Emerging-Market Debt Outlook 2023: A Shifting Balance of Risks

Christian DiClementi | Lead Portfolio Manager—Emerging Market Debt Adriaan du Toit | Director—Emerging Market Economic Research; Senior Economist—Africa

Financial markets offered few opportunities for refuge in 2022, and emerging-market bonds were no exception. We expect the past year’s difficult conditions to gradually unwind in 2023, but risks remain, and investors will need to be selective.

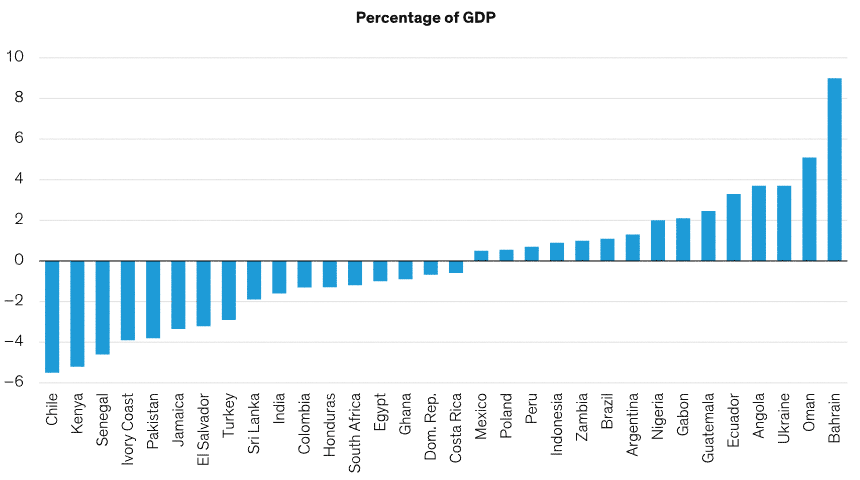

Global growth is expected to face stiff headwinds this year, which could pressure commodity prices. Higher commodity prices are generally positive for emerging markets, especially when the US dollar is weak. The cycle over the past two years has been somewhat unorthodox, with commodity prices rising sharply alongside a strong US dollar. This created tension between high- and low-quality credits, with lower-quality credits suffering the most. While commodity weakness would help contain global goods inflation and reduce the risk of soaring funding costs, it could also prove challenging for commodity-dependent countries with large external financing requirements—particularly those with negative basic balances (Display) and limited bond-market access.

Emerging Markets: External Dynamics Vary Widely

2023 Forecast Basic Balances (Current Account + Foreign Direct Investment)

Source: Haver Analytics and AllianceBernstein (AB)

A Potential End to Rate Hikes Despite Stubborn Inflation

If deteriorating economic conditions lead to a deep or prolonged cyclical trough, the global monetary policy cycle could pivot, although our baseline expectation is for a prolonged policy pause.

Emerging-market investors are already seeing light at the end of the policy-tightening tunnel. We believe that the tightening cycle is more than 80% complete, with growing evidence that core inflation is decelerating. This means one of the major macro-level headwinds for emerging markets—the tightening of global financial conditions—is abating.

Inflation has been anything but transitory, however, and despite evidence of disinflation, we don’t expect inflation to fall back to pre-pandemic levels in 2023. This could limit central bank maneuverability and might ultimately force central banks to accept higher inflation as a new normal.

China’s Pivot on Zero-COVID Could Bring a Note of Stability

One reason for lackluster emerging-market performance in 2022 was China’s economic underperformance, due in part to lockdowns aimed at staving off the spread of COVID-19 infections. While China’s decision to wind down its zero-COVID policy is encouraging, it isn’t likely to supercharge the growth outlook for emerging markets.

Still, this long-awaited economic reopening, coupled with China’s low commodity inventories, could help stabilize commodity prices and emerging markets as a whole. At the very least, it will remove one of the major obstacles to emerging-market asset prices.

Pockets of Distress Remain, Though Defaults Have Likely Peaked

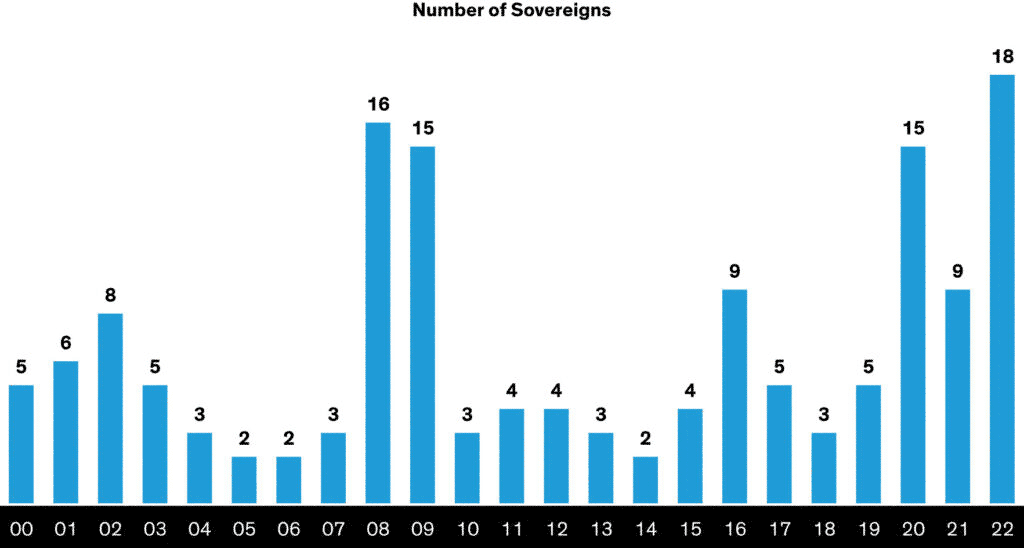

While we could see an end to rate hikes in early 2023, policymakers aren’t likely to cut rates as quickly as they’ve been able to in previous cycles. The policy pivot might come too late, or the macro downdraft might be too forceful, to avoid distress in the frontier space of emerging markets, where credit stress is high (Display).

Sovereign Credit Stress Is Elevated

Sovereigns with Spreads >1,000 Basis Points

Source: Goldman Sachs Investment Research and AB

But in our view, the worst of the sovereign default and restructuring cycle is behind us, and we don’t believe default rates currently priced into emerging-market assets will be realized in 2023. As a result, we expect sovereign distress to be increasingly credit specific and less cyclical in nature. For investors, this means careful issuer selection will be key—particularly among lower-quality segments.

We’re also keeping an eye on the more cyclical part of the market—specifically, local rates and currency. We believe the global economy is approaching an inflection point as both inflation and growth slow. This could open the door for select opportunities in undervalued emerging-market currencies or domestic rate markets.

Emerging Opportunities Despite Cyclical Risks

As we transition into 2023, we expect the correlation between duration and risk assets to turn negative again, which should improve the return potential of emerging-market debt. Still, investors should be realistic about fundamental challenges that could dilute a potential rebound of emerging markets, including lower long-term growth potential, higher debt burdens and continued geopolitical tensions.

Valuations remain a mixed bag, and investors should be cautious when assessing value through a traditional lens. Valuations have moved the most in distressed market segments, and less so among sovereigns with stronger fundamentals.

As the balance of risk continues to shift, we see select opportunities in three market segments:

- Lower-quality corporate and sovereign credit that is best positioned to weather a downside surprise to global growth—and where the probability of default is overpriced

- Local-currency sovereign debt where mature interest rate hiking cycles and disinflation could support bond prices

- Undervalued currencies in emerging markets where monetary policy has already been tightened and that may benefit from a weaker US dollar

We believe the stage has been set for a more constructive environment for emerging markets to start the year. As the balance of risks shifts in 2023, we see the potential for active investors to enhance returns through thoughtful country, sector and security selection.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in