Has the Market Reshuffled the Public-Private Mix for Insurers?

Richard Roberts, ACCA, CFA | Director—EMEA Insurance Solutions

Dmytro Mukhin, PhD, FSA, CFA | Managing Director and North America Senior Insurance Strategist—Global Business Development

Gary Zhu, CFA | Director—Insurance Portfolio Management; Global Head—Multi-Sector Insurance

What You Need to Know

A vastly different market environment in 2022 has dramatically reshaped the balance of insurance investors’ relative opportunities across public and private capital markets. This shift may create a pause in the growth of private allocations for some insurers as they reassess prospects. However, we don’t expect the long-term trend of growth in private allocations to change.

USD 1.2 Trillion

In Private Debt Assets under Management in 2022

200+ Basis Point

Increase in Public Market Bond Yields from 2020–21 Levels

Wider Dispersion

In Recent Private vs. Comparable Public Yield Spreads

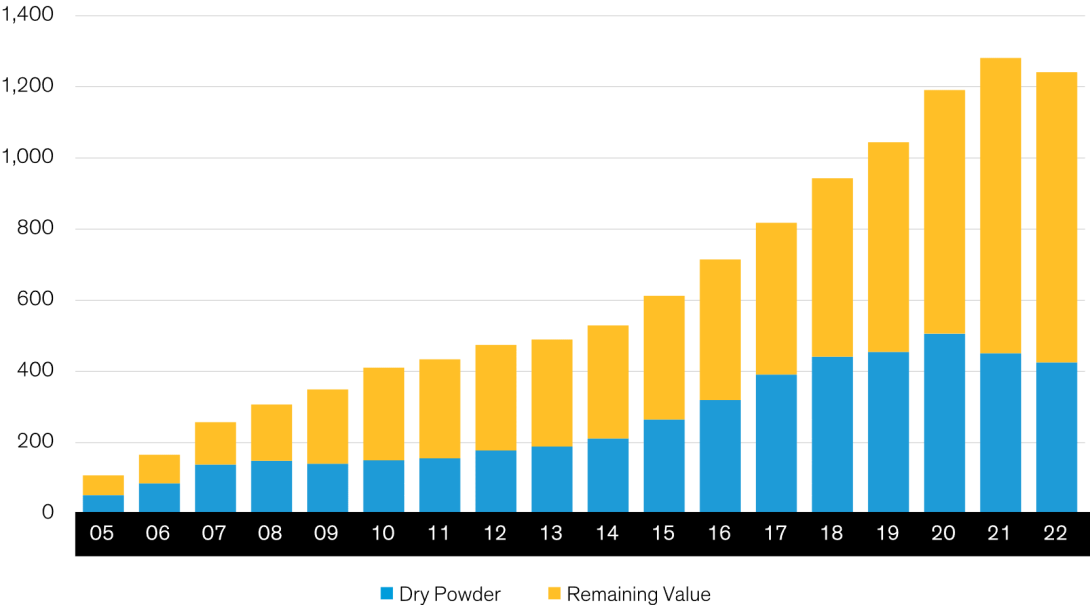

Demand for private assets has swelled since the global financial crisis (GFC) (Display), and insurers have been no exception, steering a growing share of their credit exposure to private markets.

Several factors have fueled demand, including persistently low yields that require a wider net to enhance returns through illiquidity premiums. Also, banks have pulled back from lending to certain private markets, leaving room for other lenders, including insurers, to fill the gap. And the nature of insurers’ liabilities has enabled them to allocate to less-liquid areas.

Private Debt Has Grown Substantially Since the GFC

Private Debt* Assets Under Management (USD Billion)

Past performance does not guarantee future results.

*Includes direct lending, credit special situations, mezzanine loans, bridge financing, real estate debt, infrastructure debt, venture debt and general debt

As of June 30, 2022

Source: Global Private Debt Report: 1H 2022 (PitchBook, September 27, 2022)

After years of heavy focus on allocating to private markets, some insurers may have taken a breath in 2022 to survey what’s now a very different market landscape. What does this mean for the future appetite for private assets?

Higher Yields Make Relative Value Tools More Important

As central banks battled inflation in 2022, interest rates surged globally, pushing public bond yields up from their post-GFC lows—a point when private market demand started picking up in earnest. Overall, yields are up more than 200 basis points from their levels in 2020 and 2021, sharply reducing what had been US$18 trillion of negative-yielding bonds to US$1.7 trillion—roughly back to 2015 levels (Display).

The Amount of Negative-Yielding Bonds Has Tumbled

Market Value of Global Aggregate Negative-Yielding Debt (USD Billion)

Past performance does not guarantee future results.

Through October 21, 2022

Source: Bloomberg and AllianceBernstein (AB)

With overall yield levels much higher, relative-value tools are even more important for investors deciding where to put incremental capital. Yield spreads have widened too but have actually fallen as a percentage of total yield (Display), given the significant climb in government-bond yields. As a result, risk-free rates are driving a greater share of yield, and we think higher-beta asset classes are less attractive than they may seem on the surface. We also don’t think credit sectors have fully priced in the risk of slower growth or recession, so spreads may have room to widen further.

Assessing Relative Value: Spread vs. Total Yield

Credit Spread vs. Treasuries and Credit Risk Premium as Percentage of Total Yield

Past performance does not guarantee future results.

Through October 20, 2022

Source: Bloomberg Index Services and AB

Private-credit spreads have been slower to react than public spreads, given that pricing in private markets tends to lag, though we expect the illiquidity premium to increase from its compressed levels—a process already under way in the fourth quarter. Still, when public and private spreads converged earlier this year, it prompted a question from some investors: Should the ramping up of private-market allocations continue?

We believe that both retail and institutional investors’ allocations across private credit have slowed broadly given the macro volatility, while borrower demand for private funding remains relatively steady. The resulting supply-demand imbalance around capital has contributed to improved pricing through wider spreads or steeper issuance discounts—and through increasingly lender-friendly terms, such as meaningful call protection.

In commercial real estate debt, supply-demand imbalances favor lenders: banks have retrenched, more loans maturing has driven more refinancing (more so in Europe but also in the US) and debt liquidity is flowing to the highest-quality opportunities. Debt pricing has widened as a result of a higher yield base and higher risk premium. Structure is improving for lenders too, providing better downside protection.

For insurers invested in private equity, a difficult 2022 has hurt portfolio performance. Going forward, we think the average return on the average private equity investment will be in line with that of public equities after fees (highlighting the importance of manager selection in the private-equity space). In the context of private assets, and since private equity is generally less aligned structurally with insurers’ needs than is private credit, we think more marginal flows will head into areas other than private equity.

What a Reshuffled Landscape Means for the Focus on Private Assets

Private-spread widening has been catching up to that in public markets, though the illiquidity premium is still compressed in some areas of private markets. That illiquidity premium actually compensates investors for incremental risks, mainly illiquidity but also complexity and possibly credit-profile differences (typically offset by stronger deal structure and documentation). For simplicity’s sake, we’ll call the entire mix an illiquidity premium.

From the tactical lens, we think insurers should ask themselves three questions as they consider short-term allocation decisions:

1. Does the return potential on private assets still fully compensate me for any added risk?

The answer to this question depends on the specific public and private assets in question, but we can outline an example of the considerations in the context of US private placements.

Generally, we can look at relative value through the perspective of illiquidity compensation. In some cases, spreads on US private-placement transactions haven’t been high enough in the absence of more attractive covenants or diversification benefits. Investors with annual quotas may be less sensitive to this lens but faced with a choice between slowing the pace of origination or continuing at pace by adding assets that don’t fully compensate for illiquidity risk, we favor slower origination.

The yield surge is presenting a broader menu of options across public and private fixed income, while spreads are wider, and volatility is up. This environment makes disciplined analysis critical in evaluating relative opportunities, and the ratio of yield spread to total yield is a useful tool. In high-yield bonds, for example, we think the spread should account for two-thirds of total yield. The liquidity premium should be worth more, which means a higher required rate of return.

For insurers seeking to fulfil pre-agreed allocations, alignment is critical, too—with the manager’s view of relative value and with the role of private assets on the insurer’s balance sheet.

2. Does the specific private asset provide risk diversification and bolster my balance sheet?

With volatility and economic uncertainty up and central banks tightening, insurers are reassessing the resiliency of their balance sheets—across assets and on a net asset/liability basis. Inflation is sure to be a focus, including assessing the inflation exposure of current allocations and potential allocation changes at both the sector and asset-class levels.

For example, assets closely related to consumer staples are likely to face challenges in passing on the effects of rising prices to customers, while materials-related assets are expected to have positive correlations with inflation. Generally, sectors exposed to real and physical assets or commodities would likely fare better in higher inflation—and can be found across public and private fixed-income markets.

Several private asset classes combine exposure to real and physical assets with defensive qualities, which could be attractive in uncertain markets. Private markets may also make it easier to combine long-term inflation hedges with defensive characteristics. Real estate debt, for example, avoids taking first-loss exposure, in contrast with real estate equity. What’s more, infrastructure-related investments have historically posted higher recovery rates than corporate bonds.

Floating-rate debt offers potential inflation protection too, though insurers will need to consider their appetite for floating-rate assets within an asset-liability matching (ALM) framework. Floating-rate debt can also be found in public and private markets; much of the private-credit arena is floating rate. Given the heightened macro risks, the balance of insurance portfolios’ exposures to macro and idiosyncratic risks is also worth examining. Focusing on exposures to carefully selected investments driven more by idiosyncratic risk can enhance diversification and may make portfolios more resilient.

Generally speaking, private assets often provide access to different risk drivers than public assets, and their privately negotiated nature often offers greater protections (in the form of covenants). Those protections are certainly attractive in uncertain times.

3. Do I still have the same capacity for illiquid assets today?

Higher volatility and interest rates have raised the issue of illiquidity-risk capacity for the first time in years. The UK liability-driven investment turmoil highlighted that unexpected collateral calls can increase the need for short-term liquidity. Insurers’ hedging requirements differ, of course: they’re fully funded, using derivatives to reduce net asset/liability gaps rather than amplify exposures. However, they’ll likely be stress testing exposures in order to dimension potential liquidity needs.

On the liability side, given the higher costs of living for policyholders, insurers may be considering the impact on policy-lapse experience (particularly within the life insurance sector); lapses can also be a draw on liquidity. In the property-and-casualty space, insurers are likely to be considering the impact of inflation on claims (replacement costs).

Because the value of insurers’ private-market exposures may have declined less than public-market equivalents, private-market allocations may have risen closer to or beyond their targets. To the extent allocations have been based on illiquidity appetites, insurers may pause to think through potential liquidity needs from a liability standpoint before adding less-liquid transactions—though as fully funded investors, their illiquidity appetites are less likely to be affected.

To wrap up the tactical discussion, insurers face a broader menu of investment options, with some public-market options offering comparable expected returns to private-market equivalents. But it’s important to receive adequate compensation for the associated risk and liquidity characteristics (particularly the perceived liquidity of public markets).

Viewing the Problem Through the Strategic Lens

In the long run, we think institutional investors will continue their shift into private markets, because private markets offer genuine portfolio diversification. For insurers, private allocations will also account for ALM considerations, seeking the most efficient return for a given appetite for risk (economic, regulatory or both), as well as portfolio constraints.

For the return side of the equation, we believe private-market assets will continue to exhibit a premium over public-market equivalents (Display) in the long term, driven largely by illiquidity and complexity premiums. The complexity premium can be broadly defined as incremental return for the ability to source, assess and execute customized deals.

Comparing Private and Public Yield Spreads

Select Private Placement Spread Advantage vs. Public Sectors by Rating/Maturity Past performance and current analysis do not guarantee future results.

Past performance and current analysis do not guarantee future results.

Through September 16, 2022

Source: AB

In terms of economic risk, both quantitative and qualitative assessment are needed. On a quantitative basis, private assets often have lower volatility, though some of this likely stems from a lack of daily quoted prices. That makes the qualitative lens important in assessing underlying fundamentals.

Regulatory risk must be assessed on a regime-by-regime basis. In Europe, Solvency II doesn’t distinguish between public and private fixed-income assets, basing the capital requirement for the majority of assets on credit rating and modified duration. However, many private assets don’t have agency ratings, so they typically incur a flat capital charge, roughly between a BBB and BB rated asset under the standard formula. Insurers can develop internal risk models, which may be more sensitive to their investments’ assessed credit risk (often assisted by asset managers’ internal credit ratings).

In the US, regulatory and accounting treatment impacts how insurers craft their strategic allocations, perhaps even more so with public versus private allocations. A changing regulatory environment is an added wrinkle. The National Association of Insurance Commissioners (NAIC), for example, implemented new, expanded capital factors for public bonds and private placements, altering the relative capital efficiency of some bonds. Six capital factors expanded to 20, though they differ only by credit rating—most other capital regimes distinguish by maturity, too.

Fixed-income funds or exchange-traded funds (ETFs) are another interesting case. Normally, a fund investment would be accounted for on Schedule BA in statutory filings, entailing a punitive risk-based capital (RBC) requirement similar to common equity—regardless of the fund’s underlying holdings. This requirement reduces the relative capital-adjusted risk/return attractiveness of private fixed income, which is often offered through a fund structure. The impact is pronounced on small- and mid-sized insurers, who may not have the capacity to hold private assets directly on their balance sheets.

Financial structuring has opened avenues for improving capital treatment. For instance, private-credit funds that issue collateralized fund obligations or rated notes, or that invest through rated feeder funds, enable insurers to treat private assets in a way that’s more in line with the economic risk of the underlying fund investments. Likewise, certain Securities Valuation Office-approved fixed-income ETFs can now receive bond-like RBC and accounting (systematic value) treatment.

Additionally, Senior Schedule BA mortgages can be rated CM1 or CM2, with all other mortgage loans falling into the CM3 category. All else equal, the capital-adjusted relative value of a mezzanine mortgage fund carrying an RBC requirement of only 3% (pre-tax) may impact the size of that allocation versus, for example, a BB+ bond with a 3.15% requirement. Finally, the NAIC is currently working on several initiatives that could change the modelling and capital treatment of securitized assets.

Insurers’ Private Allocations Will Likely Continue Growing…

The ability to diversify public-market exposures is a key argument in the case for greater exposure to private assets, but there’s another strategic angle for insurers to consider. A growing array of private-market investments have the potential to enhance diversification within private allocations as well as more broadly across general accounts.

In addition to well-known areas such as real estate debt, infrastructure lending and private placements, insurers can also consider segments such as middle-market lending, residential mortgages or sub-utility-scale clean energy, areas that may be less crowded. This broader universe makes it easier to access exposures that fit targeted characteristics, whether it’s specific risk drivers, duration profiles or return targets. Private assets also offer greater scope for investors, including insurers, to influence deal structure so that it aligns with insurers’ specific needs. For example, investors seeking to reduce prepayment risk might insist on make-whole clauses in real-estate debt—for a trade-off.

With insurers’ general-account investments increasingly including ESG-related objectives, private markets often offer targeted, more transparent opportunities to channel capital toward these goals. In public markets, investment opportunities are often focused on funding the activities of much broader corporate entities. ESG goals are often climate-related, and funding clean-energy projects through private markets would align with environmental objectives. Targeted private investment in digital infrastructure may satisfy the desire to provide more equitable access in pursuit of social goals.

The regulatory landscape may also provide impetus for further private investment. It’s designed to ensure a sound industry, but regulation can also acknowledge companies’ needs, particularly if there’s common ground on ultimate goals. Amendments to Solvency II regulations on Qualifying Infrastructure Projects and Corporates are a good example. The European Union wants to promote infrastructure investment, such as the Global Gateway initiative. Regulators, after receiving feedback and conducting due diligence, adjusted capital requirements on spread risk, reducing disincentives for insurers to invest in private infrastructure. The US Inflation Reduction Act, though a broad policy change rather than regulation, incentivizes investment in private markets—particularly earlier-stage clean energy firms.

Internal factors will also likely drive private investment, given that many insurers have built substantial capabilities involving investment committee and board approvals as well as engagement with local regulators. They’ll likely be eager to pursue private opportunities, though they’ll need to consider the limits of their resources in assessing and overseeing managers in new asset classes. This situation may spur more interest in strategic relationships with investment managers that have broader capabilities.

…but Public Markets Will Remain a Key Part of Insurance Portfolios

While we think insurers will continue to expand their private-market ambitions, both now and over the long run, we by no means suggest that public markets won’t remain a vital part of general-account portfolios, given their many advantages.

For one thing, public markets offer faster capital deployment for insurers seeking to put money to work rapidly. Investment cost is another consideration: insurers factor investment-management fees into the overall economics of all asset-allocation decisions; within that calculus, fees for public-market investments are generally lower than those of private alternatives.

Liquidity is a major consideration in insurance portfolio design. Public markets have faced occasional liquidity crunches, and liquidity varies across market segments, but public markets clearly offer much more liquid prospects than private markets. In an environment where insurers face greater uncertainty, that liquidity advantage could be weighted more heavily.

Related to the previous two points, public markets bring greater flexibility in making tactical moves as market conditions change, with multisector public fixed-income mandates well placed to take advantage of opportunities from uncertainty and market disruption. Given the volatility we’ve seen in 2022, that can be an attractive trait.

The Big Picture

Recent yield increases, central-bank policy reversals and an uncertain macro backdrop have raised questions that haven’t been visited in some time. Among these are whether the landscape of insurers’ investment opportunities across public and private markets has been reshaped, and what impact this might have on the growth in general account allocations to private assets.

In the short term, we think insurers are likely to increase focus on public-market allocations alongside select, prudent private-market capital deployment. In doing so, relative-value comparisons will be critical, given the different characteristics of each market and higher levels of absolute yields across both. Over a strategic horizon, we see continued growth in insurers’ private-market allocations, given private assets’ distinct advantages and the increasingly diverse investment options available.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in