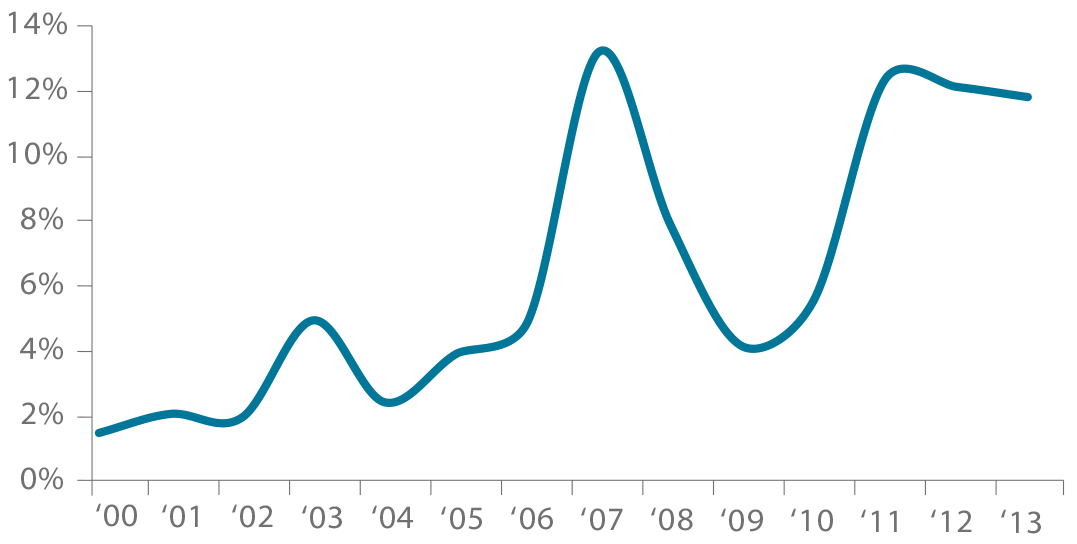

Co-investing is the practice of making non-control direct equity investments in individual transactions alongside general partners who source, or sponsor, the deal (“GPs” or “Sponsors”). Co-investing became institutionalized in the mid- to late 1990s as the overall private equity industry began to mature and has become a more prevalent allocation in investors’ portfolios. According to StepStone’s analysis, coinvestment dollars represented 13% of total equity invested in 2012, up from 1% in 2000 and on par with 2007, as shown in Figure 1.

FIGURE 1 | CO-INVESTMENT OFFERED AS % OF EQUITY INVESTED

Source: StepStone analysis.

Co-investments have clearly become more popular. However, researchers and limited partners (“LPs”) alike continue to question whether co-investments are a healthy choice or a guilty pleasure. Skeptics have several concerns, including (i) “adverse selection,” or the sense that GPs may not be showing their best deals to prospective co-investors; and (ii) limited evidence that co-investment programs (including funds) have matched the returns of buyout funds.

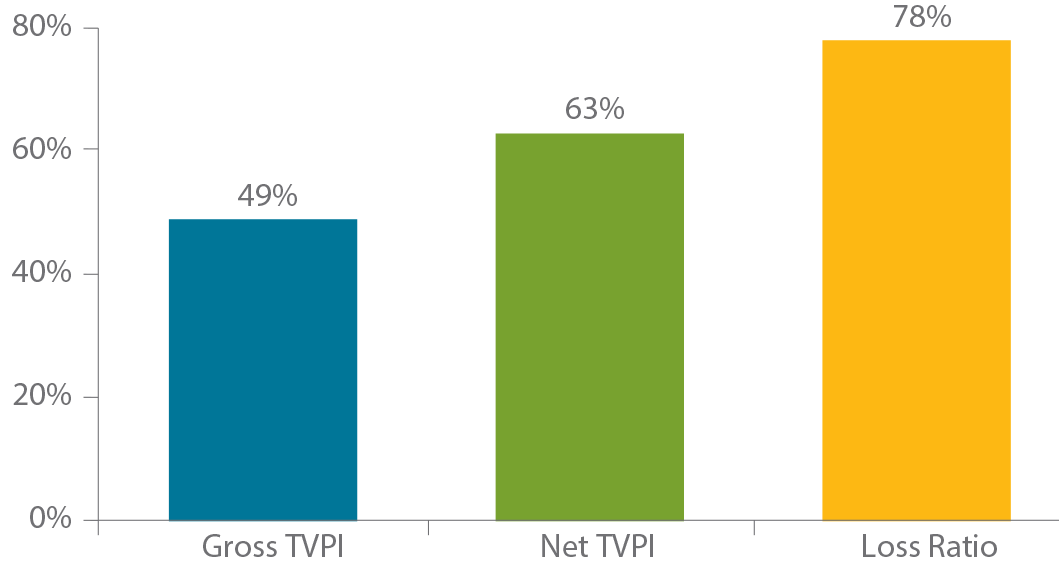

We conducted our own analysis of a dataset of 400 co-investment transactions completed by 97 GPs and found that co-investments have held attractive return potential, as shown in Figure 2. Specifically, co-investment deals generally performed in line with the funds that completed the deal (“Parent Funds”) on a gross basis, outperformed them on a net basis, and on average had lower risk profiles. However, our analysis also highlights several risks that LPs need to consider when incorporating co-investments into their broader private equity programs. StepStone believes that a broad sourcing network, understanding of GP incentives, and a rigorous due diligence process are critical for success in co-investing. With these caveats, we found that a well-constructed co-investment program has the potential to contribute to a healthy portfolio.

FIGURE 2 | PERCENTAGE OF CO-INVESTMENTS OUTPERFORMING PARENT FUNDS

As of 12/31/2013

Source: StepStone analysis.

Co-Investment Market Overview

From the mid-1990s until the late 2000s, market participants for co-investing generally included banks, which were investing off their balance sheets, insurance companies, funds-of-funds and high net worth individuals. Today, pension funds, insurance companies, sovereign wealth funds, family offices and consultants are driving growth in the co-investment market. Noticeably absent are banks, due to regulatory concerns, and hedge funds, due to liquidity limitations following the global financial crisis (“GFC”).

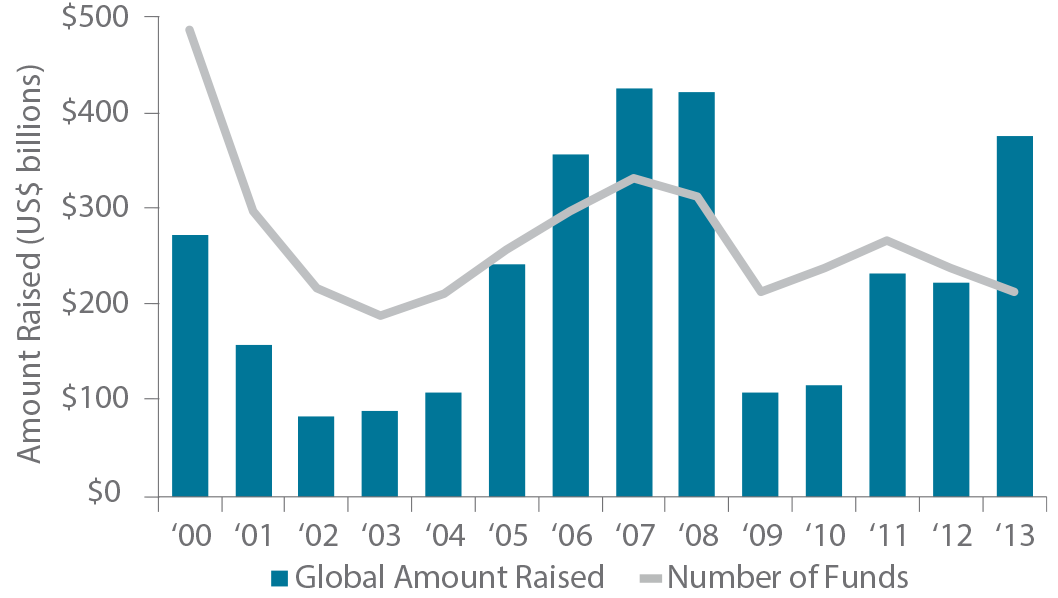

The growth in demand for co-investments post-GFC has been matched by a number of trends that have supported the supply of co-investment opportunities. In particular, global fundraising activity has declined significantly from the last market peak of 2006-2008, as shown in Figure 3. As a consequence, fund sizes have declined, and GPs have less equity to invest in individual transactions.

Concurrently, while Sponsors have been unwilling to assume equity syndication risk, traditional sources of capital from banks and hedge funds have declined. In addition, an industrywide aversion to “club deals” has discouraged partnerships with other private equity firms. In this environment, GPs are increasingly seeking co-investment capital, particularly with valuable LP relationships.

FIGURE 3 | HISTORICAL PRIVATE EQUITY FUNDRAISING

Source: StepStone analysis.

Co-Investment Rationale: LP Perspective

As the private equity industry has matured, LPs have grown in sophistication and are increasingly looking for new ways to gain exposure to the sub-asset class. LPs want better economic terms, greater control over portfolio management, including the pace of capital deployment, and deeper relationships with GPs. Ultimately, LPs consider these factors as ways to improve the return profile of their portfolios. Co-investments may help LPs achieve these objectives.

REDUCE FEE BURDEN

Co-investments have provided LPs with a cost-effective way to achieve private equity exposure. The extent to which LPs can experience lower fees can vary depending on what type of co-investor they are. Direct co-investors often invest pari passu on a “no fee and no carry” basis alongside Sponsors. While the absence of fees is an attractive feature, direct co-investing requires in-house staff or third-party resources to source and complete co-investment transactions, the cost of which can be prohibitive for all but the largest investors. Co-investment funds charge fees and carry to their investors, albeit they are generally less than half of the typical “2 and 20” fee structure of private equity funds. Separately managed co-investment accounts are a middle ground for investors that cannot rationalize building an in-house program but have sufficient allocation for co-investments.

INCREASE CONTROL OVER PORTFOLIO MANAGEMENT

In addition to being more cost-effective, co-investments have also provided LPs with a more nimble way to manage their portfolios. In particular, LPs have achieved attractive diversification benefits through co-investment programs, including co-investment funds, since they can access deals with managers of different sizes in various geographies and varied sector specializations. LPs have therefore enjoyed the benefit of diversification without sacrificing quality or having to pay two layers of fees, as required in fund-of-funds investing. In addition, co-investing has allowed LPs to deploy capital more rapidly than fund investing and towards geographies or sectors that they favor. As such, a co-investment program can be used to help implement tactical moves in a portfolio, by either scaling up exposure or scaling back exposure as desired by the LP.

DEEPEN GP RELATIONSHIPS

In addition to lower fees and greater control over portfolio management, co-investing has also allowed LPs to deepen their relationships with GPs. By working closely with the Sponsors during the due diligence process as well as during the holding period as the Sponsor implements value-creation initiatives, LPs have had the opportunity to develop insights into the strengths and weaknesses of GPs. As a result, the co-investor has had the ability to make more informed decisions about not only that specific GP, but also others, for future commitments.

Co-Investment Rationale: GP Perspective

From the GP’s perspective, the most obvious advantage to seeking co-investment capital from LPs has been the ability to access additional capital to complete a transaction. Maintaining control of the investment and staying within a fund’s diversification parameters are also important factors. Finally, GPs see co-investing as a good way to build stronger relationships with key investors.

ACCESS TO CAPITAL

Co-investing is an efficient way to participate in a deal which would otherwise be too big to undertake within the fund’s size parameters for each transaction. Prior to the GFC, GPs often co-invested with other GPs via “club deals,” a practice in which participants pool their capital in order to make the deal possible.

Following the GFC, however, co-investment dynamics changed. Club deals became unpopular and traditional sources of capital from banks and hedge funds dried up. At the same time, equity contributions in transactions became significantly larger, as shown in Figure 4, and smaller fund sizes forced buyout firms to invest fewer equity dollars per transaction. To bridge this gap, and as a way to reduce equity syndication risk, GPs have turned to co-investors to round out their equity checks.

While co-investment capital can reduce equity syndication risk, this is only a benefit if the Sponsor can still manage the transaction process to get to the closing table on time. Therefore, Sponsors favor those LPs who have a reputation of moving quickly and responding to them in a timely manner.

FIGURE 4 | AVERAGE EQUITY CONTRIBUTIONS TO BUYOUT DEALS

Source: S&P Capital IQ.

CONTROL AND GOVERNANCE

Sponsors’ experience with club deals was that governance can be challenging when other GPs are involved. Therefore, in the post-GFC era, GPs have preferred to maintain primary control of deals. Partnering with a valuable yet non-control investor allows the GP to retain greater control of an asset.

PORTFOLIO MANAGEMENT

Another motivation for GPs to offer co-investment opportunities is the need to address portfolio management issues. In many cases this will arise because the GP is buying a company where the total equity check will push them close to, or beyond, their fund’s diversification limits. However, GPs may also offer co-investment in average-sized deals when they are still fundraising and therefore unsure of the ultimate size of the fund. In addition, GPs may offer co-investment opportunities toward the end of the life of their funds when they have reduced capital availability but have yet to close on a new fund. As such, there are a number of portfolio and risk management considerations that can prompt GPs to offer co-investment opportunities in a range of deal sizes.

STRATEGIC PARTNERSHIP

Co-investment arrangements have allowed Sponsors to deepen relationships with existing LPs and to build relationships with potential investors. Co-investing provides Sponsors the opportunity to differentiate their capabilities first hand vis-àvis their competitors. Sponsors also benefit from having more sophisticated LPs as co-investors as they may bring a unique viewpoint, skill, network, or resource to the opportunity.

Read the full article here

This document is for information purposes only and has been compiled with publicly available information. StepStone makes no guarantees of the accuracy of the information provided. This information is for the use of StepStone’s clients and contacts only. This report is only provided for informational purposes. This report may include information that is based, in part or in full, on assumptions, models and/or other analysis (not all of which may be described herein). StepStone makes no representation or warranty as to the reasonableness of such assumptions, models or analysis or the conclusions drawn. Any opinions expressed herein are current opinions as of the date hereof and are subject to change at any time. StepStone is not intending to provide investment, tax or other advice to you or any other party, and no information in this document is to be relied upon for the purpose of making or communicating investments or other decisions. Neither the information nor any opinion expressed in this report constitutes a solicitation, an offer or a recommendation to buy, sell or dispose of any investment, to engage in any other transaction or to provide any investment advice or service.

Past performance is not a guarantee of future results. Actual results may vary.

Each of StepStone Group LP, StepStone Group Real Assets LP and StepStone Group Real Estate LP is an investment adviser registered with the Securities and Exchange Commission (“SEC”). StepStone Group Europe LLP is authorized and regulated by the Financial Conduct Authority, firm reference number 551580. Swiss Capital Invest Holding (Dublin) Ltd (“SCHIDL”) is an SEC Registered Investment Advisor and Swiss Capital Alternative Investments AG (“SCAI”) (together with SCHIDL, “SwissCap”) is registered as a Relying Advisor with the SEC. Such registrations do not imply a certain level of skill or training and no inference to the contrary should be made.

Manager references herein are for illustrative purposes only and do not constitute investment recommendations.