China policy mix broadens to support private sector

China is pivoting policy back to supporting capital markets and the private sector as it seeks to strengthen its post-Covid economic recovery.

- Policies aim to de-risk economy by addressing property market and local government debt issues

- Pledge to ‘invigorate’ capital markets should help restore confidence

- Earnings need to turn higher to deliver real market momentum

We maintain our constructive view for Chinese equities despite tepid market performance in 2023 so far, as China policy makers aim to boost market confidence through more supportive policies focused on expanding domestic demand and addressing key risks.

Policy is turning more supportive in recognition that the transition to what China’s leadership has called ‘higher quality growth’ – with reduced reliance on construction and infrastructure spending – is in its infancy. External demand is also not offsetting tepid Chinese domestic demand with exports falling 14.5% year on year in July, reflecting weaker growth in inflation-hit Europe and the US.1 As a result, a new round of policy measures is expected in the second half of the year as the July Politburo meeting set a more pro-growth policy tone, with a focus on de-risking the economy and restoring confidence in the private sector.

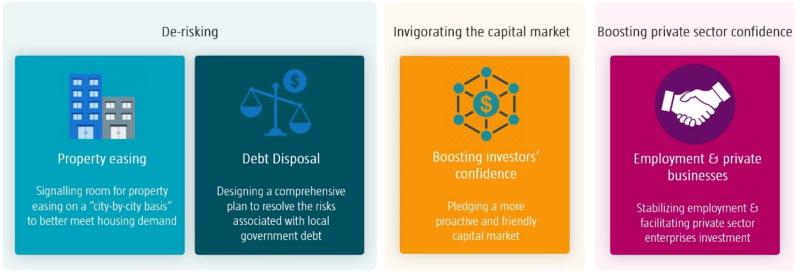

Figure 1: Politburo aims to de-risk and boost the private sector

Source: Robeco

De-risking the economy: Property market support ongoing

The tone regarding property policies has shifted, indicating a more relaxed stance and suggesting that further easing measures may be implemented. The politburo dropped the phrase “housing is for living not for speculation” and practically, local governments will get more flexibility to remove remaining restrictions on home purchases, and reduce down payment requirements for second mortgages. Banks will also be under pressure to enhance credit support for developers and consider reducing mortgage rates for existing mortgages.

Local government debt resolution key to future fiscal stimulus

The politburo meeting also emphasized the need to effectively address debt risks at the local government level, but details remain unconfirmed. Given the magnitude and complexity of China's local government debt and the potential moral hazard involved, a complete debt swap or bailout of local government financing vehicles (LGFVs) is unlikely in the near future. Instead, we anticipate measures such as debt extensions and de facto restructuring, particularly with banks, to be encouraged. Additionally, local governments may be urged to sell or mortgage assets to improve liquidity and to settle outstanding debts to the corporate sector which would help enhance corporate cash flow and confidence, but may require interim credit or fiscal support from the central government. Given any fiscal stimulus is likely to flow through local government, any definitive restructure of local government debt arrangements could be a precursor to more fiscal support for the economy, and thus is likely to be welcomed by equity markets.

Energizing capital markets

The commitment to rejuvenate capital markets and enhance investor confidence was very well received and media reports suggest securities brokers are being consulted on the potential policy mix.2 Policies under consideration include a stamp duty cut, which would reduce trading costs by RMB 22 billion for A-share investors for every 0.01 ppt cut, in 2022 terms. A reduction in IPO approvals to improve liquidity could also happen, with temporary pause to those from large-sized or nonprofitable companies. Changes to regulations to make equities trading more efficient are also likely, while caps on stock investments by pension, insurance companies, and foreign investors could be lifted.

Boosting private sector confidence

The politburo emphasized the importance of integrating employment stabilization into its overall strategy, in the light of concerns over rising unemployment among specific groups like young graduates, although specific measures have not been announced yet. As the private sector employs the majority of the labor force, policymakers also committed to introducing new policies that facilitate private-owned enterprise (POE) investment, indicating a supportive environment for entrepreneurial activities. The revival of IPO and M&A activities are keys to watch for.

Long-term investors should be re-assured

We welcome the renewed sense of urgency and purpose from the politburo meeting and expect detailed policy measures to flow in the second half. There are also solid reasons for optimism as China works to maintain its economic recovery, including substantial scope for monetary easing as inflation remains absent, and equity valuations remain attractive from a historical average point of view.

Domestic consumption remains a mixed picture with strong performance in services sectors like travel & hospitality where we remain overweight. We like the insurance sector which is benefiting from structural reform. We also like China’s technology names with AI exposure – a long-term theme that has room to run. Regulatory focus on China’s internet sector also appears to be complete, and we are positive as a result, given strong demand. China’s EV supply chain continues to boom with auto exports growing and we continue to favor long-term themes where we believe value lies, including the green economy, technology innovation, and the technological upgrade of China’s industrial base.

The earnings trend has remained subdued but an earnings revival would be a major catalyst for Chinese equity markets, and long-term investors should be in position before that happens to best take advantage.

1 Chinese exports suffer worst fall since start of pandemic – Financial Times – 8 August 2023

2 Rare China Vow on Market Support Puts Beijing’s Toolkit in Focus – Bloomberg – 7 August 2023

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in