Credit outlook: ‘If I have to make a tackle, I’ve already made a mistake’

The Fed may have made a policy mistake by starting this tightening cycle too late. One of the key risks we face is higher-than-anticipated hikes in the coming months.

Speed read

- Fundamentals have deteriorated; the range of outcomes has broadened

- Valuations never stay at average levels, but they do reflect some risk now

- Technicals are weak since central banks need to correct quickly on inflation

Making an economic assessment had been difficult even before the escalation of the Russia-Ukraine crisis, given the distortion in many data series after two years of Covid. This was why we entitled our previous Credit Quarterly Outlook ‘Imperfect information and imperfect foresight’. “With the Ukrainian conflict, higher oil prices and further supply chain disruptions, it is clear that an even wider set of possibilities has to be assessed for fundamentals. If anything, downside risks to the economy have risen materially and recession risk is now openly debated,” says Victor Verberk, Co-head of the Robeco Credit team.

Regarding valuations, markets have cheapened up significantly since our Outlook in early December. The compensation for liquidity risk has risen a lot, as is also reflected by wider European swap spreads.

On technicals, our main worry is that developed market central banks are behind the curve. We think the Fed made a clear policy mistake by starting this tightening cycle too late. The key risks here are higher-than-anticipated hikes in the coming months, and inflation that not only lasts longer but peaks out at higher levels. This situation is akin to the Italian football player Paolo Maldini stating that when your defensive tactics don’t anticipate future risks ahead of time, you have to take an emergency measure (that is, tackle).

All in all, we are accepting betas that are a touch higher for investment grade credit. We do not mind if betas are just above one, while we remain in the first quartile of our risk budget. For high yield, the US market in particular has already started reflecting some optimism again, and trades too tight in our opinion. This means we like to stick to our underweight beta positioning overall, despite the fact that European high yield credit spreads have cheapened up in recent months.

A humanitarian disaster

“Let us first express our sympathy to all victims of the unjustified war in Ukraine,” says Verberk. “A humanitarian disaster is unfolding that far exceeds any relevance that our regular Credit Quarterly Outlook might have. This is our job, though, and we will therefore focus as usual on a cold financial assessment of the situation, in order to be positioned correctly on behalf of our clients.”

The European economy will be hit hard by this crisis. Europe faces supply chain issues and is of course highly dependent on energy from Russia, besides agricultural commodities from Ukraine.

The US economy, despite being less than two years into a recovery, is already in overheating territory. The labor market has largely healed and this part of the Fed’s job is done. Wage growth has started to broaden out. It seems that the key question for everyone in the policy and market community is the inflation trajectory.

A few words on China are warranted, too. “We have been worried about the sustainability of this debt-fueled economic growth ‘miracle’ for some time,” says Sander Bus, Co-head of the Robeco Credit team. “It is clear to us that this economic miracle has come to an end. More debt will not help in meeting the 5.5% growth target without simultaneously compromising Beijing’s macroprudential concerns. The demise of the real estate sector is a symptom of capital misallocation and of a system which is overleveraged. Because social stability remains the overarching objective for Beijing, stimulus will likely come in some shape or form.”

Inflation that is too high to ignore

So, what is the impact of the higher oil and gas prices? “As my colleague Martin van Vliet has highlighted, sharply higher oil prices can cost about 3% of GDP growth over a multi-year period,” says Jamie Stuttard, Robeco Credit Strategist. “So, the energy shock is clearly a tax on growth, besides its inflationary effects on headline inflation. This puts central banks in an awkward position. Inflation simply is too high to ignore and the Fed has to react, given their inflation mandate. Therefore, a quick series of rate hikes is likely to occur in a short period of time, with balance sheet tightening thrown in for good measure, potentially hurting economic growth.”

We are aware that both the rate cycle and the oil shock can trigger a recession. We think the likelihood is reasonably large, and it has certainly increased.

As US economists Larry Summers and Alex Domash pointed out, when inflation is above 4 or 5% and unemployment also below 5%, in a large majority of cases historically, the business cycle ends in a hard landing. Central banks will put on the brakes; they have few good choices.

Valuations have adjusted

We spent a lot of time digesting the relative value of current credit markets. In our analysis, the end of QE and the expectation of the start of QT in the coming months is now reflected in market prices and in credit spreads. We refer to this as the ‘2018’ scenario. But there are also a few scenarios that have not been priced yet.

First, 1970s-style inflationary and recessionary consequences from the current oil price shock might not materialize, but the comparability of the supply-driven oil shock currently unfolding makes us alert to the possibility of a bigger slowdown and spread reaction.

Second, we are not so certain that a Russian default, which would in nominal terms be one of the biggest in history, could be dismissed as being fully priced in risk premia.

Third, 5.5% economic growth in China looks increasingly unlikely to us. Given that China has provided over 50% of the marginal contribution to global GDP growth in the past decade, this scenario might also cause disappointment.

The conclusion for valuations is that spreads are around median levels again, which is wider than at any time in the past seven quarters. For this reason we no longer want to be short risk, although we need a bigger risk premium to take a long risk position. We focus on stock picking, sector choices and regional differences in the composition of spreads.

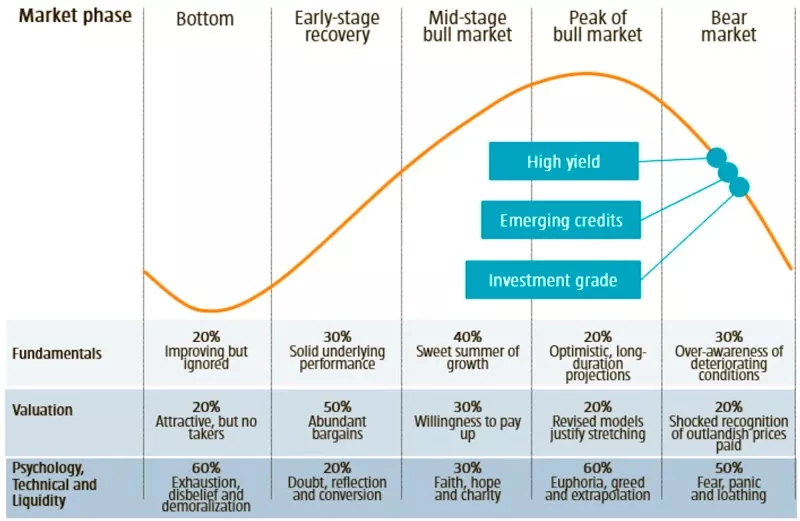

Market cycle | Mapping our view on market segments

Source: Robeco, March 2022

Watch the technicals

The technicals debate in our Quarterly Outlook session was one of the most interesting in years. We talked about the fear of much more front-loaded central bank action, the signals of an inverted curve and many geopolitical events.

Oil shocks tend to be met with a tighter central bank policy response, and oil shocks as well as sustained rate tightening cycles historically precede recessions. The risks to growth are especially acute when oil shocks are exogeneous supply-side events instead of demand-side shocks: the odds are not looking very good.

Further, since central banks have provided vast amounts of liquidity, one should not be surprised that the withdrawal of liquidity leads to more volatility. This is a very awkward time for central banks to be withdrawing liquidity, but inflation once again leaves them with little alternative.

Staying cautious

All in all, valuations suggest a somewhat more constructive stance to credit markets. However, as Maldini once said, “if you have to make a tackle, you have already made a mistake”. We still are a touch cautious in managing these allocations, since tail risks are around the corner and the full extent of the oil shock remains to be seen.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in