The Covid-19 pandemic has changed the world, making it harder and more complex for investors to navigate the likely conditions for the major asset classes. This has made the tenth edition of our award-winning five-year outlook even more eagerly anticipated than usual: these are not usual times.

Expected Returns 2021-2025: ‘Brave real world’ contains our investment outlook for developed world and emerging market equities, government and corporate bonds, listed real estate and commodities, along with cash. It also contains our economic predictions for the likely post-Covid-19 recovery, and five special topics on the biggest issues of our times, two of which directly relate to this pandemic.

We are particularly proud to present our predictions this year to assist investors in their asset allocation decisions, because let no one doubt, the world is facing its biggest crisis since the Second World War. When the global economy was first confronted with Covid-19, we experienced the most significant US GDP contraction since the third quarter of 1932, and the deepest global recession since the 1930s.

To overcome the crisis, we believe investors need more than ever to understand that ultra-low interest rates are a key feature of the current investment landscape. We foresee a protracted period of negative real interest rates, meaning their impact on the relationship between economic fundamentals and asset price performance, and the consequences for multi-asset allocation, will be critical. We are living in a time of radical transition, and volatility in markets will remain elevated.

Yet, there are signals to be found amid the static. Financial markets have been confronted by pandemics and prolonged episodes of negative real interest rates before. We believe risk taking will be rewarded in the next five years, especially as some traditional safe havens will eventually be deemed risky as well.

Brave real world

During the Great Depression, Aldous Huxley published his famous 1932 novel Brave New World. It is a depressing dystopian vision, but it does have some relevance when describing an unequal, technologically advanced, consumerist society, in which governments interfere in the private sector – even infringing on individual freedoms. For instance, would it have been possible a year ago to imagine being forced into ‘lockdown’ or ’quarantine‘? And therefore to be consuming more digital media than ever before?

And yet, it’s not a brave new world as it is unlikely that the post Covid-19 era will mark the beginnings of a completely new world. There is much talk about a ‘new normal’. This is no wonder, considering the great divide emerging in the global economy, which can be seen most clearly in the discrepancy in performance between the technology sector and the non-tech sector since the 23 March trough.

What this suggests is that the global economy’s sudden standstill in 2020 has created a structural break. In fact, this is an acceleration of a tectonic shift that was already in the making. It’s not a new normal, but the old normal amplified. What was bubbling under the surface in the old normal has gradually become more real and more urgent. The larger trends are still present: high non-financial corporate leverage, declining trend growth, ever widening wealth and inequality gaps and shrinking monetary and fiscal policy space. So, it’s not a brave new world that will emerge in the next five years; it is a brave real world.

It’s a brave real world because medical workers and researchers are engulfed in a frantic race to provide an effective vaccine for Covid-19 and reboot society. It’s a brave real world looking at the real possibilities for a sustainable, greener future, after the lockdowns made the world accidentally sustainable. It’s a brave real world because the digitization trend that has become the principal way of working and living, but the time will come to get real instead of virtual. It’s a brave real world for policymakers who have provided stimulus that massively outweighs that of the global financial crisis. And it’s a brave real world for asset allocators, as they need to reconsider the concept of safe haven assets.

Three economic scenarios

In our economic scenarios for the next five years, our four building blocks are: solving the health crisis, crisis relief, aggregate demand management, and addressing the policy failures along the way. How effectively these four building blocks are implemented in actual monetary and fiscal policy will also largely determine the type of economic recovery path for countries and regions, as well as the behavior of financial markets.

In our base case, ‘Credible fiscal financiers’, the post-pandemic recovery starts off lopsided as the existing divide opens further between tech-savvy sectors and those at the front end of lockdowns. Companies in the leisure and hospitality sectors recover incompletely, while in-service sectors catch up significantly after 2022 as Covid-19 vaccines deliver herd immunity. Growth increases to trend towards the end of our projection period, while inflation in developed markets increases to 3% in the US by 2025.

In our bull case, ‘A reboot for growth with echoes of the 1970s’, economic growth retains momentum after an initial rebound in 2021. The first phase, solving the health crisis, is more successful. A larger number of effective Covid-19 vaccines are brought into circulation in 2021, and a fiscal cliff is avoided with no significant delay between the expiry of liquidity provisions by governments, and the emergence of a self-sustaining recovery.

Our bear case, ‘The great Covid-19 stagnation’, sees the cracks in the global economy get wider. The pandemic can barely be brought under control, with setbacks in vaccine research owing to unexpected mutations of the virus. Distribution of an effective vaccine is thus delayed until 2022. Economic actors remain in crisis mode as the seesaw between lockdowns and reopenings tips towards lockdowns. The crisis-relief toolkit is exhausted and a fiscal cliff develops before a self-sustaining recovery can set in.

What does this mean for investors?

The defining feature of this investment environment is ultra-low nominal interest rates and significantly negative real interest rates for longer, as inflation in both our base case and bull case picks up. This echoes 1971-1977 when developed countries had a negative real cash return of on average -2.4%.3 But the echo will be faint: we have not penciled in an outright stagflation scenario.

In such an environment, investors must boldly reorient themselves regarding stores of wealth and hedging capabilities of traditional safe haven assets. The mild inflation overshoot caused by policy makers in our base case transforms the risk-free returns of cash and bonds increasingly into return-free risks. We expect a negative return on cash for Eurozone investors and negative returns for developed sovereign bonds.

So, the brave real world is a paradoxical one: there will be risky safe havens. We expect risk taking to be rewarded in the next five years, even as volatility levels remain elevated. The preoccupancy of financial markets will shift from central banks to governments. This will bring about higher levels of asset and foreign exchange volatility as politicians offer guidance and policy implementation that is less smooth compared to those from their central banking counterparts.

Predictions for the major asset classes

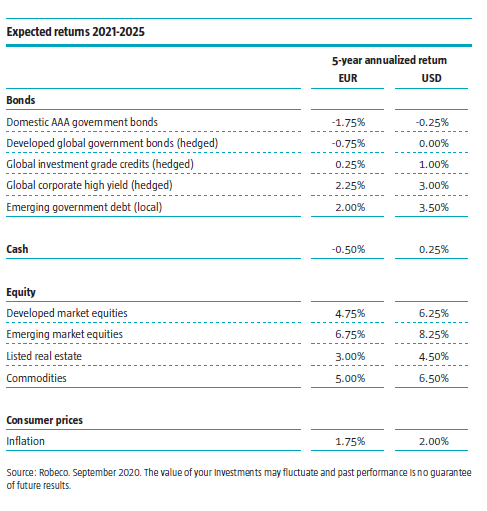

For the asset classes themselves, we think the best returns will be seen in emerging market equities, followed by commodities, developed market stocks and then listed real estate. We believe positive returns will also be found in higher risk emerging market debt and high yield corporate bonds (credits), with small positive returns still available in investment grade credits.

However, in line with our core thesis that the rates will stay lower for longer as central banks combat the pandemic, we foresee negative returns for AAA-rated super-safe government bonds and low-risk developed market sovereigns. Cash is also seen making negative returns in euro terms but positive returns in US dollar terms, due to policy difference between the Eurozone and US.

Five special topics

Our special topics this year cover a wide range of issues, two of which directly relate to the pandemic. In ‘Money for nothing, inflation not guaranteed’, we argue that the massive stimulus to restart economies following the Covid-19 crisis isn’t likely to trigger inflation. ‘Don’t be so negative about interest rates’ discusses three scenarios regarding the potential prevalence of negative interest rate policies over the coming years, including whether the pandemic means they are here to stay.

In ‘Factor investing – going beyond Fama and French’, we argue that there is more to factor investing than the standard academic factors, two of which – value and size – have performed badly over the past decade. This cannot be said of tech stocks, which continue to dominate stock market returns, as discussed in ‘Trends investing: finding the winners among skewed equity returns’.

Finally, we address the need to decarbonize portfolios in ‘Carbon pricing: asset allocation and climate goals’. This is proving to be a difficult but necessary task for investors in the drive to meet the Paris Agreement goals.

Important Information

Robeco Institutional Asset Management B.V. (Robeco B.V.) has a license as manager of Undertakings for Collective Investment in Transferable Securities (UCITS) and Alternative Investment Funds (AIFs) (“Fund(s)”) from The Netherlands Authority for the Financial Markets in Amsterdam. This document is solely intended for professional investors, defined as investors qualifying as professional clients, who have requested to be treated as professional clients or who are authorized to receive such information under any applicable laws. Robeco B.V and/or its related, affiliated and subsidiary companies, (“Robeco”), will not be liable for any damages arising out of the use of this document.

The contents of this document are based upon sources of information believed to be reliable and comes without warranties of any kind. Any opinions, estimates or forecasts may be changed at any time without prior notice and readers are expected to take that into consideration when deciding what weight to apply to the document’s contents. This document is intended to be provided to professional investors only for the purpose of imparting market information as interpreted by Robeco. It has not been prepared by Robeco as investment advice or investment research nor should it be interpreted as such and it does not constitute an investment recommendation to buy or sell certain securities or investment products and/or to adopt any investment strategy and/or legal, accounting or tax advice.

All rights relating to the information in this document are and will remain the property of Robeco. This material may not be copied or used with the public. No part of this document may be reproduced, or published in any form or by any means without Robeco’s prior written permission. Investment involves risks. Before investing, please note the initial capital is not guaranteed. This document is not directed to, nor intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, document, availability or use would be contrary to law or regulation or which would subject Robeco B.V. or its affiliates to any registration or licensing requirement within such jurisdiction.

This document may be distributed in the US by Robeco Institutional Asset Management US, Inc. (“Robeco US”), an investment adviser registered with the US Securities and Exchange Commission (SEC). Such registration should not be interpreted as an endorsement or approval of Robeco US by the SEC. Robeco B.V. is considered “participating affiliated” and some of their employees are “associated persons” of Robeco US as per relevant SEC no-action guidance. SEC regulations are applicable only to clients, prospects and investors of Robeco US. Robeco US is located at 230 Park Avenue, 33rd floor, New York, NY 10169.

© Q3/2020 Robeco