance sheets. Our credit analysts use their company-specific knowledge of European high-yield issuers to supplement top-down default estimates with bottom-up analysis. We recently conducted this analysis under three macroeconomic scenarios: moderation, recession, and stagflation, and in doing so, we identified four key drivers of our outlook for defaults.

- As mentioned, top-down models apply historical default rates to individual credit rating categories, which overlooks issuers current, historically strong balance sheets.

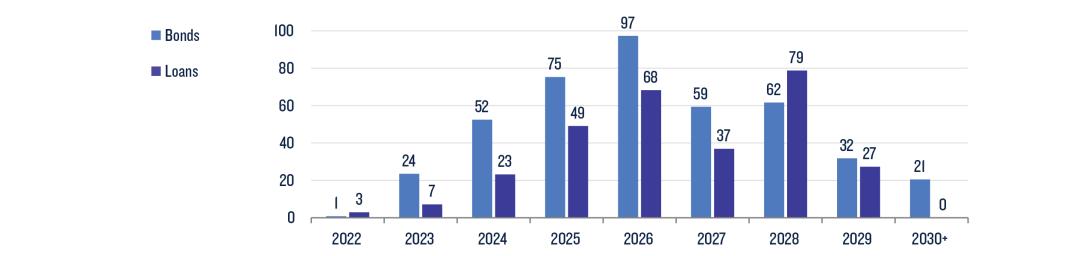

- Most top-down models don’t incorporate the fact that many firms have no debt maturities due for several years (Figure 3).

- Similarly, most top-down models don’t incorporate current levels of inflation, which helps some companies—particularly those with pricing power—by reducing the real liability of their nominal debt stock.

- Finally, top-down models don’t count equity support. If shareholders perceive that there is equity value in a business, they may support it with an equity injection instead of negotiating with debt holders.

Figure 3: The moderate maturity profile of upcoming high-yield bond repayments ($)

Source: J.P. Morgan as of July 2022.

Details of our three macroeconomic scenarios and conclusions are as follows:

SCENARIO 1. “MODERATION”

Inflation moderates towards pre-pandemic levels. Economic growth stabilises around 1%-2%. Issuers’ profits continue to grow, and yields fall from current levels.

- In this scenario, defaults continue to remain benign in 2023-24.

- High yield returns would be significantly positive with minimal default losses, high coupon receipts, and capital gains.

SCENARIO 2. “RECESSION”

Inflation falls back to trend or below, but the Eurozone economy shrinks in a mild recession. Issuers’ revenues suffer, but central banks moderate their policy tightening.

- In this scenario, default rates rise in 2023 and peak around 2% in mid-2024. Defaults occur mainly among real estate, financial, travel/transport, and food businesses.

- Returns remain positive on a two-year basis given the support from limited default losses.

SCENARIO 3. “STAGFLATION”

Inflation remains high and economic growth slows or turns negative, possibly due to a sudden stop of energy supplies. Issuers’ revenues struggle, and central banks keep interest rates high to subdue inflation.

- In this scenario, default rates rise from 2023 and peak around 3% in 2025-26. In addition to the above sectors, defaults increase in the retail and industrial sectors.

- Returns remain positive on a medium-term basis, supported by moderate default losses. A more attractive entry point relative to current levels materialises over a longer timeframe.

The capability of credit selection to lower defaults, raise returns

With the intent of keeping defaults below market levels and enhancing returns, our active management process starts with bottom-up credit views. In the economic downturn that is approaching, we see vulnerability in cyclical and consumer discretionary sectors, such as certain retailer and leisure names. We believe opportunities in cyclical sectors lie at a different, earlier stage of the credit cycle. By contrast, telecoms firms, packaging producers, and utilities appear more insulated due to their pricing power.

Avoiding vulnerable issuers and overweighting issuers with pricing power can substantially increase returns. In addition, we carry higher cash levels at times or use hedges to keep risk at appropriate levels. It is also important to maintain liquidity as volatility presents attractive relative-value opportunities.

Conclusion: low defaults boost the outlook for high-yield bond returns

Our conclusion remains similar in all three cases with two broad expectations. First, we expect defaults to remain below external analysts’ top-down forecasts. Second, we expect defaults to stay in-line with historical averages. Even in our most severe downside scenario, we do not expect cumulative four-year defaults to exceed 12% (i.e., we expect them to remain below 3% per year, on average). These rates remain around historical averages, rather than the higher levels we saw during the Global Financial Crisis of 2008-09 or during the pandemic in 2020-21.

With these default expectations in mind, we think that current yield levels, especially in certain non-cyclical sectors, more than compensate investors for expected default losses on a medium-term basis.

Timing markets and entry points into specific asset classes, such as European high yield, is difficult. Yet, as a potential recession and further spread widening approaches, a peak level in credit spreads and all-in yields may lie in the near future.

This combination will present an attractive entry point for investors with longer time horizons.

Read More from PGIM Fixed Income

Source(s) of data (unless otherwise noted): PGIM Fixed Income as of 24 October 2022.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. Clients seeking information regarding their particular investment needs should contact their financial professional. These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors. All investments involve risk, including the possible loss of capital. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. No risk management technique can guarantee the mitigation or elimination of risk in any market environment. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. No liability whatsoever is accepted for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this report. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients or prospects. No determination has been made regarding the suitability of any securities, financial instruments or strategies for particular clients or prospects. For any securities or financial instruments mentioned herein, the recipient(s) of this report must make its own independent decisions.

Conflicts of Interest: PGIM Fixed Income and its affiliates may have investment advisory or other business relationships with the issuers of securities referenced herein. PGIM Fixed Income and its affiliates, officers, directors and employees may from time to time have long or short positions in and buy or sell securities or financial instruments referenced herein. PGIM Fixed Income and its affiliates may develop and publish research that is independent of, and different than, the recommendations contained herein. PGIM Fixed Income’s personnel other than the author(s), such as sales, marketing and trading personnel, may provide oral or written market commentary or ideas to PGIM Fixed Income’s clients or prospects or proprietary investment ideas that differ from the views expressed herein. Additional information regarding actual and potential conflicts of interest is available in Part 2A of PGIM Fixed Income’s Form ADV.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2022 PFI and its related entities.

2022-6203

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in