Credit outlook: Trade and trust

Valuations have cheapened but this has not been broad-based enough. More proof is needed that markets are pricing a full-blown recession.

Speed read

- At an inflection point around monetary, fiscal and geopolitical policies

- The credit and business cycles still need to unwind a bit further

- Central banks are driving markets like never before

We’re at an inflection point

The Robeco Multi-Asset team has just issued its latest 5-year Expected Returns publication, entitled ‘The Age of Confusion’. The report reflects on the many cyclical, secular and geopolitical inflection points we need to juggle as market participants. The Credit team agrees.

One example is the fact that global supply chains only work in peace time. ‘Eurussia’ no longer works, and ‘Chimerica’, the largest bilateral relationship in the world, needs watching carefully. The theory of trade expectations tells us that trade works if there is trust. We are now entering a phase of deglobalization or – as the Global Macro team prefers to phrase it – re-globalization along the lines of emerging military alliances.

These secular trends overlay cyclical trends in which central banks continue their own war: a war on inflation. “For now we take them at face value, and hence discount the dual mandates these might have, that inflicting pain on the economy is needed to bring inflation (expectations) back in line,” says Victor Verberk, Co-Head of the Robeco Credits team.

“This means more recession pain is to come in terms of earnings, investments, defaults in leveraged loans and market volatility in general. Valuations have cheapened but this has not been broad-based enough.”

We need more proof that a full-blown recession is priced. Technically, central banks will hike more and in many cases QT still has to start. All in all, we push out our forecast of the bottom of the cycle slightly, to later this year.

How far would central banks go?

The last decade or so policy makers have been horribly wrong in forecasting growth or inflation trends. We experienced a decade of almost no inflation and QE, which resulted in asset price inflation. We were then told that inflation was supposed to be transitory.

We have now entered a phase in which central banks worry about inflation becoming entrenched in the economy via wages and corporate pricing power. It tells you how inherently difficult inflation forecasting is, as well as the process of managing it. This means that policy mistakes have to be expected.

Central banks believe they have to inflict pain on the economy, on the demand side, to bring down inflation expectations. We have done some historical analysis to get guidance on what the nature of this pain could be and what we can learn about the timing and potentially the depth of the upcoming recession. Let us give a few of the many examples we looked at.

Seeking clues on where we are in the cycle

- First, history shows us that as the ISM falls from 60 to 50, spreads tend to widen. Only once recession is acknowledged, typically when ISMs and PMIs fall below the 47-48 region, is the downturn usually priced in. If the ISM or PMIs are good indications this time again, we are not there yet.

- Second, payrolls growth on average decelerates to under 200k at the end of the tightening cycle. The US economy is still way above that.

- Third, median financial conditions in recessions were historically much tighter than at present. The impact on rates, oil and equity has further to run on this metric.

- Fourth, sticky inflation like rents is still trending up. Also, the Atlanta Fed wage tracker does not show meaningful moderation yet.

Our overall conclusion is that, in terms of the economic cycle, we are not there yet by most metrics.

Then there is the market cycle. Historically, credit bear markets associated with recession last for at least 1.5 years. We have so far reached only nine months. Furthermore, the magnitude of the spread widening is typically at least 150 bps, while we’ve seen less than half of that move to date.

It is impossible to know precisely when we will reach the end of the tightening cycle.

“But we do know that interest rates historically peak before credit spreads. We also know that interest rates peak, on average, around the time of the second-to-last rate hike,” says Jamie Stuttard, Robeco Credit Strategist. “Based on this framework, our conclusion is that we might get there somewhere in November or December this year.”

We spent little time on China this quarter. It is evident that we should not expect the old locomotive of the global economy to do its job again this time. We seriously worry about growth expectations, debt levels and very high youth unemployment, for example. Economically restrictive Covid policies are also not helping.

We do not want to sound too bearish but at the same time we need to be somewhat more patient about entering the last phase of the credit cycle.

“There are a few positive tail risks that might change the base case,” says Verberk. “First, an unexpected end to the Ukrainian war or the recession itself might cause oil to drop a lot further. This would have benign implications for inflation and growth and might give the Fed a reason to pause. Second, maybe corporate pricing power will be better than expected, which in turn is good for corporate health. All considered, we do not think we have seen all phases of the bear market yet but we are slowly getting there.”

Valuations are becoming more attractive

On an optimistic note, the very painful positive correlation between credit, government bonds and equity so far in 2022 has led to much better valuations. A typical 60/40 balanced fund has lost 18% and bond markets have experienced the worst sell-off in total return terms for years. The flipside of the coin is that pricing has started to move towards more attractive levels.

We are very constructive on European swap spreads. Cross-sectional relative value shows that is the cheapest part of the market on a risk-adjusted basis compared to its own history. This is driven by Bund scarcity and very tight repo markets, which in turn is one of the many side effects of QE.

It means that European credit spreads have become cheaper than US credit spreads if the investor has government bonds as a reference benchmark. It has made high-quality investment grade credit like covered bonds or agencies very cheap. On an asset-swap-spread or spread-over-swaps metric, credit spreads do not look cheap yet. A reversal of Bund scarcity could be triggered by some kind of QT program by the ECB in the coming months.

For US high yield, the average option-adjusted spread has historically been 540 bps. We are close to that now, but recessions often see spreads twice that level. Current spreads do not reflect a premium for rising default rates or other unexpected risk premia. Still, as markets weaken, we are likely to enter the phase in which excess returns on a 12-month horizon become positive.

US investment grade spreads tend to widen to over 200 bps in a recession. We are not there yet, with current spreads around 150 bps. In Europe, spreads have widened a bit further due to the swap spread, but basically the risk premium for credit risk rather than liquidity risk is not there yet to justify a long beta position on an index basis.

We also looked at earnings and equity valuations as a reference. A few facts here. First, 50% of the NASDAQ constituents are down over 50%. Second, global fintech stocks on a price-to-sales ratio are arguably at oversold levels. Third, FAANG stocks (with real cash flow and business models) are down 30% to 70% from peak to current. Finally, European cyclicals/value stocks are at an all-time oversold level versus defensives. Clearly, long-duration assets got hammered and a recession has to a certain extent been priced in.

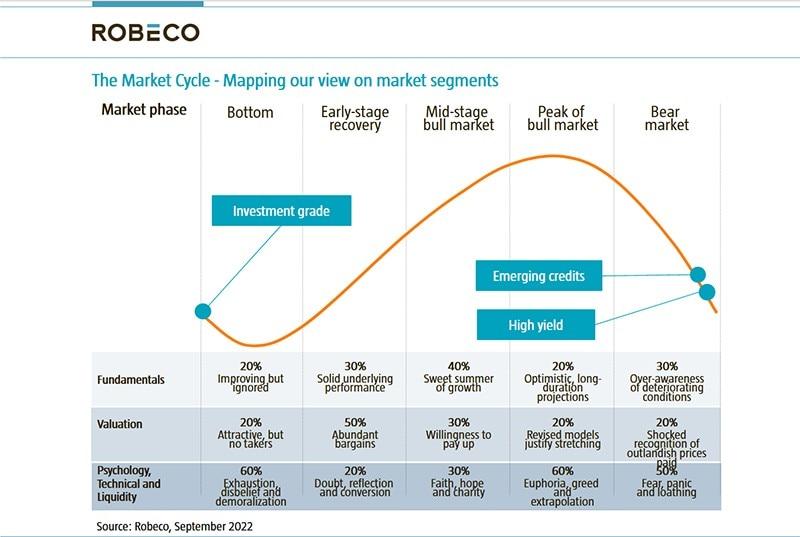

Figure 1: The market cycle

Mapping our view on market segments

Source: Robeco, September 2022

Don’t fight the Fed – or any central bank, for that matter

Central bank liquidity withdrawal is still the driving factor in markets. Equity and credit returns continue to correlate with the changes in the aggregate balance sheets of the world’s major central banks. A move from QE to QT means a lot of deflation in asset prices.

Given the very clear message from central banks that bringing inflation back in line remains their key priority, we do not expect a QE program any time soon to save the market. Instead, we should expect more volatility.

We are still a few months away from the second-to-last rate hike and even once rates have stabilized, history suggests we may first undergo a period of falling yields and rising spreads.

In an age of confusion, learn from history

The age of confusion has started. Inflection points in the business cycle, the monetary cycle as well as some secular cycles around demographics (are we headed for permanent labor shortages?) and geopolitics make the current period confusing to analyze.

Sander Bus, Co-Head of the Robeco Credits team, concludes: “For now, we believe that if history teaches us any lessons, it is that the business cycle has to unwind a little further, there is a risk that central banks will overreact and the market in general is not yet priced for a full-blown recession. We are aware of wider spreads, and in some pockets of the market we have started to buy, but a bit more patience is prudent before making a long beta call.”

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in