The COVID-19 crisis has accelerated the end of the credit cycle, setting up a wave of downgraded fallen angels. For insurers, navigating this landscape requires adaptability, because with strong credit research, fallen angels can mean rising valuation opportunities.

Download PDF

Insurance investors always keep a careful watch on the credit cycle. Among the biggest holders of investment-grade credit in the world, insurers understand that the later stages of the cycle bring the potential for an increase in fallen angels—corporate bond issuers downgraded from investment-grade to high-yield status.

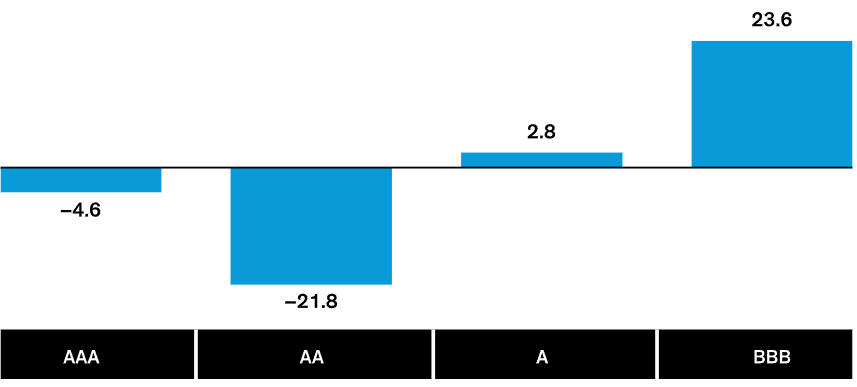

The concern has intensified over the past decade, as the ranks of BBB-rated issuers—the lowest rung of investment grade—have swelled. Since 2008, their share in the Bloomberg Barclays Global Corporate Bond Index has risen by 24% (Display 1). With so many issuers perched on the lowest ledge of investment-grade status, the concern about a wave of fallen angels is understandable.

Display 1: Growth of BBB Issuers Has Raised Alarms of a Fallen-Angel Surge

Change in Market Value Weight of Ratings Since 2008 (Percent)

Analysis provided for illustrative purposes only and is subject to revision.

As of March 31, 2020

Global corporates represented by Bloomberg Barclays Global Corporate Bond (USD Unhedged)

Source: Bloomberg, Moody’s and AB

The COVID-19 Pandemic and the End of the Credit Cycle

Entering 2020, the credit cycle was largely maturing at a measured pace, and the fallen-angel migration seemed manageable. But the situation deteriorated in late February and March, when the global spread of the coronavirus (officially COVID-19) forced widespread social-distancing mandates and business shutdowns. Essentially, efforts to flatten the COVID-19 curve also flattened the global economy. Oil prices, already under pressure from the sudden collapse in global demand, spiraled further downward as a price war erupted. The conflict’s trigger was a collapse in production-cut discussions between Saudi Arabia and Russia, which led to a breakup of OPEC+, a broad coalition of OPEC members and other large oil-producing countries, including Mexico and Russia. Together, the shutdown of most of the world economy and a shocking plummet in oil prices took a heavy toll on corporate earnings and ratcheted up the pressure on bond issuers, accelerating the end of the credit cycle.

Dimensioning the Coming Fallen-Angel Wave

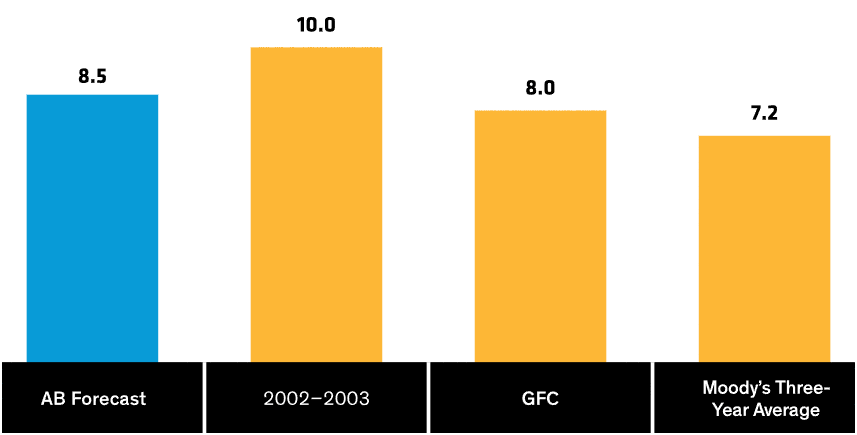

To understand the expected size and scope of the fallen-angel migration from the US investment-grade corporate market, we reassessed credit fundamentals with an in-depth review of all issuers we cover. Based on those results, we updated our internal credit ratings (distinct from credit agency ratings). Our analysis suggests that about 8.5% of investment-grade corporate bond issuers will see their financial condition decline to levels that indicate high-yield status over the next three years. We didn’t attempt to predict when—or if—credit-rating agencies will officially downgrade these issuers. Historically speaking, this percentage is similar to the 2002–2003 recession (10% fallen angels) and the global financial crisis (GFC) of 2008–2009 (8%). It’s also not much higher than the 7.2% average three-year cumulative downgrade rate (Display 2). But with the investment- grade corporate bond market now roughly four times its 2008 size, the absolute value of downgraded debt will be larger than prior crises.

Display 2: In Percentage Terms, Fallen-Angel Expectations Are Similar To Prior Crises

Percent of Index Downgraded to Fallen Angels

Historical analysis and forecasts do not guarantee future results.

Global corporates represented by Bloomberg Barclays Global Corporate USD Unhedged

As of March 31, 2020

Source: Bloomberg, Moody’s and AB

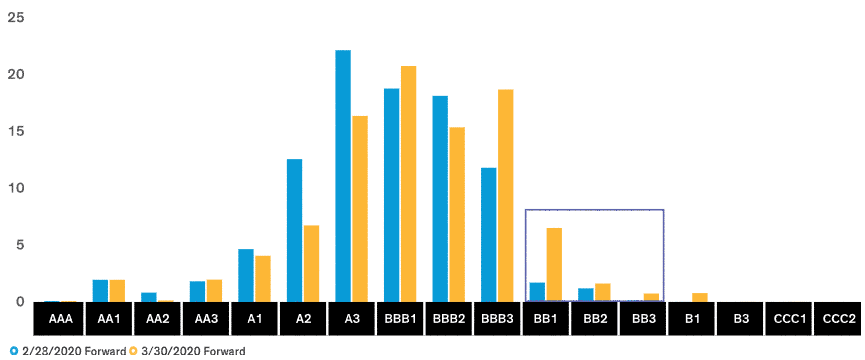

Display 3: Most Fallen Angels Expected To Be BB-Rated

AB Forward Ratings (Percent)

Analysis provided for illustrative purposes only and is subject to revision.

As of March 31, 2020

Reflects PRISM forward ratings. Percentages represent shares of Bloomberg Barclays US Investment Grade Corporate in par value. Universe covered by AB research totals 82% of the index.

Source: AB

Fallen-Angel Challenges for Insurance Investors

A potential fallen-angel wave of this size has major implications for insurance companies. Globally, insurers have been among the heaviest BBB buyers, moving deeper into the lowest level of investment grade to boost income in an environment of low interest rates and tight credit spreads.

Regulatory requirements and internal investing restrictions make fallen-angel risk a constant presence for insurance companies. High-yield bonds carry a steeper capital charge—longer-maturity bonds in particular, under some regulatory jurisdictions. Many insurers limit high-yield exposure—and some prohibit it altogether. These structural constraints can lead to forced selling.

Accounting headaches can emerge, too. When an insurer’s bond holding is downgraded to high yield, it may trigger a write-down review. This assessment would determine whether the insurer needs to book an impairment, under the assumption that the issuer may ultimately default and prevent the recovery of the bond’s full par value.

Despite the pressures fallen angels put on insurers, the transition can also create opportunities—so there are clearly risks from reducing credit exposure at the wrong time. Given the unique position of insurance investors in the credit space, how should they get ready for the coming wave?

Looking Under the Wave’s Surface

The first step is to look beneath the wave to understand what’s driving it, how far it will reach and which issuers might be caught up in it.

Bear in mind that BBB issuers won’t leave the investment-grade ranks quietly. There are strong incentives to stay put, notably the desire to remain eligible for Federal Reserve support programs. And even if an issuer is downgraded to high yield, the recent extension of the Fed’s backstop to include some fallen angels will help issuers by maintaining access to capital and providing liquidity relief.

Most corporate bond issuers that we expect to join the fallen-angel wave likely won’t fall too far. Based on our fundamental reassessment, most will settle at the upper tiers of BB (Display 3), with very few falling deeper into high-yield territory. This suggests that the higher capital charge for insurers holding newly fallen angels would be relatively limited.

A Few Hard-Hit Sectors—But Opportunities Elsewhere

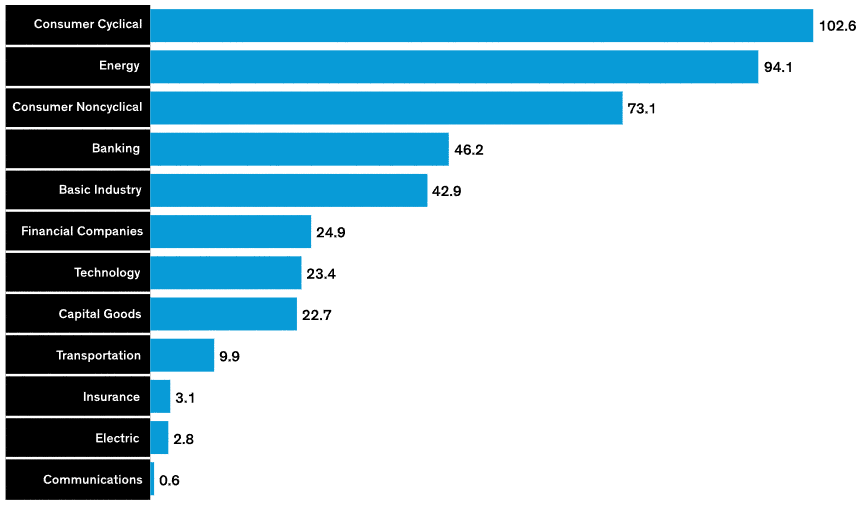

It’s no surprise that the sectors expected to contribute the most to fallen-angel risk are those hit the hardest by COVID-19 disruptions and collapsing energy prices. Issuers who boosted their financial leverage to enable merger and acquisition activity are also vulnerable.

The sectors we expect to be hit the hardest include airlines and consumer cyclicals—autos, gaming, home construction and retail. When people aren’t traveling for work or leisure, and when they can’t shop for items beyond those deemed essential, industries in the impact zone will feel a lot of pain.

Energy will feel its share of the pain, too, led by independent exploration and production issuers. Consumer noncyclical companies—namely food and beverage issuers that levered up for mergers and acquisition—will be under pressure, too.

Outside these areas (Display 4), the rest of the fallen-angels should be reasonably well distributed across industries. Because many of them may be painted with the same brush, opportunities arise for investors who do their credit homework and identify usually sound companies caught in the wave.

Display 4: Downgrades Expected To Be Largely Well Distributed

US Investment-Grade Average Forward Ratings Changes Since 2/28/2020: Share of Investment-Grade Index

Analysis provided for illustrative purposes only and is subject to revision.

As of March 31, 2020

Reflects PRISM forward ratings. Percentages represent shares of Bloomberg Barclays US Investment Grade Corporate in par value. All updated credits as 82% of AB’s coverage and 73% of US investment grade

Source: AB

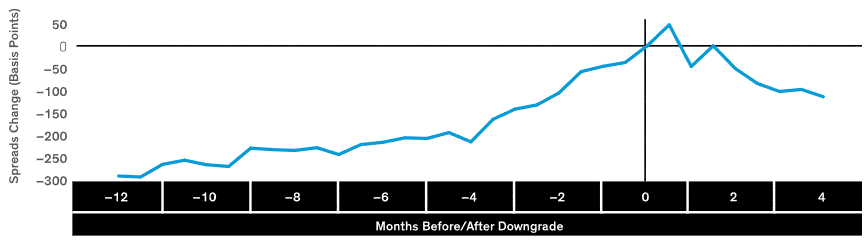

Display 5: Fallen-Angel Spreads Have Widened Before Actual Downgrade

Historical analysis does not guarantee future results.

As of March 31, 2020

Median fallen angel from 2010 through 2018

Source: Barclays Research, Bloomberg and AB

Forced Selling of Fallen Angels Can Lock in the Pain

The prospect of forced selling of a credit downgraded to high yield is a familiar one for many insurance investors, given the scrutiny of regulatory regimes and internal guidelines. We understand that these are critical considerations, but we also believe more flexibility is needed.

Historically, markets have recognized struggling issuers and repriced them long before official credit ratings catch up. As a result, most credit-spread widening happens before an official downgrade to high yield (Display 5). Once ratings confirm high-yield status, the pain has already been inflicted. So, selling an “official” fallen angel gets the timing wrong—locking in the return penalty from spread widening.

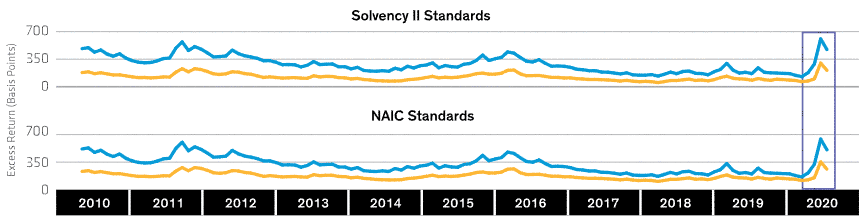

Currently, credit spreads remain wider than normal. The excess return net of capital costs for BBB-rated credits (Display 6) is more attractive than it was for BB-rated bonds at the end of 2019—high enough to justify the risk of fallen angels. And BB-rated credits appear very attractive outright, suggesting that incorporating flexibility to hold high yield in a strategic asset allocation makes sense.

Display 6: BBB/BB Compensation Is Attractive After Capital Costs

Historical analysis and forecasts do not guarantee future results.

Through April 30, 2020

The return on equity for both NAIC and Solvency II are assumed to be 10% and tax rates 20%. Solvency II examples use BBB five-year capital charge and BB three-year capital charge. Yield spreads are from Bloomberg Barclays US Corporate Bond.

Source: Bloomberg and AB

Can the High-Yield Market Handle the Wave?

The flow of fallen angels related to the COVID-19 economic shutdown will certainly be unprecedented in terms of its dollar volume. Based on our forecasts, the wave could amount to as much as 35% of the existing high-yield bond market. But in our view, the market should be able to absorb this volume.

Of course, some disruption is to be expected—the pace of the wave will matter, as investment accounts make room for this new supply. But the high-yield market has shown the ability to digest large volumes of fallen angels before. During one week in March, it absorbed both the largest fallen angel on record (Ford) and the fourth-largest (Occidental Petroleum), and still managed to rise by 7%.

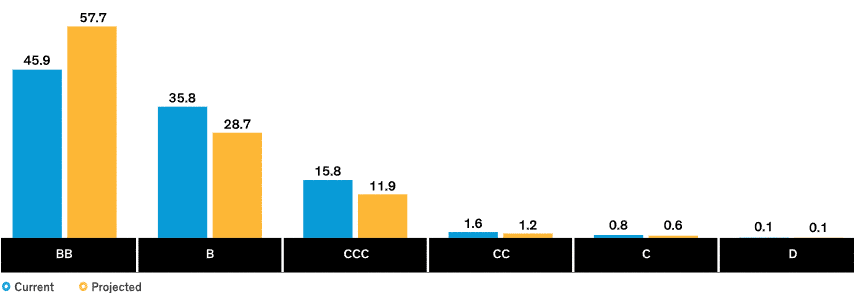

A large inflow of formerly BBB-rated bonds also boosts the quality of the high-yield market. This can draw more investors to highyield bonds to snap up quality companies with strong franchises and brands that have been caught up in the downturn—but will likely survive it. BB-rated bonds are about 45% of the high-yield market today, and that could rise to near 60% with incoming fallen angels (Display 7).

Policy Support For Certain Issuers Under Stress

Fallen angels weren’t overlooked in the blizzard of policies rolled out to support the US economy and help financial markets keep functioning.

The Fed expanded its Primary Market Corporate Credit Facility (PMCCF) and Secondary Market Corporate Credit Facility (SMCCF) to $750 billion in purchases, backed by $85 billion from the US Treasury. The Fed will also use the Main Street Lending Program (MSLP) to buy up to $600 billion in small and midsize business loans outright, using $75 billion from the US Treasury. These programs help shore up credit markets.

Within the corporate purchase programs, the Fed has made some fallen angels eligible for purchase, as long as they were rated investment grade as of March 22 and have since been downgraded to BB. The SMCCF’s inclusion of fallen angels as eligible purchases should help relieve the pressure on markets from the anticipated fallen-angel wave and reduce the risk of fallen angels being closed out of capital markets.

The Fed’s actions won’t stop the wave of fallen angels and defaults—in fact, some downgrades have already begun. But we do expect the programs to backstop liquidity for US firms that were otherwise financially solvent before the crisis interrupted their access to relatively inexpensive funding.

Display 7: Implied Fallen Angels Would Alter The US High Yield Index

High Yield Ratings as Percent of Index

Analysis provided for illustrative purposes only and is subject to revision

As of March 31, 2020

Reflects PRISM rating changes. Percentages represent par value as a percent of Bloomberg Barclays US High Yield Corporate Bond. Adjusted for issuer constraint of 2% of index.

Source: Bloomberg and AB

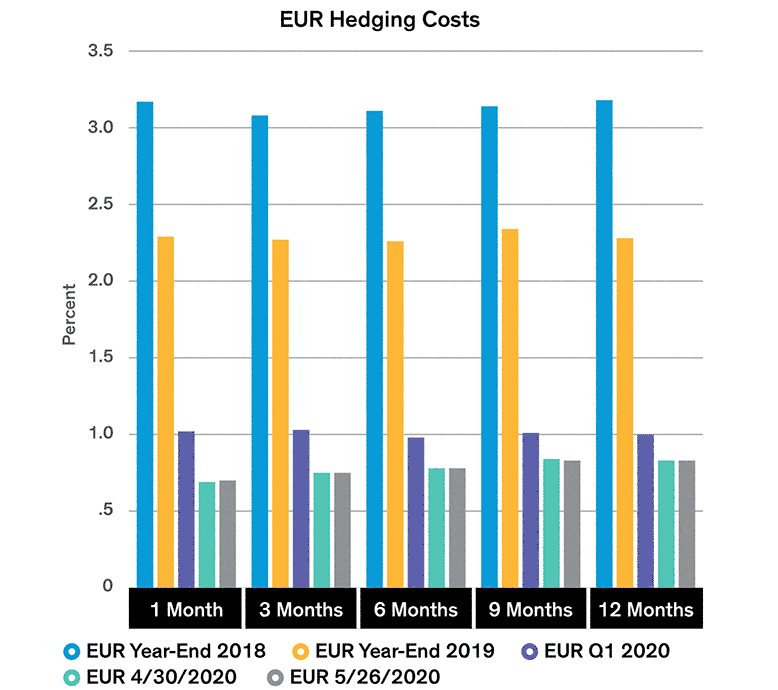

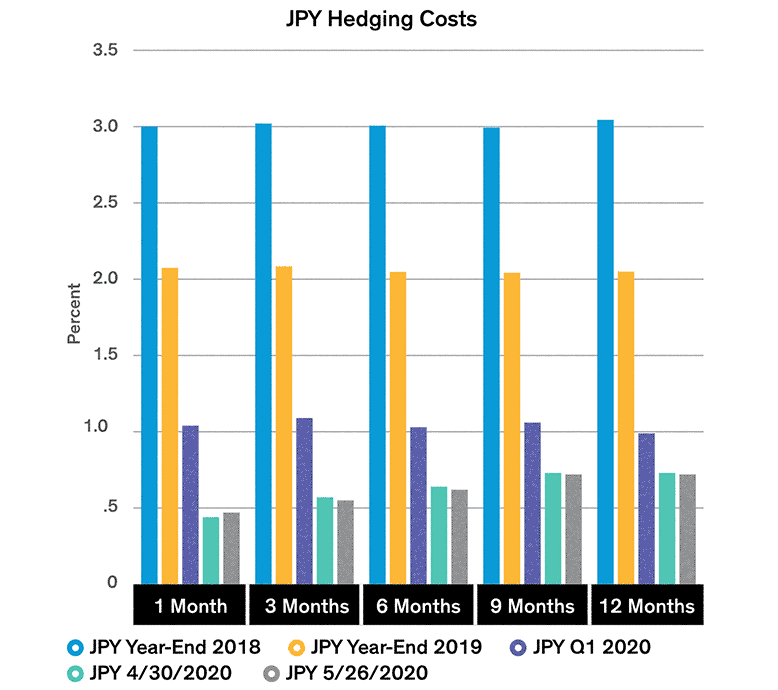

Display 8: Lower Hedging Costs Support Technical Environment For US Credit

Historical and current analyses do not guarantee future results.

As of May 26, 2020

Source: AB

The Watchword for Insurers: Flexibility in Credit Exposure

What does all of this mean for insurance investors that need to balance the search for income and yield with maintaining an appropriate level of quality in their bond portfolios?

First, we think it’s important to avoid being forced sellers of fallen angels, which would simply lock in the pain. Given the current environment, we think the upper tier of the high-yield market and the lower tier of the investment-grade market should be viewed as part of the ratings continuum—not a clear divide.

At this juncture, many insurers are under capital constraints, with likely reduced solvency ratios from lower interest rates and mark-tomarket degradation of credit assets. However, they could provision for the higher capital costs of fallen angels by reducing other risky assets—equities, for example, which have rallied recently. This would provide more room to maneuver.

If local insurance regulatory frameworks and internal risk-management controls permit insurers to invest in fallen-angel corporate bonds, we think this is a good time to consider using that flexibility to hang onto debt from firms struggling under the stresses created by the COVID-19 economic shutdowns.

Lower hedging costs add to the widespread attractiveness of the credit opportunity (Display 8). The 12-month hedging cost for a European insurer in US markets was 3.2%; that cost has dropped to 2.3%. For Japanese insurers, hedging costs have declined from 3.0% to 2.1%. Not only does that create attractive opportunities, it’s also likely to provide technical support to US credit.

Looking at the Big Picture

The bottom line for insurance investors? There’s an opportunity—by adding a bit of flexibility—to build compelling credit portfolios that are less susceptible to downgrade while also ensuring that current valuations accurately reflect the desired risk profile.

But the unique nature of the COVID-19 crisis will affect the dynamics of every industry differently than they would in a typical economic downturn. This reality puts a premium on the ability to underpin security- selection decisions with strong fundamental credit analysis—not just access credit opportunities through passive market allocations.

Download PDF

There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results.

The information contained herein reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. The views expressed herein may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AllianceBernstein or its affiliates.

Note to Canadian Readers: AllianceBernstein provides its investment-management services in Canada through its affiliates Sanford C. Bernstein & Co., LLC and AllianceBernstein Canada, Inc. Note to European Readers: European readers should note that this document has been issued by AllianceBernstein Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. The registered office of the firm is: 50 Berkeley Street, London W1J 8HA. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). The information in this document is intended only for persons who qualify as “wholesale clients,” as defined in the Corporations Act 2001 (Cth of Australia), and should not be construed as advice. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AllianceBernstein is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AllianceBernstein is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AllianceBernstein does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Taiwan Readers: AllianceBernstein L.P. does not provide investment advice or portfoliomanagement services or deal in securities in Taiwan. The products/services illustrated here may not be available to Taiwan residents. Before proceeding with your investment decision, please consult your investment advisor. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investmentmanagement company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2022 AllianceBernstein L.P., 1345 Avenue of the Americas, New York, NY 10105