Economic backdrop

After a steady stream of interest-rate hikes, the world’s central banks seem to finally be making progress in reining-in inflation. European and UK inflation rates have declined sharply in recent months, however, worries about a looming recession remain. Meanwhile, in the US, the annual core rate of inflation in October dropped to its lowest point since August 2021. Overall, the US economy has held up quite well, especially when compared to those elsewhere in the world. While it has been able to avoid recession, there are hints that economic growth may finally be slowing in the wake of the Federal Reserve’s higher-for-longer interest-rate policy. US consumers pulled back on retail spending in October, raising concerns they may be running out of steam as they head into the holiday season. On the manufacturing front, recent surveys showed a dimmed outlook with a noticeable negative shift in the comments from participants. This sets up a more challenging dynamic for the economy going forward.

Still, despite the recent signs of cooling, the US economy has fared better than those in Europe and the UK, which appear to be on the precipice of recession. GDP for the 20 countries that comprise the eurozone declined by an annualized 0.4% in the third quarter after scratching out a meager 0.6% gain in the second quarter. Meanwhile, China’s property bust continues to serve as a drag on that country’s economy, despite government efforts to mitigate the fallout.

We currently hold that the US economy will experience a recessionary-type environment in 2024 but are cognizant to the prospect of a positive, albeit sub-trend growth scenario playing out. A main difference in these two scenarios is the speed of rate cuts on the other end—faster in the former and slower in the latter. We also see Europe and the UK heading into a shallow recession next year as the impact of central banks’ higher interest rates feeds into those economies.

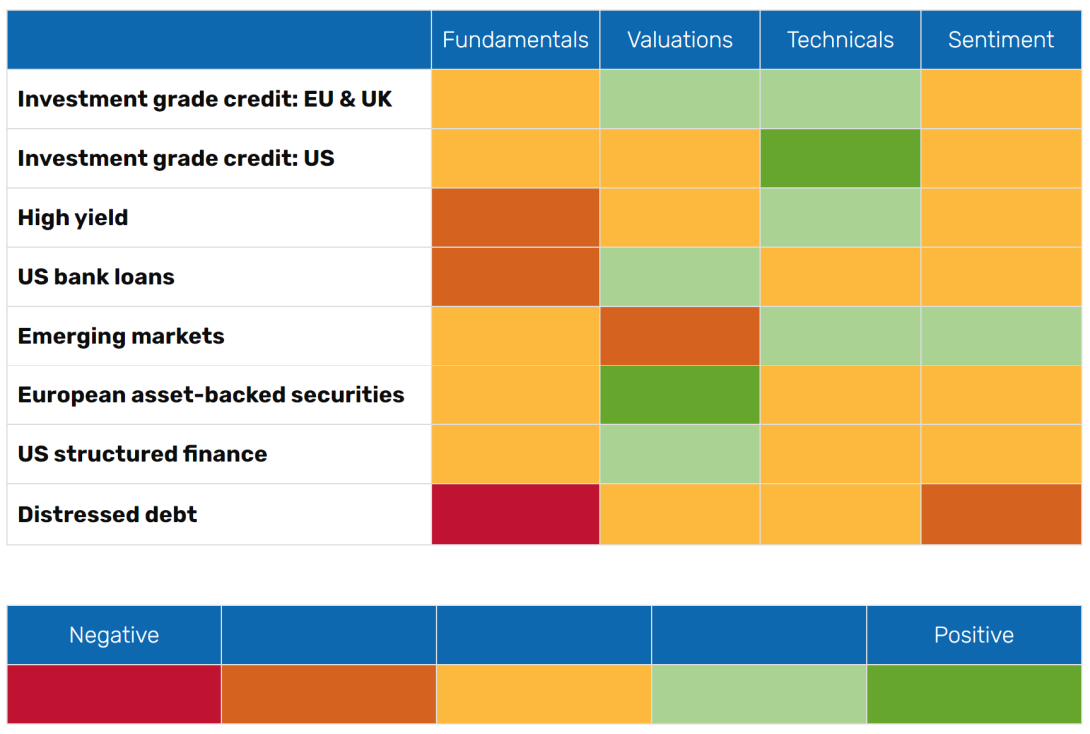

Global corporate credit research overview

- Fundamentals generally stable, but softer economic environment to pressure growth and margins

- Increasing divergence between higher- and lower-quality issuers with companies with near-term maturities and limited access to the markets becoming more concerning

- Consumer sectors, especially services, are expected to be more resilient than companies in the basics and industrial space

- Continue to favor sectors and companies better positioned to weather a softer economy and higher rates

The anticipated slowdown in economic activity is taking hold, putting some pressure on margins and earnings growth. The impact on balance sheets and overall credit metrics will likely remain somewhat muted, resulting in continued stable fundamentals across most sectors. That being said, with higher rates and a weakening economy we expect a greater divergence between high-grade and levered issuers in 2024.

The rate hike cycle seems to be largely complete, which has reduced demand and begun to lower inflation, although it still remains at elevated levels. Lower inflation is more notable in consumer goods sectors, as services-focused companies continue to see strong demand as the post-pandemic shift toward travel and other experiences continues. Wage inflation remains resilient however, buoyed by low unemployment that has only recently showed signs of easing. This has also supported consumer spending, with concerns concentrated in lower-income cohorts impacted by rising borrowing costs and tightening lending standards. At the same time, higher-income consumers have also become more cost conscious with increased purchasing activity at higher-value/lower-cost retailers.

Supply chains have largely normalized, allowing inventory levels to come down, free up capital and lower just-in-time logistics costs. However, there are pockets of issues in certain consumer and basics sectors that could lead to some price discounting to preserve market share. The slow recovery in China has created headwinds for many industrial companies, including those exposed to commodity prices in the chemical, metals/mining and energy sectors. Interest-rate sensitive sectors such as housing and autos are relying on increased incentives to support demand. Financials appear to have stabilized following difficulties in US regional banks and Credit Suisse’s failure early in the year. Consumer credit profiles and commercial real estate loans remain in focus, but most larger firms appear to have manageable exposures.

Capital adequacy levels across financial companies and leverage ratios across corporates in most industries are healthy, though interest coverage ratios and cash balances are expected to continue declining from recent highs, notably in the levered credit markets.

We expect debt-financed mergers and acquisitions and leveraged buyout activity will remain subdued due to higher financing costs, increased regulatory scrutiny and an uncertain economic environment. As a result, those with strong free cash flow generation and well-positioned balance sheets may shift some capital allocation toward shareholder-friendly activities.

After several rating upgrades in the energy sector, we expect more balance going forward between rising stars and fallen angels, though within high yield we expect downgrades to outpace upgrades. In a higher-for-longer interest-rate environment, companies with near-term maturities are becoming more concerning, particularly for those with the lowest ratings that may have limited market access. Overall, we remain cautious, favoring companies and sectors better positioned to weather an uncertain economic landscape.

Fixed income outlook

- Higher yields present opportunity despite ongoing volatility, economic uncertainty

- Sector and security selection will be key given the likely economic slowdown

- Avoid taking on risk without getting paid for it given weakening growth

Fixed income assets are set to begin 2024 at broadly attractive levels, with Treasury yields near their highest since the financial crisis, albeit off recent peaks. The repricing higher in yields has increased breakevens (or yield per unit of duration) to their most compelling levels in years, which can offer protection against ongoing volatility or further increases in yields.

The recession, which many market participants had anticipated in 2023, never materialized. Instead, a surprisingly resilient economic backdrop amid restrictive monetary policy sent long-dated yields higher, leading to a challenging return environment for fixed income investors. Expectations continue to suggest an economic slowdown next year and the evolution of economic activity will drive market conditions in 2024.

While our base case implies a recessionary-type environment in 2024, a period of positive, but below-trend growth, remains a possibility. As the economy slows, excess returns for lower-quality credit products could face challenges, but an easier stance of monetary policy holds the potential to support total returns. Sector and security selection will be of heightened importance in an economic slowdown given the likelihood of concentrated pockets of weakness in the economy following a prolonged period of elevated funding costs. It is wise to be selective when considering spread-based fixed income opportunities and to avoid credits where investors are not getting paid for the risks given this slowing to no/negative growth environment.

Please download the PDF below to read our outlook in its entirety, including individual asset class outlooks.

DOWNLOAD

Unless otherwise noted, the information in this document has been derived from sources believed to be accurate at the time of publication.

This material is provided by Aegon Asset Management (Aegon AM) as general information and is intended exclusively for institutional, qualified, and wholesale investors, as well as professional clients (as defined by local laws and regulation) and other Aegon AM stakeholders.

This document is for informational purposes only in connection with the marketing and advertising of products and services, and is not investment research, advice or a recommendation. It shall not constitute an offer to sell or the solicitation to buy any investment nor shall any offer of products or services be made to any person in any jurisdiction where unlawful or unauthorized. Any opinions, estimates, or forecasts expressed are the current views of the author(s) at the time of publication and are subject to change without notice. The research taken into account in this document may or may not have been used for or be consistent with all Aegon AM investment strategies. References to securities, asset classes and financial markets are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions. It has not been prepared in accordance with any legal requirements designed to promote the independence of investment research, and may have been acted upon by Aegon AM and Aegon AM staff for their own purposes.

The information contained in this material does not take into account any investor’s investment objectives, particular needs, or financial situation. It should not be considered a comprehensive statement on any matter and should not be relied upon as such. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to any particular investor. Reliance upon information in this material is at the sole discretion of the recipient. Investors should consult their investment professional prior to making an investment decision. Aegon AM is under no obligation, expressed or implied, to update the information contained herein. Neither Aegon AM nor any of its affiliated entities are undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable US federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

Past performance is not a guide to future performance. All investments contain risk and may lose value. This document contains “forward-looking statements” which are based on Aegon AM’s beliefs, as well as on a number of assumptions concerning future events, based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees of future performance, and actual outcomes and returns may differ materially from statements set forth herein.

Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans and such prepayments cannot be predicted with accuracy. There is no guarantee that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation or that such collateral could be liquidated if necessary.

Investing in foreign-denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, economic and political risks, which may be enhanced in emerging markets.

Investments in high yield bonds may be subject to greater volatility than fixed income alternatives, including loss of principal and interest, as a result of the higher likelihood of default. The value of these securities may also decline when interest rates increase.

Structured Finance assets (such as ABS, RMBS, CMBS and CLOs) are complex instruments and may not be suitable for all investors. The assets may be exposed to risks such as interest rate, credit, liquidity, issuer, servicer, underlying collateral, prepayment, extension, and default risk. Investors typically receive both interest and principal payments for a security, and these prepayments may reduce the interest received and shorten the life of the security. Although some types of structured finance securities may be generally supported by a form of government or private guarantee, there is no assurance that guarantors will meet their obligations.

The following Aegon affiliates are collectively referred to herein as Aegon Asset Management: Aegon USA Investment Management, LLC (Aegon AM US), Aegon USA Realty Advisors, LLC (Aegon RA), Aegon Asset Management UK plc (Aegon AM UK), and Aegon Investment Management B.V. (Aegon AM NL). Each of these Aegon Asset Management entities is a wholly owned subsidiary of Aegon Ltd. In addition, Aegon Private Fund Management (Shanghai) Co, Ltd., a partially owned affiliate, may also conduct certain business activities under the Aegon Asset Management brand.

Aegon AM UK is authorized and regulated by the Financial Conduct Authority (FRN: 144267) and is additionally a registered investment adviser with the United States (US) Securities and Exchange Commission (SEC). Aegon AM US and Aegon RA are both US SEC registered investment advisers. Aegon AM NL is registered with the Netherlands Authority for the Financial Markets as a licensed fund management company and on the basis of its fund management license is also authorized to provide individual portfolio management and advisory services in certain jurisdictions. Aegon AM NL has also entered into a participating affiliate arrangement with Aegon AM US. Aegon Private Fund Management (Shanghai) Co., Ltd is regulated by the China Securities Regulatory Commission (CSRC) and the Asset Management Association of China (AMAC) for Qualified Investors only.

©2023 Aegon Asset Management or its affiliates. All rights reserved.

AdTrax: 3648452.9GBL