Cutting the Gordian EM Restructuring Knot

In recent years, investors have become accustomed to a significant impasse facing emerging market sovereign debt restructurings. China’s role as a major creditor owes to its Belt-and-Road initiative (BRI) and its inability, or unwillingness, to sign on to the traditional bilateral creditor coordination mechanism (i.e., the Paris Club) when its BRI lending went bad. February’s G20 meetings failed to breach the deadlock, and secondary market prices for sovereign debt of restructuring candidates continue to trade at deeply distressed levels.

Although the recent approval of Sri Lanka's long-delayed program with the International Monetary Fund (IMF) seemingly clears the way for future progress, we doubt that the treatment of Sri Lanka’s debt to China is repeatable. However, as with the mythological Gordian Knot, if there is a will, another resolution may exist under the IMF’s current policy mechanisms with modest changes to bond contracts. Our proposal not only addresses the current standstill, but it also improves participants’ incentive to maintain market access following a debt restructuring.

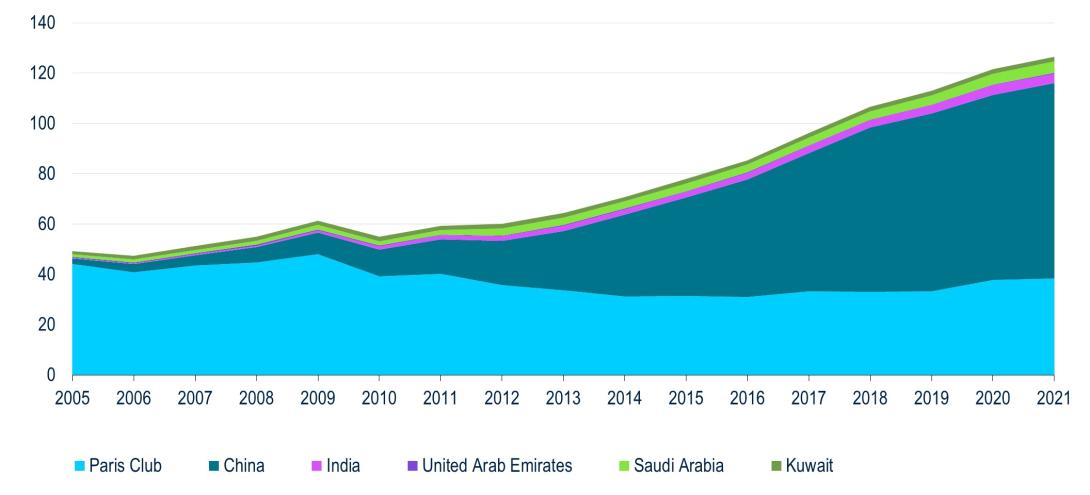

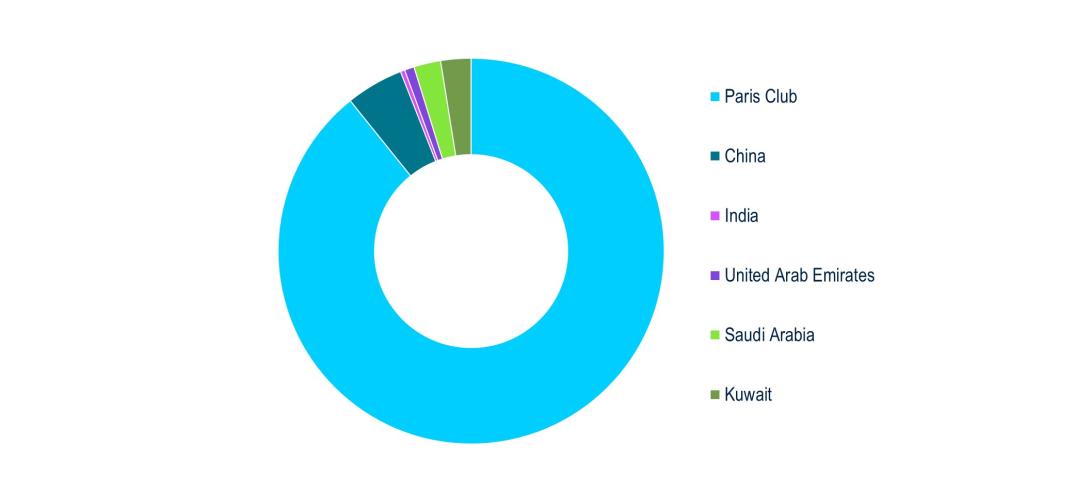

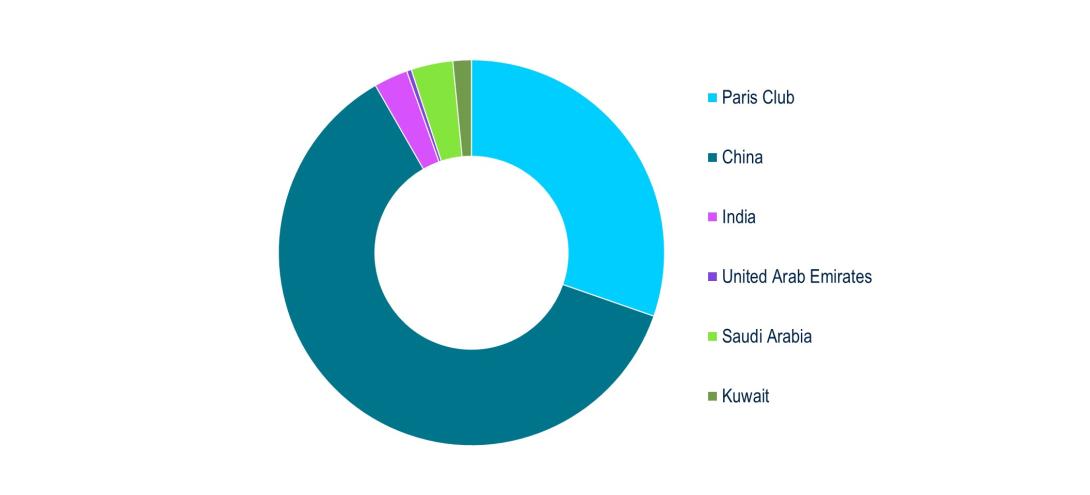

China is now the world’s largest bilateral creditor far, more than double the size of all Paris Club creditors combined (Figure 1). Moreover, most Chinese creditors to the affected countries are policy- or state-owned commercial banks, and, in contrast to otherwise universally accepted practice, the Chinese authorities do not consider them sovereign. Thus, they are not subject to Paris Club treatment. Moreover, during prior opaque restructurings in countries as wide ranging as Venezuela and Djibouti, China appears to have “cherry picked” and claimed collateral in the form of commodities and port infrastructure, a practice normally eschewed by bilateral sovereign creditors.

Figure 1: China Replaces the Western Bloc as Low-Income Countries' Main Creditor (Bilateral Loans Only)

Source: World Bank International Debt Statistics. Measures public and publicly guaranteed debt of Debt Service Suspension Initiative eligible countries to nations specified.

Past attempts to solve the problem have largely fallen flat. On the heels of the March 2020 Debt Service Suspension Initiative, which was limited to payment suspensions to bilateral creditors, the IMF, World Bank, and G20 countries developed the so-called “Common Framework in 2021.”1 While not initially singling out China, the framework prescribes an approach where up-front debt treatment by bilateral creditors is a condition for IMF programs. Furthermore, the subsequent negotiation of comparable terms with private creditors is a condition to further disbursements. Initial optimism regarding the framework has proved fleeting: bilateral debt relief for Zambia—where China co-chairs the bilateral creditor committee—has not even been agreed upon. The IMF program subsequently stalled after Board approval.

The “solution” adopted in Sri Lanka’s IMF program merits scepticism. Sri Lanka’s program languished since last summer’s agreement on polices as key bilateral creditors, including China, demurred from extending financing assurances, which are essentially regarded as a commitment to abide to Paris-Club terms and IMF debt-sustainability targets. Approval was finally unblocked by splitting China’s bilateral debt in two: claims by China ExIm Bank were deemed sovereign (and received the equivalent of financing assurances), while those of China Development Bank (CBD) were lumped together with commercial debt (restructuring of which is a requirement for the second IMF disbursement envisaged in six months). However, the arrangement may leave both sides unhappy. As in Zambia, ExIm Bank could still renege on commitments, while the significant progress reportedly made in the commercial creditor committee risks being undone once CDB’s requests are presented. Thus, a repeat of the Zambia situation is a high-probability, if not a central, scenario.

The situation need not be deadlocked—there are tools in place to move ahead. With this background, it appears the Common Framework can now be safely laid to rest, and the creditor split in Sri Lanka’s situation can remain an isolated case. Instead, we propose that the IMF use another existing tool, the so-called “Lending Into Arrears To Official Bilateral Creditors (LIOA)” policy, more aggressively.2 The origin of that policy is telling.

In 2013, Russia was the sole buyer of a bond issued by Ukraine in the waning days of the latter’s Yanukovych government in an effort to move lending to Ukraine outside the scope of a future sovereign debt treatment. On the heels of Russia’s invasion and annexation of Crimea in 2015, a restructuring on Ukrainian debt was needed, and Russia balked at accepting bilateral terms on its “Eurobond,” which in turn put financing for the IMF program in peril. As a result, the IMF adopted LIOA, the Russian claim was not serviced, and the IMF disbursed funds to Ukraine. Moreover, the Fund has used LIOA as a threat in other cases to get some smaller bilateral creditors to deliver financing assurances.

From perceived bad faith to hiding behind private-creditor status, the parallels to the current situation are obvious. The IMF Board could advance stalled programs under LIOA with the condition that debt service to China is halted until requisite and comparable debt treatment with the country is agreed upon.

Potential “hold-out” gains for China and others are a theoretical problem under our proposal. If all other creditors agree to debt restructurings and China does not, then China would still have all of its original claims intact after full upon completion of the IMF program. This would be an unpalatable situation to say the least, especially if the other creditors provided meaningful debt relief. Moreover, the problem may be large enough that other creditors could balk at initial restructurings.

However, while looming large in theory, this problem may not be insurmountable for a couple of reasons. First, we doubt that China would enjoy the reputational cost of being the sovereign holdout creditor who gets paid in full, a role that only so-called vulture funds embrace on the private side. Second, even if one were not to put much stake in reputational concerns, another work-around exists.

In new, post-restructuring debt and bond contracts, a modest tweak can redress the hold-out problem. Introducing a so-called “Most-Favored Creditor Clause” (MFC) into the newly restructured debt would embed a substantial disincentive against favorable holdout settlements. In basic terms, this clause would require each restructured debt to benefit from a more favorable restructuring in the future. In extremis, if a holdout creditor was subsequently made whole, that would also be the requirement for prior restructured bonds. Thus, if China or any other holdout were to follow this route, all other restructured claims would “snap back,” and the original non-sustainable debt situation would reappear, including the need for another IMF program with LIOA. This could provide a powerful incentive against holdouts of any type.

Implementing polices along the lines proposed also could provide a jolt to needed international coordination. Advancing rules-based debt restructuring is an international common good that does not align with pro- or anti-Western narratives. India’s role chairing the G20 is particularly propitious. It already blazed a trail for other “non-traditional creditors” by agreeing to provide financing assurances to Sri Lanka. During its G20 presidency, it could further leverage its leadership and rising power to constructively mediate and implement a workable debt-restructuring along the lines proposed above. In turn, the G7 countries would also need to stand ready to step up with any “back-fill financing” if Chinese financing going forward falls short, preferably via boosting IMF resources. The G7’s fledging Partnership for Global Infrastructure and Investment initiative designed to offer an alternative to BRI would be a natural starting point. Of course, actual country examples will provide their own idiosyncratic challenges, and, as in the past, they are best dealt within multilateral organizations that would also benefit from a common G20 vision.

Our market-based proposal appears more timely and easier to implement than other recently suggested alternatives. Other recent proposals have centered on creating large sweeteners to creditors from cleverly leveraged multinational balance sheets.3 Of course, these funds have yet to be raised, and tighter strings make it unlikely that they will be in time for Zambia and Sri Lanka. Though, in the end, such proposals may be the easiest way to prompt an overdue boost in IMF resources. In contrast, our proposal relies on already existing IMF policies that just need a simple IMF Board decision to be applied. While we propose a new element in bond contracts, the MFC is hardly new ground as the last decades brought the wide-spread adoption of collective action clauses (CACs). We don’t see a reason why MFCs should not be similarly easy to adopt as part of the exchange bonds offered in a restructuring.

Turning crisis into catharsis. Our proposal to quickly resolve the current deadlock in sovereign debt restructurings harkens to the Greek legend of cutting the intractable Gordian knot. But our proposal could also help overcome the chronic shortcomings of the past—repeated sovereign restructurings for the same country, e.g., in Argentina, Ecuador, and Zambia. Similar to MFCs, the introduction of covenants into sovereign bonds could help. Covenants feature prominently in corporate bonds (e.g., prescribing leverage ratios), but they find little equivalent in the sovereign universe.

A covenant that would accelerate a prior (restructured) bond if the sovereign contracted new, non-concessional debt would be a powerful disincentive against new borrowing, which has been a past culprit in subsequent restructuring needs. Covenants would be equivalent to similar conditionality in IMF programs, but binding even if there is no program. Complete bond acceleration may not be needed and a preferrable situation may be to allocate only two-thirds of new debt issuance to buying back prior restructured debt. This could offer a road into a new and so-far elusive finality in debt restructuring. Staying in Greek, more catharsis than crisis.

Read More from PGIM Fixed Income

3 See for example Setser et al’s proposal to leverage SDRs (https://www.ft.com/content/60a9e577-0bd3-4898-ac18-6ea9ff3573dd ) or Buchheit’s and Lerricks’ idea to leverage World Bank bons (https://www.ft.com/content/60a9e577-0bd3-4898-ac18-6ea9ff3573dd )

Source(s) of data (unless otherwise noted): PGIM Fixed Income as of April 2023

For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional.

These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy.

Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2023 PFI and its related entities.

2023-2687

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in