State Street Global Advisors SPDR® - Tue, 11/09/2021 - 19:56

Innovations with ETFs in Insurance General Accounts

Insights

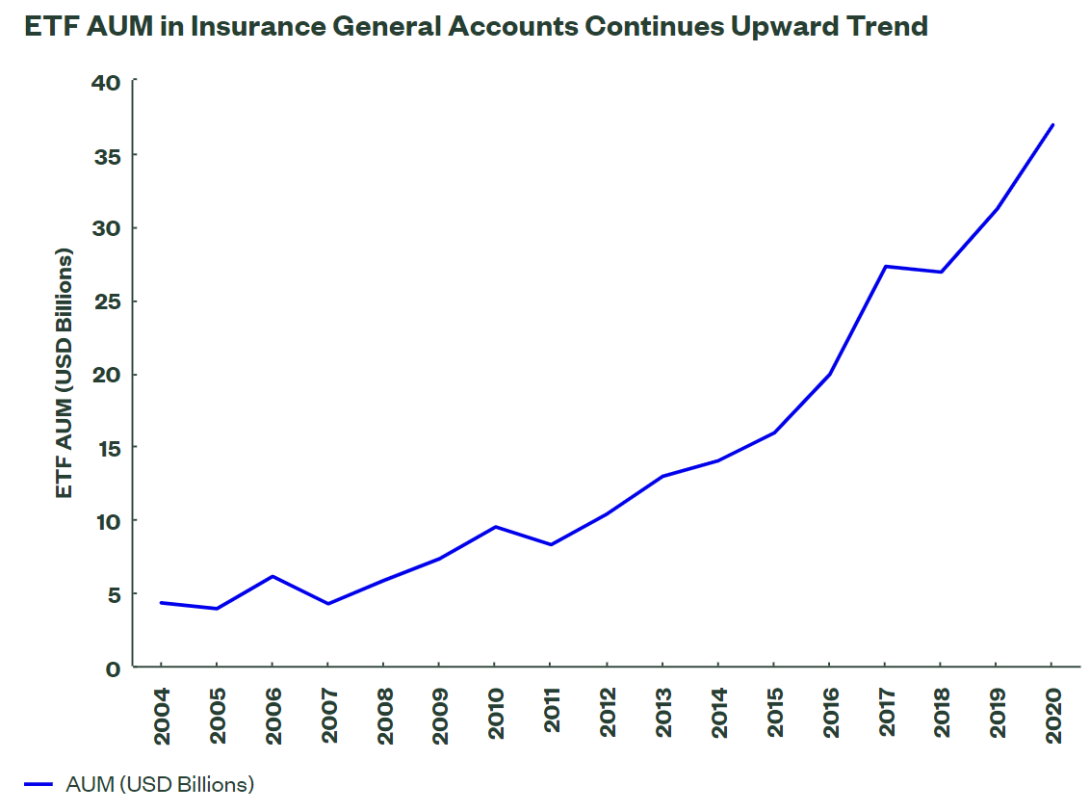

In 2020, US insurers increased their ETF AUM by 18% year-over-year to $36.9 billion.1

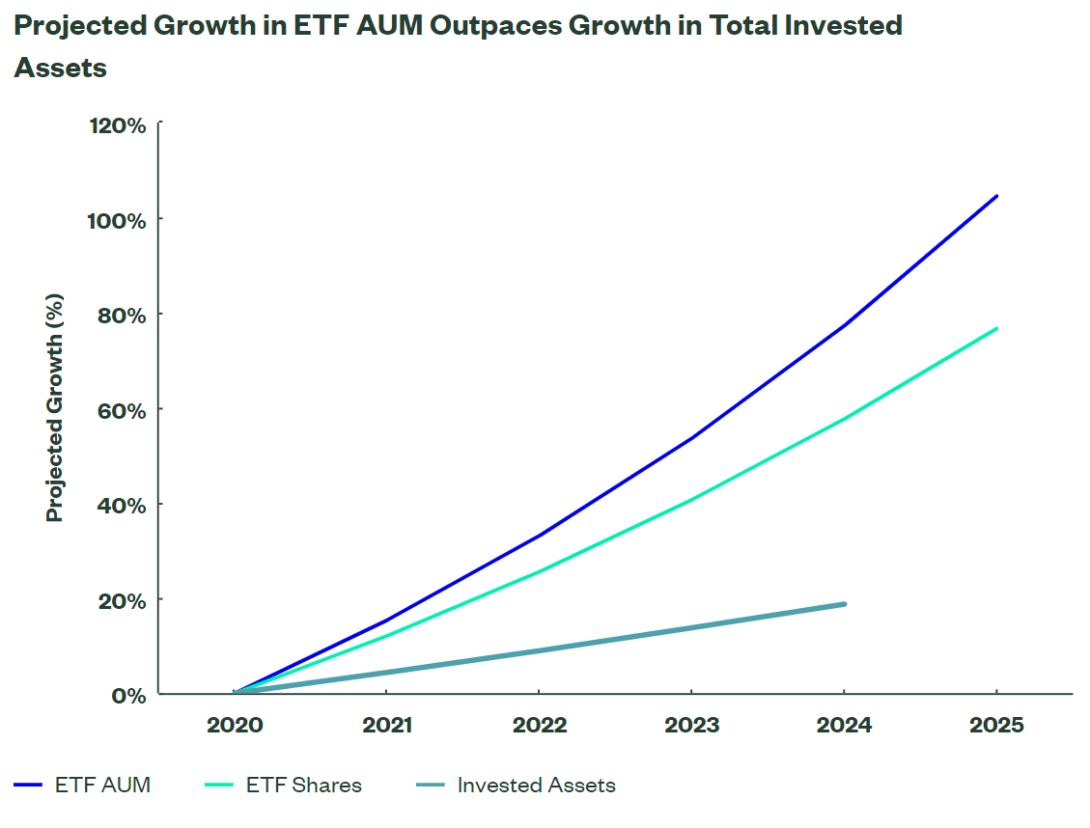

Growth in ETF usage by insurance general accounts is expected to substantially outpace growth of invested assets.

Insurers are using ETFs in a number of innovative applications, including reducing cash drag and building scale in subsidiary accounts.

Since the first US-listed ETF launched in 1993, ETF adoption by institutional investors has been growing steadily as entities around the world are widely embracing a new way of investing.

Insurance companies in particular are rapidly expanding their use of ETFs in general account portfolios, both in terms of AUM and innovative portfolio applications. ETFs are becoming a cornerstone component of many insurance general account portfolios — and the runway for future growth is robust. Here, we examine this important trend, drawing on recent research by S&P Global Market Intelligence.2

Key Drivers of ETF Adoption among Insurers Institutional investors are drawn to ETFs’ ability to lower costs, improve efficiency, and maximize the impact of asset allocation decisions. Additional benefits include the potential for enhanced liquidity, versatility, and pricing transparency.

Fixed income ETFs are a particularly fast-growing segment of the market and of specific interest to insurers. Traditionally, insurance companies have sourced fixed income securities from broker-dealers — but declines in broker-dealer inventories, increases in transaction costs for individual bonds, and a prolonged low interest rate environment have pushed insurers to identify other means to find fixed income investments. Regulatory developments are another supportive factor for broader use of fixed income ETFs by insurers.

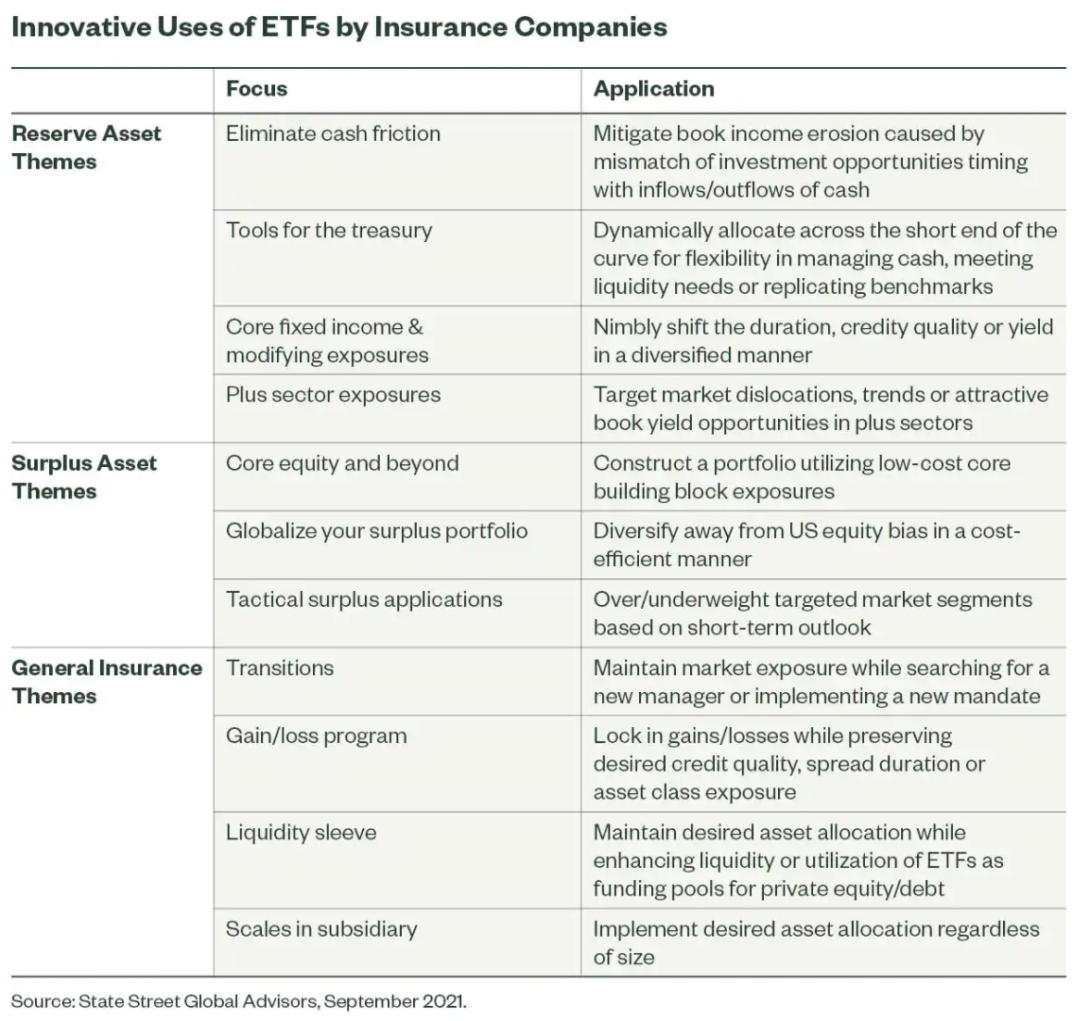

Real-World Applications: ETF Use Cases in Insurance General Accounts ETFs present a number of tactical and strategic applications for insurance general accounts.

Recent applications by our clients include:

Creating a liquidity sleeve – In Q2 2021, a large health insurer used multiple ETFs as a liquidity tool to build cash reserves in anticipation of higher-than-expected payouts due to the COVID-19 pandemic.

Building scale in a subsidiary – A mega life insurance company allocates to ETFs to build scale in subsidiary accounts, with a particular focus on fixed income ETFs.

Managing a tactical surplus – In March 2020, a medium Property & Casualty (P&C) insurer bought $120 million in a broad equity ETF when the market sold off, then sold its position in June 2020, netting a large gain.

By the Numbers: Insurance General Accounts Increasingly Adopt ETFs In a turbulent 2020, US insurers increased their ETF AUM by 18% year-over-year to $36.9 billion, keeping pace with the strong growth rate established in recent years. As a percentage of operating companies, the number of insurers using ETFs increased to a record 36%.

Source: ETFs in Insurance General Accounts – 2021, S&P Dow Jones Indices, as of December 31, 2020.

Although the amount invested in ETFs represents a small fraction of the $7.2 trillion in overall invested assets of US insurance companies, growth in ETF usage is expected to continue outpacing the growth of invested assets by a substantial margin. In fact, if insurance companies continue to invest according to the trend, their use of ETFs could almost double in the next five years — a mark already achieved between 2015 and 2019.

Source: Cerulli Associates and ETFs in Insurance General Accounts – 2021, S&P Dow Jones Indices, as of December 31, 2020.

Taking a closer look at the data from 2020, we note several key developments:

Company type – Life, health, and P&C firms all grew their ETF assets. Life insurers posted notable growth in their holdings, which increased almost 50% as the segment channeled $2.9 billion into ETFs. Much of this inflow was concentrated in fixed income ETFs.

Source: ETFs in Insurance General Accounts – 2021, S&P Dow Jones Indices, as of December 31, 2020.

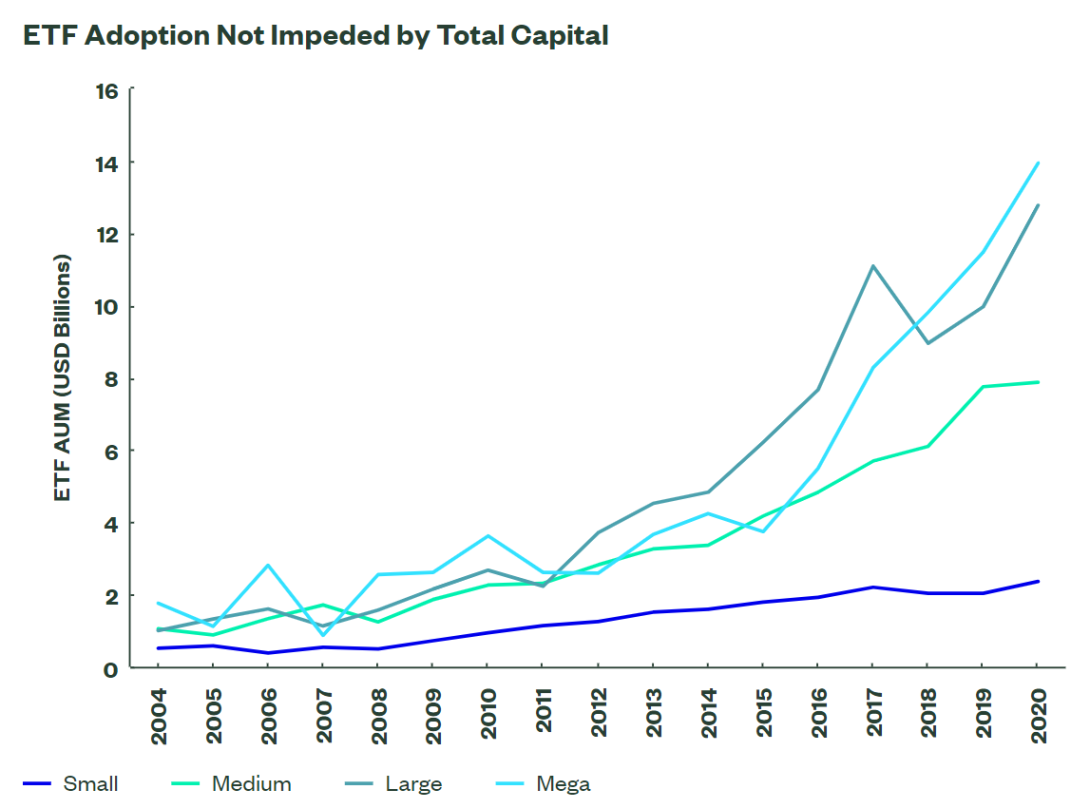

Company size – Mega companies owned most of the overall invested assets but held only about one-third of the ETF AUM. Since 2015, mega insurance companies have steadily increased their allocation to ETFs, boosting ETF AUM by 30% each year. While insurers of all sizes have increased their use of ETFs, medium-sized companies added the least in 2020.

Source: ETFs in Insurance General Accounts – 2021, S&P Dow Jones Indices, as of December 31, 2020.

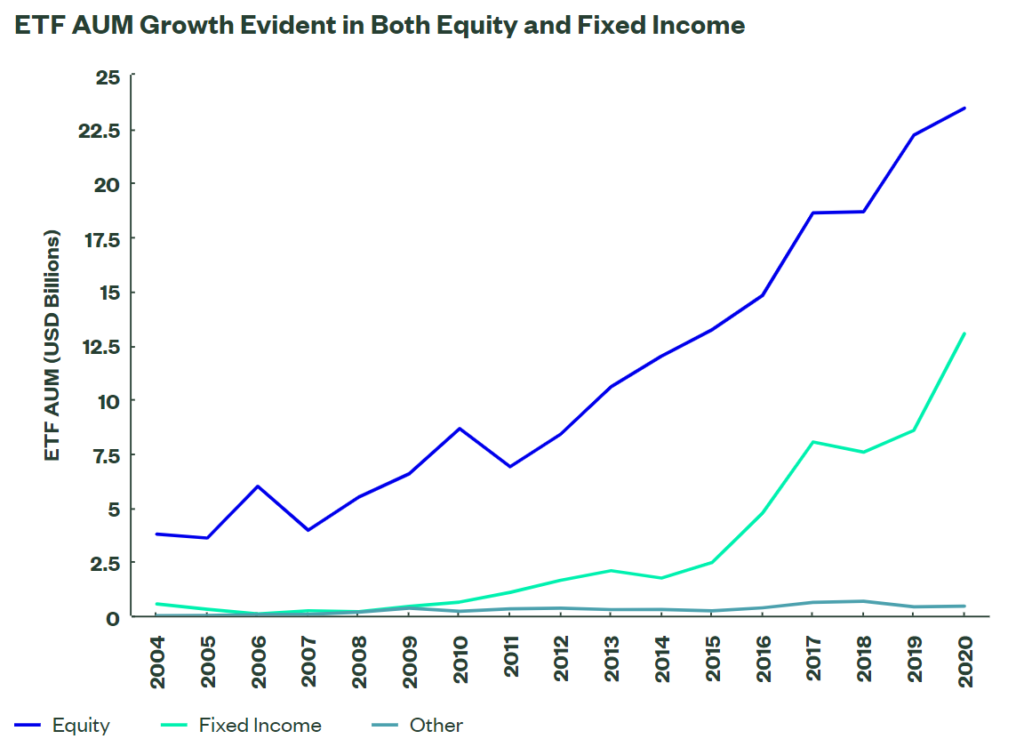

Asset class – Insurers funneled nearly $5 billion into fixed income ETFs, lifting the allocation to an all-time high of $13 billion and increasing AUM by 52%. Equity AUM increased by $1.2 billion.

Source: ETFs in Insurance General Accounts – 2021, S&P Dow Jones Indices, as of December 31, 2020.

As an ETF leader, our expertise has helped us build trusted partnerships with top insurance companies. You can see the full SPDR ETF line-up here, along with NAIC designations where applicable. To learn more about how we may be able to assist you and your clients, please reach out to the SPDR Insurance team, Benjamin Woloshin and Dewey Yoo.

This post was written with contributions from Dewey Yoo. Dewey is an Insurance ETF Business Development Representative on the SPDR Insurance team.

Unless otherwise noted, all data and statistical information were obtained from S&P Dow Jones Indices Research as of December 31, 2020.

The views expressed in this material are the views of SPDR Insurance Team through the period ended 10/18/2021 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

Because of their narrow focus, sector investing tends to be more volatile than investments that diversify across many sectors and companies.

There can be no assurance that a liquid market will be maintained for ETF shares

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor