Fusion Ignition and its Impact Implications

“This astonishing scientific advance puts us on the precipice of a future no longer reliant on fossil fuels but instead powered by new clean fusion energy” – Chuck Schumer1

Investors have been tempted for more than half a century by nuclear fusion’s promise of safe, reliable baseload without environmentally harmful emissions or radioactive waste. However, it wasn’t until California’s Lawrence Livermore National Laboratory announced the first successful “ignition” in late 2022 that fusion entered mainstream discussions (Figure 1). That news has led some to conclude that the decarbonization solution is at hand, potentially de-emphasizing the urgency and perceived benefits of installing new renewable energy. This post challenges that conclusion and argues that, given the discernible, positive impact of existing decarbonization technologies, the importance of investments in these areas will only grow with the passage of time.

Figure 1: Looks complicated—the target chamber at Lawrence Livermore National Laboratory where fusion ignition occurred on December 5, 2022

Source: Lawrence Livermore National Laboratory

Fusion’s Promise

Fusion is effectively the reverse process to fission—instead of splitting a nucleus (of enriched uranium), the nuclei of two or more atoms (of hydrogen isotopes) are combined. If fusion can be scaled, it would offer the primary benefits of fission—reliable baseload with low emissions and a small geographic footprint—without most of fission’s drawbacks.2 Fusion has no real risk of meltdown, generates only low-radioactivity, fast-decaying waste, and does not require enriched uranium.3 Instead, one of its fuels, deuterium, is abundant in sea water, and experiments to “breed” the other, tritium, on site could enhance energy security.4

Ignition Not the Same as Overall Net Positive Energy

Although achieving ignition—when fusion outputs more energy than it consumes—is a major milestone, it represents a relatively small step. The reaction depended on lasers, but “ignition” only considers the energy those lasers delivered inside the reactor, not the electricity that powered them. When accounting for the entire operation, the “ignition” consumed about 100x more energy than it created.5

The bigger breakthrough will be when a reactor creates significant net-positive overall energy, which is likely to still be years away (if it happens at all). The reactor in California functions by rapidly compressing and heating a tiny fuel pellet using x-rays delivered by powerful lasers. Improving the timing of the reaction and the quality of the fuel pellet will be key to producing more energy. The hope is that each successful experiment enhances researchers’ understanding and leads to additional breakthroughs. Still, much more progress will obviously be needed to balance the significant electricity needs of the lasers. That said, the “laser” design – known as inertial confinement – may not be the most viable design in the long-run. Most investment and commercial research has been based on magnetic confinement designs that aim to compress heated fuel using super-conducting magnets, which may be more successful at outputting sustained net positive energy.6 However, no magnetic confinement reactor has yet reached ignition.

A Solution that Entails More Global Capacity than Currently Installed

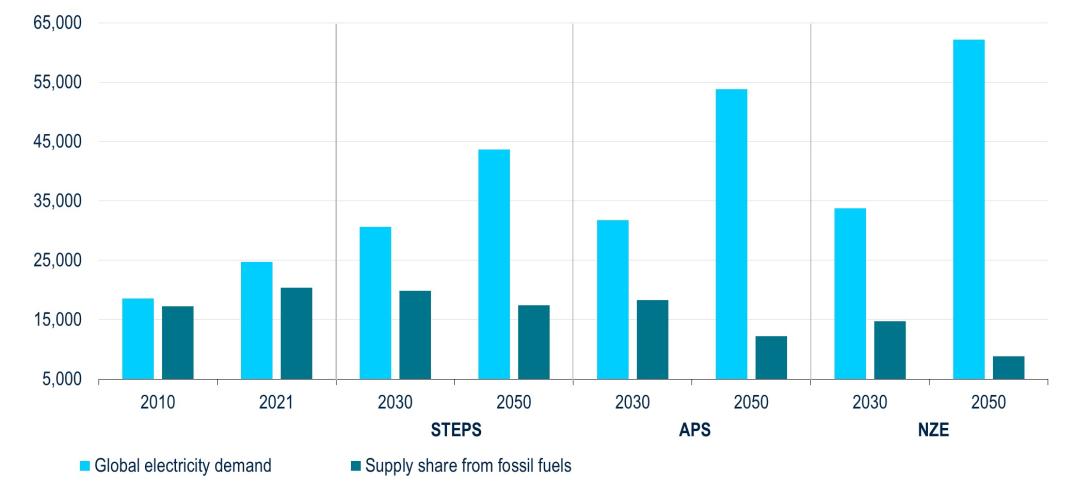

Once a sustained, net-positive reaction is achieved, nuclear fusion plants must be financed and built. Figure 2 shows that this is no small task considering the supply and demand dynamics. In terms of the latter, electricity demand is projected to surge, especially in scenarios aligned with Paris targets where it would more than double by 2050.

On the supply side, even assuming a very generous 90% efficiency rate, replacing the roughly 2/3 of electricity currently generated by fossil fuels would require almost 2,000 gigawatts (GW) of fusion capacity.7 However, early prototypes are anticipating capacity factors of just 20-30% due to several factors, including anticipated maintenance, availability of cooling water, and operational needs (e.g., cooling systems and tritium breeding). Therefore, for fusion to be the decarbonization solution, installed capacity would need to reach 10,000 GW before mid-century—a level that exceeds all electricity capacity installed today.

The Growth in Global Electricity Demand is Expected to Increasingly Exceed Sources Derived from Fossil Fuels (TWh)

Source: PGIM Fixed Income and International Energy Agency, World Energy Outlook 2022. STEPS refers to Stated Policies Scenario, APS refers to Announced Pledges Scenario, and NZE refers to Net Zero Emissions by 2050 scenario.

The Need for Accelerating Electrification, Connection, and Conservation

Another consideration of fusion is that it creates electricity, which only makes up about 20% of global final energy consumption.8 Fusion is of little help for the other 80% unless that too is electrified. For example, transportation makes up over 25% of energy consumption and more than 90% of this still came from oil products in 2020, versus just over 1% from electricity. A similar story is true for electrification of buildings’ heat, where fossil fuels and biomass still dominate. In both cases, electrification is making inroads, but remains well behind the pace needed to achieve the Paris targets. Additionally, around 25% of global emissions are not related to energy at all.9 Thus, even if fusion were viable, investments in electrification and other decarbonization technologies need to rapidly accelerate.

Similarly, fusion (and renewables) cannot help with decarbonization without being connected to consumers. It’s an area of severely neglected investment—in its Net Zero Emissions scenario, the IEA estimates investment in grids and transmission needs to more than double by 2030.10 As a result of the foregone investment, renewable projects in most developed market countries face long connection times, e.g., an average of seven years in the U.S. and the UK. Meanwhile, 774 million people globally still lacked reliable electricity access in 2022.

Finally, a discussion of energy generation neglects a foremost consideration. As the adage goes, the cleanest energy is the energy you don’t use. It is also usually the cheapest. Yet, investments and policies promoting efficiency and demand reduction are also well behind Paris-aligned pathways.11

Intangible Impact

While much is said about fusion’s potential, the preceding points indicate that its impact is not yet ascertainable. Even in a best-case scenario where fusion is commercially viable by the late 2030s, it could still take several additional decades to build the initial generation of plants. And several more decades before fusion makes up a material share of the energy mix (to say nothing of the astronomical costs). Meaning that even in this best-case scenario, fusion may not make a significant contribution until late this century.12

But time is of the essence. At current rates, the 1.5C° carbon budget is projected to be completely depleted in less than 10 years. At that point, warming of 1.5C° or more will be locked in. To avoid this, immediate emissions cuts on the order 8% per year are needed—making a scenario of abundant fusion energy after mid-century far too late.

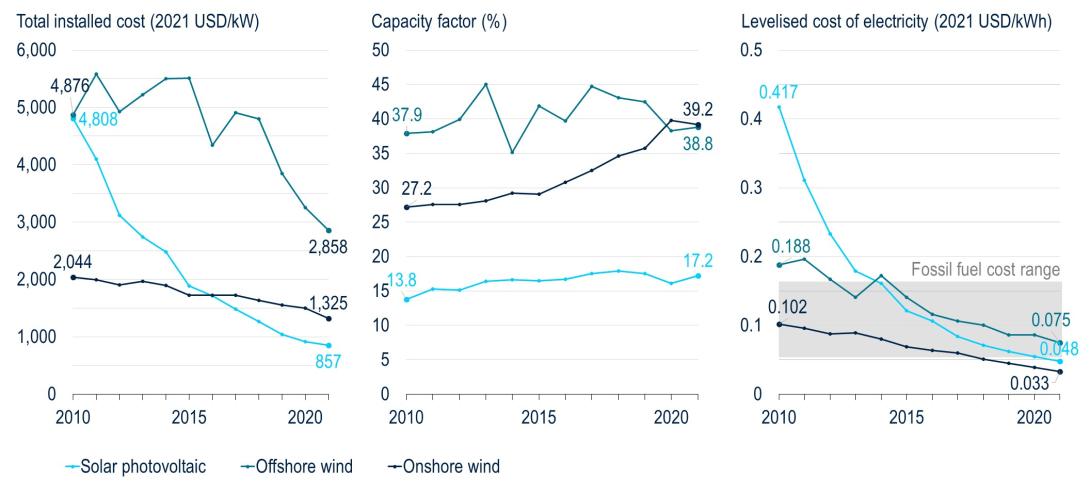

This scenario stands in stark contrast to the prospects for existing renewables. The IEA estimates the average time needed to build a new renewable project is now less than two years.13 The costs of renewables and storage have also rapidly decreased and are expected to continue dropping over time (Figure 3).14 So, it is possible fusion may not be cost competitive if/when it becomes commercially viable.

The Tumbling Costs of Renewable Energy Projects

Source: PGIM Fixed Income and International Renewable Energy Agency

The upshot is that even if fusion becomes a reality, it will only be a fraction of the solution. A massive expansion of other clean energy technologies (and a continuation of some fission power) will be urgently needed as well.

Conclusion

The first successful fusion ignition is an undeniable scientific achievement. Yet, it was nowhere close to producing overall net-positive energy, and even if/when that is achieved, it could take several decades more for fusion to make a positive impact on decarbonization. Dwindling carbon budgets are set to be depleted well before then.

Therefore, as we monitor advancements in fusion technology, we remain focused on conservation as well as the positive effects of renewable energy sources. These continue to bring identifiable, positive impacts to decarbonization and those portfolios oriented on achieving positive environmental impacts.

Read More from PGIM Fixed Income

1 “National Ignition Facility achieves Fusion Ignition,” the Lawrence Livermore National Laboratory, December 14, 2022. The quote is attributed to Senator Chuck Schumer, (D) New York.

2 Traditional nuclear power is concentrated in a handful of countries and makes up around 5% of total energy supply (and 10% of electricity). Its primary benefit is reliable baseload with few greenhouse gas (GHG) emissions. Its downsides include nuclear waste, a small portion of which remains highly radioactive for centuries; the risk of meltdowns; uranium enrichment potentially contributing to nuclear weapons programs; water intensity; and high upfront costs and prolonged construction times that are frequently well above expectations.

3 The reaction requires a constant input of fuel, so cannot become self-sustaining.

4 In “breeding,” tritium would be produced as part of the fusion reaction in certain reactor designs. Free neutrons escaping the reaction would interact with lithium isotopes in the material surrounding the reactor vessel to create new tritium. This is crucial as tritium is extremely rare in nature, and existing global production is far below the needs of even a single commercial fusion reactor.

5 Inside the reactor, 2.05 megajoules were input for 3.15 megajoules of output. The lasers required 300 megajoules of energy to create the ignition. And, the reaction lasted less than a second.

6 An experimental prototype under development – the Joint European Torus project – is expected to require 700-800 MW of power. The hope is that commercial reactors will require only 200-300 MW as magnetic coils become more efficient, and could produce as much as 1-2 GW of power, though this is still theoretical.

7 For context, less than 400 GW of fission capacity is installed today.

8 Power generation’s share of GHG emissions is slightly higher than its share of final energy consumption, at around one quarter.

9 The large majority (though not all) of these are related to agriculture, forestry and land use. Waste is also a major contributor, as well as industrial applications (e.g., steel and cement production) that rely on fossil fuels directly in their production processes.

10 From $320 billion today to $740 billion.

11 For instance, the IEA shows total energy consumption falling 9% to 2030 and 23% to 2050 in its 1.5C scenario, but expects it to rise under stated policies.

12 It may also be worth noting that the Lawrence Livermore National Laboratory’s reaction used an inertial confinement design. However, most facilities being developed for commercial use focus on magnetic confinement designs, which have some noteworthy differences, and have yet to achieve successful ignition.

13 This assumes timely permitting, which in some key regions, such as the EU, can currently take longer than actual construction.

14 Notwithstanding the recent stall resulting from higher raw material costs and supply chain disruptions.

The comments, opinions, and estimates contained herein are based on and/or derived from publicly available information from sources that PGIM Fixed Income believes to be reliable. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. Past performance is not a guarantee or a reliable indicator of future results.

Source(s) of data (unless otherwise noted): PGIM Fixed Income as of March 1, 2023.

For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional.

These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy.

Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2023 PFI and its related entities.

2023-1932

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in