Do investors score with European soccer stocks?

As anticipation builds in Europe for the new soccer season, we delve into the risk and return dynamics of European soccer club stocks.

- European soccer club stocks exhibit high volatility but low correlation with market movements

- Despite occasional massive returns, European soccer stocks have, on average, underperformed

- Like lottery tickets, they have occasional high returns and overall negative long-term returns

Although the majority of European soccer clubs are privately held, enough are publicly listed to warrant in-depth exploration. These stocks might not be on every investor's radar, largely due to their low market capitalizations. This means their financial and economic impact is limited, which prevents their inclusion in mainstream stock indices.

However, their unique nature makes for an intriguing case study. For example, in October 2004, the stock price of Arsenal's "Invincibles" spiked by an impressive 67% after the team achieved an unbeaten streak of 49 games. Conversely, Juventus experienced a 45% drop in May 2006 following the revelation of the "Calciopoli scandal".

Generally, a club's revenue is heavily tied to their on-field performance, where the line between success and failure is often razor-thin. Unlike conventional firms, European soccer clubs tend to focus less on maximizing shareholder dividends, instead opting to reinvest earnings into their teams to enhance their potential for winning future matches and titles.

Data

Our aim was to identify the most significant European soccer stocks in terms of market capitalization, not only today, but also historically to avoid survivorship bias.1 Our sample consists of 26 soccer stocks from across a dozen European countries, typically competing in their respective local premier leagues. This includes well-known clubs such as Manchester United, Arsenal London, Borussia Dortmund, Juventus, Olympique Lyon, and Ajax. A comprehensive overview of the included soccer stocks is given below in Figure 1.

Figure 1: Sample of listed European soccer clubs

Source: Robeco, STOXX. The figure visualizes our sample of listed European soccer clubs: Aalborg, AFC Ajax, Aarhus, AIK Fotboll, Arsenal, AS Roma, Benfica, Besiktas, Borussia Dortmund, Brondby IF, Celtic, FC Porto, Fenerbahçe S.K., FK Teteks, Galatasaray, Juventus, Kopenhagen FC, Lazio Roma, Manchester United, Newcastle United, Olympique Lyon, Ruch Chorzow, Silkeborg IF, Sporting Lisbon, Tottenham Hotspur, Trabzonspor.

Our sample spans from January 1997 to March 2023, offering over a quarter-century's worth of data. We gathered return and market cap data for each individual stock and constructed a soccer index by determining the capitalization-weighted average return of the available stocks at each point in time.

Initially, our soccer stock count is a mere 6, but the index gradually diversifies. Until 2005, the index is significantly influenced by Manchester United, with an average weight exceeding 40%. After Manchester United's delisting in 2005, the index becomes more balanced, a trend that persists even after Manchester United is relisted in 2012.

Low risk or high risk?

Our first analysis focuses on the risk associated with soccer stocks. The two most important risk measures are volatility and beta. For most stocks, these risk measures align closely, i.e., low-volatility stocks also tend to be low-beta stocks, and high-volatility stocks also tend to be high-beta stocks.

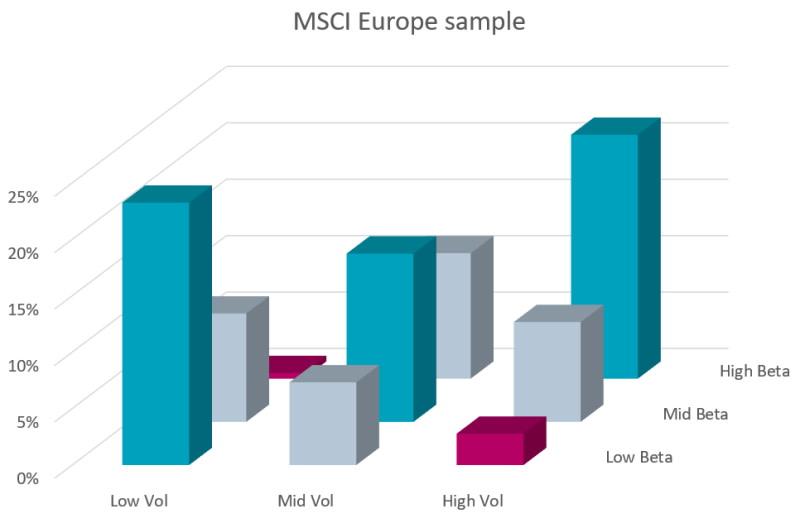

This relationship is illustrated in Figure 2, which classifies all MSCI Europe index constituents into three volatility buckets and three beta buckets independently.2 The graph demonstrates that most stocks fall along the diagonal from front left to rear right (blue bars), while stark differences between volatility and beta (red bars) tend to be quite rare.

Figure 2: Distribution of MSCI Europe constituents in volatility and beta groups

Source: Robeco, Refinitiv. The figure shows the distribution of MSCI Europe Index constituents in volatility and beta groups. To be included in the sample, we require at least five years of available return data. The sample period is January 1997 to March 2023.

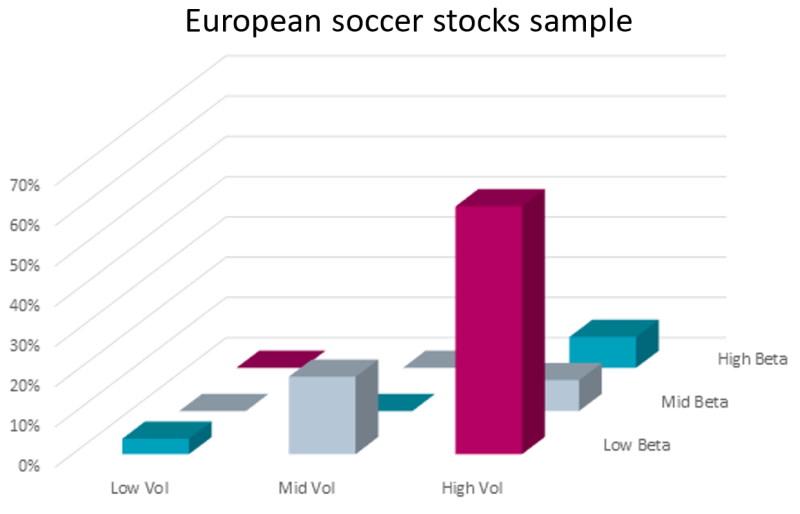

However, soccer stocks exhibit very different risk characteristics. As shown in Figure 3, most soccer stocks simultaneously display a high volatility and a low beta, a very unusual combination. The high volatility means that share prices fluctuate widely, but the low beta indicates minimal co-movement with the market. In simple terms, the prices of soccer stocks go all over the place, but in their own unique way. Depending on the definition of risk, this makes them both low-risk and high-risk stocks at the same time.

Figure 3: Distribution of European soccer stocks in volatility and beta groups

Source: Robeco, Refinitiv. The figure shows the distribution of Europe soccer stocks in volatility and beta groups. The soccer stocks are sorted into three volatility buckets and three beta buckets based on the same breakpoints as in Figure 2. The sample period is January 1997 to March 2023.

The return of soccer stocks

The return of the aggregate soccer index versus the MSCI Europe index by calendar year is shown in Figure 4. Return variations of 20 or 30% in a single year are no rarity, underlining the high volatility of soccer stocks. The low beta of soccer stocks is apparent in years like 2008 (global financial crisis) and 2022 (tech crash), when soccer stocks massively outperformed the market, demonstrating their rather uncorrelated behavior.

Unfortunately, large underperformances have been considerably more frequent (48% of the years) than large outperformances (just 30% of the years). Over the full sample, the return of the soccer index lagged the market by almost 6% per annum.

Figure 4: Calendar year return of European soccer clubs versus MSCI Europe

Source: Robeco, Refinitiv. The figure shows the return spread between European soccer stocks and the MSCI Europe Index. Portfolios are value-weighted and updated monthly. The constituents of the soccer portfolio are presented in Figure 1. The sample period is January 1997 to March 2023.

Source: Robeco, Refinitiv. The figure shows the return spread between European soccer stocks and the MSCI Europe Index. Portfolios are value-weighted and updated monthly. The constituents of the soccer portfolio are presented in Figure 1. The sample period is January 1997 to March 2023.

We have published extensively on the low-risk anomaly - the phenomenon that low-risk stocks deliver market-like (or superior) long-term returns with substantially lower risk, whereas high-risk stocks generate poor long-term returns despite their high risk.3 The same conclusion applies regardless of whether volatility or beta is used as a risk measure, which is unsurprising given their usual high correlation.4 However, soccer stocks, due to their contrasting volatility and beta characteristics, present a unique opportunity to assess which metric is a more important determinant of expected return.

To this end, we compare the long-term return of the soccer index with the returns of volatility- and beta-sorted portfolios in the MSCI Europe universe. We consider value-weighted tertile portfolios for volatility and beta estimated on daily data over a one-year lookback period. Figure 5 shows that the low-risk anomaly is clearly present among European stocks. In terms of long-term return, the low-volatility and low-beta portfolios come out on top, while the high-volatility and high-beta portfolios end up last. Although volatility seems slightly more potent than beta, the differences are small. This is consistent with the extensive literature on the low-risk anomaly.

Figure 5: Cumulative performance of European soccer, volatility, and beta portfolios

Source: Robeco, Refinitiv. The figure shows the cumulative excess return over the risk-free rate of European soccer stocks and stock tercile portfolios based on 260-day volatility and beta. Portfolios are value-weighted and updated monthly. The constituents of the soccer portfolio are presented in Figure 1. The investment universe of the tercile portfolios consists of the MSCI Europe Index constituents. The sample period is January 1997 to March 2023.

Turning to the portfolio of soccer stocks, we observe that they clearly have the worst performance of all. In fact, their long-term cumulative excess return has been negative, meaning that an investment in soccer stocks underperformed even risk-free cash holdings. Given their extensive short-term return fluctuations and disappointing long-term average return, soccer stocks bear more resemblance to high-risk stocks than low-risk stocks. Thus, the high volatility of soccer stocks appears to be a better indicator of these stocks' performance behavior than their low beta. So when volatility and beta conflict, the evidence from soccer stocks suggests that investors should let volatility prevail over beta.

Soccer stocks as lottery tickets

A common rationale for the low-risk anomaly is that speculative investors willingly overpay for risky stocks due to a preference for lottery-like properties, i.e., a chance to hit the jackpot.5 Our sample contains some striking examples of this. For instance, Borussia Dortmund returned 138% in the 2010-2011 season when they unexpectedly clinched the championship after a long dry spell, Celtic returned 159% in the 2006-2007 season when they secured the national title and made it past the group stages in the Champions League, and Fenerbahçe generated a whopping 190% return in the 2007-2008 season when they reached the quarter-finals of the Champions League.

However, much like lotteries yield more losers than winners, the occasional big payoffs of some soccer stocks go hand-in-hand with poor returns in many other periods. Thus, while soccer stocks might be great for a lucky few who happen to choose the right club at the right moment, most investors end up disappointed.

Of course, die-hard fans might derive a certain non-financial utility from investing a small part of their wealth in the clubs they passionately support. However, from a purely financial perspective, the analysis in this article demonstrates that, despite their seemingly attractive low-beta characteristics, soccer stocks are generally not a desirable long-term investment opportunity.

Footnotes

- We looked at the constituents of European soccer stock indices that used to be available in the past, which includes soccer stocks that have since been delisted.

- Although our sample contains a few stocks from emerging markets (Turkey, Poland) or even frontier markets (North Macedonia) we use the regular MSCI Europe index as a reference point.

- For an extensive overview we refer to Blitz, van Vliet, and Baltussen, 2020. “The Volatility Effected Revisited”, Journal of Portfolio Management, volume 64, issue 2, pages 45-63.

- We tend to find slightly stronger results for volatiltiy than for beta but the main conclusion is the same.

- See Barberis and Huang, 2008. “Stocks as Lotteries: The Implications of Probability Weighting for Security Prices”, American Economic Review, volume 98, issue 5, pages 2066-2100.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in