Central bank watcher: Running down that hill

The rise in long-term bond yields since the middle of the year has been fully reversed in the space of six weeks, as markets second-guess the ‘higher for longer’ message of DM central banks.

Summary

- The Fed is turning the corner

- While the ECB is experiencing a short plateau

- And for the BoJ, it’s about maintaining normalcy

This has been mainly driven by favorable developments on the inflation front – and less so by worries about a hard economic landing. The next leg of the bond rally, however, might well be spurred by negative growth surprises.

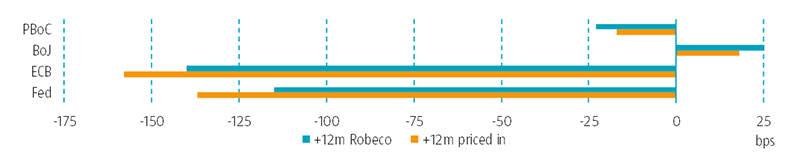

We agree with markets that policy rates won’t stay at a plateau for long, even though cuts in the US and the Eurozone might not come before Q2 next year, as the Fed and ECB fret about still too-high wage growth. We also think the longer these central banks keep rates into restrictive territory, the faster the journey back to neutral. For now, before central banks start running down the hill, we enjoy the view from the peak.

Central banks in Japan and China remain on their own course. The BoJ is still slowly running up that hill and set to end its negative rates policy by the end of Q1 2024. Meanwhile, the PBoC appears in no hurry to embrace the prospect of lower policy rates over the medium term, instead turning to balance sheet tools to stimulate the economy.

Figure 1 – Outlook for central banks policy rates

Source: Bloomberg, Robeco, change 12m ahead, based on money market futures and forwards; 19 December 2023

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in