In the past few years, demand has soared for private market assets as investors have sought to enhance investment returns, protect against inflation, and diversify their portfolios. One of the biggest challenges for private market investors is managing liquidity – maintaining exposures, reducing cash drag, meeting capital calls, and adhering to asset allocation targets. This article is the third in a series about liquidity management tools to complement private market allocations.

Senior bank loan ETFs have been a useful component in institutional portfolios as investor policy goals and objectives are challenged by an inflationary environment that is influencing changes in the forecast returns of all assets. These fixed income ETFs invest broadly in floating-rate senior loans and seek to provide current income consistent with the preservation of capital. They can serve as a satellite to a core bond fund or as a complement to a high yield or private credit allocation.

Potential Income with Reduced Volatility

Senior loans have a low effective duration, which helps to mitigate the mark-to-market volatility of a portfolio when interest rates are volatile. Duration is minimal because loan coupon payments consist of the Secured Overnight Financing Rate (SOFR) or the London Interbank Offered Rate (LIBOR), plus a stated spread. As such, senior loans have seen increasing yields with less volatility as compared to other fixed income asset classes.

With the yield curve likely to remain volatile as the Federal Reserve (Fed) attempts to balance inflationary pressure with economic growth and financial stability, senior loans may be attractive given this short duration. Additionally, senior loans may be more defensive than high yield given their higher average recovery rates historically.1

Loan ETFs as Complements to Private Credit Allocations

Private credit allocations have increased in popularity, promising enhanced returns in exchange for limiting liquidity. However, there are logistical challenges, particularly with drawdown-style funds. Given this, bank loan ETFs have proven to be apt complements to private credit allocations.

Senior bank loan ETFs are designed to actively manage industry and credit exposures based on technical and fundamental views while providing daily liquidity by secondary trading of ETF shares. In addition, to normal-way secondary trading, authorized participants (APs) often stand by to provide additional liquidity in ETF shares at institutional size. As such, even large positions in loan ETFs can generally be readily monetized to fund private credit fund capital calls as needed.

Although bank loan ETFs are not as liquid as the largest stock- or bond-based ETFs, they are still orders of magnitude more liquid than the private market closed end funds that call capital as deals are closed and often have terms of 5-10 years to achieve the higher target returns.

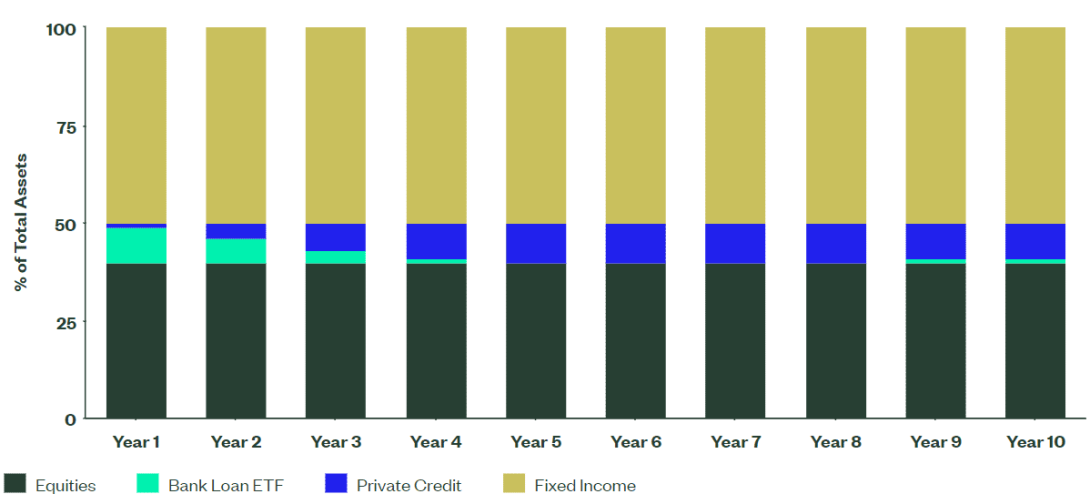

Sample Use Case

Building an allocation of 10% to private growth assets can take a number of years to achieve while managing diversification within the private credit allocation. One approach would be to invest the 10% earmarked for private credit into a liquid alternative, such as bank loans, and use this allocation to fund capital calls as they fall due. Over time, the bank loan allocation will tend to 0% as the private credit allocation increases towards target. We can estimate this path using our cashflow pacing model, an illustrative example of which is included in Figure 1.

Figure 1: Using Bank Loans to Fund Capital Calls for Private Credit

Source: State Street Global Advisors. For illustrative purposes only.

In this example, the Bank Loan allocation is 0% in Year 5, but starts increasing in Years 9 and 10. It is impossible to maintain an exact 10% allocation as private credit investments are illiquid, capital is called when opportunities present themselves, and the allocation in percentage terms depends on how the value of the liquid assets change over time.

The Bottom Line

Senior bank loans play an important role within a total portfolio as a source of diversification, potential risk-return enhancement, and inflation protection. Senior bank loan ETFs provide a liquid complement to these allocations. Additionally, senior bank loan ETFs also provide a meaningful source of income for investors. Exposure and liquidity can be achieved by way of the ETF vehicle – either as individual portfolio components or as part of a multi-asset class customized solution.

We welcome the opportunity to discuss your portfolio’s liquidity and exposure needs. Please contact us for additional information or visit ssga.com to view thought leadership related to liquidity solutions.

1 Source: Blackstone Credit, J.P. Morgan Default Monitor Period: 01/01/2005– 12/31/2022.

Download the Report Here

Disclosures

For institutional / professional investors use only.

Marketing Communication

State Street Global Advisors Worldwide Entities

The views expressed in this material are the views of SSGA’s investment Solutions Group through the period ended April 31, 2023 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs net asset value. Brokerage commissions and ETF expenses will reduce returns.

There can be no assurance that a liquid market will be maintained for ETF shares.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor’s or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor. All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

Investing involves risk including the risk of loss of principal.

Asset Allocation is a method of diversification which positions assets among major investment categories. Asset Allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

© 2023 State Street Corporation. All rights reserved.

Information Classification: General

5696940.1.1.GBL.INST

Exp. Date: 05/31/2024