Historically, the market has tended to misprice vacant or transitional properties while overpricing occupied real estate. COVID-19 related dislocations are causing valuations to become more attractive, and we expect occupancy trends to improve. That puts insurers in a unique position to provide liquidity to transitional real estate and capture a yield premium in a very capital-efficient strategy.

Download PDF

The Opportunity From COVID-19 Dislocations

Until the COVID-19 pandemic brought the world to a halt early in 2020, the US commercial real estate market had enjoyed several years of broad and steady improvement, aided by economic growth and historically low interest rates. Even during that stable period, lending access was still uneven nationwide—varying by the nature of the properties. With stricter regulations increasing the cost of capital, traditional lenders like banks and mortgage lenders have been restricting their activities to the highest-quality assets in select geographic locations.

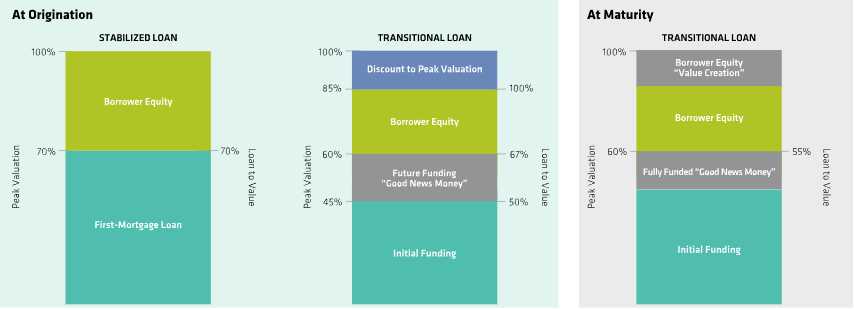

These trends have reduced available yields on loans secured by stable, core US properties. As traditional sources of debt capital have declined, value-added and opportunistic real estate investors want more capital—particularly for “transitional” properties, which are fundamentally sound but require value-added re-leasing, capital repositioning or repurposing. Transitional loans are structured to provide capital for potential “value creation” but are initially sized to assume none.

The supply and demand gap is being magnified by more than US$1 trillion of commercial real estate debt that’s due to mature by 2021 (a sizable portion of it originated before the global financial crisis). With much of this debt secured by transitional assets, a potentially robust pipeline of transitional lending opportunities is opening up, presenting alpha-generation opportunities for experienced managers as the US economy gradually works to reopen from COVID-19-related shutdowns.

After four months of government-mandated business closures, we expect occupancy trends to improve from the cyclical lows of pandemic-related dislocations. After a painful period of limited transaction volume and rapid distress for some property types (including hospitality, retail and/or borrowers that lack capital), volatility is declining and borrowers are once again looking to capital markets for debt financing.

Over the next several years, we see compelling risk-adjusted returns on unlevered first-mortgage whole loans secured by transitional or pre-stabilized assets (Display, next page)—thanks to lower property valuations, higher loan coupons, more moderate loan-to-value (LTV) ratios, and a growing preference for “lender friendlier” loan structures and covenants. Compared with stabilized lending strategies, the repositioning prevalent in transitional loans could mitigate risk through value creation.

“A potentially robust pipeline of transitional lending opportunities is opening up, presenting alpha-generation opportunities.”

Transitional Lending: Potential In Value Creation

As of June 30, 2020

For illustrative purposes. Historical analysis is not necessarily indicative of future results. There can be no assurances that comparable conditions will exist or that any investment objectives will be achieved.

Source: AB

Why Transitional Commercial Real Estate Debt?

Insurers searching for attractive risk-adjusted returns in commercial real estate are looking beyond the hypercompetitive core lending market. They’re considering moving further into the transitional lending segment, where demand for lending capital continues to outweigh supply—and where the benefits are highly attractive.

+ Enhanced Return Profile: Transitional loans are directly originated and highly customized to help borrowers drive value creation within the commercial real estate assets they own. That’s why yield spreads on transitional loans are often higher than those of comparable public credit investments. Transitional loans typically target unleveraged coupons of L+350-450bps, and, inclusive of other fees earned by the lender in connection with the loan (i.e. origination fees, exit fees, etc.) typically target overall gross yields of L+400-500bps.

+ Floating Rate Avoids USD Duration Risk: The risk of an inflation spike or sudden interest-rate increase is dramatically lower than it’s been in the past several years, but the floating-rate component of most transitional loans makes sense for non-USD insurers with liabilities in another currency that don’t want to take USD duration risk.

+ Capital-Charge Friendly: The required charges for transitional loans are modest under NAIC1 risk-based capital (RBC) and Solvency II. An average rating of roughly BBB is expected. Under Solvency II, these loans are likely to be unrated. However, the average maturity is short (around three years), leading to a fairly low capital charge under the standard formula. Insurers may be able to claim further capital relief for first-lien ranking and collateralization using their internal models. NAIC capital charges average to CM2 charge.

+ Accounting Benefits: Barring an event that materially affects collateral value, investments are held at cost. The performance of transitional loans is driven mainly by the returns of individual commercial real estate assets that are undergoing change as their owners implement value-added business plans. Because of this, transitional loans are less affected than public credit investments by broader changes in the market environment.

+ Lower Currency-Hedging Costs: For insurers in Europe and Asia (Japan and Korea, for example), the cost of hedging USD assets has dropped dramatically since the Federal Reserve cut its interest rate to practically zero. As a result, even after hedging, the substantial yield in commercial real estate is very compelling, compared with yields of similar credit-quality assets in domestic public markets.

+ Risk Reduction: Transitional loans are intended to provide capital for potential value creation, but they’re structured conservatively in case value creation is slow. As long as COVID-19 exists without a vaccine, property values in more urban markets will likely be depressed, which calls for more conservative lending standards with more moderate LTVs and stronger covenants in lenders’ favor.

AB’s Investment Strategy

AllianceBernstein’s (AB) Commercial Real Estate Debt team seeks to capitalize on the opportunity to generate attractive risk-adjusted returns in US real estate debt markets by originating unlevered, floating-rate, first-mortgage loans secured by high-quality, pre-stabilized real estate assets not ready for long-term, fixed-rate financing.

Pre-stabilized, or transitional, loans are extended primarily to institutional owners and secured by assets to be upgraded, repositioned or simply leased up. We expect this segment of the market to be underserved by the lending community as long as significant disruptions from COVID-19 remain.

The team structures loans with significant reserves, attractive prepayment terms and interest-rate protection. Borrowers also get the flexibility they need to execute their business plans—something traditional lenders are increasingly unable or unwilling to do. The team is opportunistic in identifying off-market and competitively advantageous deals.

Unlevered Structure: A Key Competitive Advantage

AB’s unlevered structure is particularly advantageous in times of market volatility and distress. Fully 100% of our loans are held exclusively on an unlevered basis, in contrast to nearly all of our main competitors in transitional lending.

This enables us to navigate the current market climate more efficiently, with complete control over loan negotiations and workouts. Because we don’t rely on leverage, we can also build stronger relationships directly with sponsors and borrowers, an advantage versus involving a third party that may have its own financial interests.

Disciplined, Multi-Step Investment Process

About The Portfolio Team

In 2012, AB created the Commercial Real Estate Debt (CRED) team. Led by Chief Investment Officer Peter Gordon, the 12-person team is responsible for commingled commercial mortgage funds and separate accounts totaling US$5.8 billion (as of June 30, 2020) for global institutions—mainly insurance companies. Its expertise spans deal sourcing/execution, portfolio management and operations, and the senior leaders average 23 years of real estate experience through various market cycles.

The CRED team draws on AB’s robust global infrastructure and the firm’s established public and private credit franchises throughout its operational and investment processes. The team also benefits from the knowledge and oversight of its investment committee, which includes individuals from across AB. This approach creates a forum through which AB’s global perspectives can inform the team’s investment efforts.

Summary

With interest rates at historical lows and central banks buying corporate bonds in public markets, insurers are being forced to rethink the structure of their credit portfolios. Many have expanded into private credit, but they haven’t yet explored the full range of options. Given this environment, it makes sense to look at less crowded segments for opportunities to provide market liquidity, such as transitional commercial real estate loans. These investments have attractive economic, risk and accounting features, which makes them a good complement to a traditional bond or whole loan allocation. Transitional loans’ yield premiums are much higher than public investment-grade opportunities, and they’re more capital-efficient than high-yield allocations.

Why AB For Commercial Real Estate Debt?

Independent Teams

+ Boutique-like focus and specialization with an independent credit process

+ Access to economic and industry research through AB’s broad fixed-income system

Independent Teams

+ US$272 billion global fixed-income platform as of March 31, 2020

+ Global public credit franchise and network of industry partners

Independent Teams

+ Business and Product Development

+ Operations

+ Legal and Compliance

+ Investor Relations

1 National Association of Insurance Commissioners

Note to All Readers: The information contained herein reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed herein may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AllianceBernstein Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AllianceBernstein Institutional Investments nor AllianceBernstein L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA–Reference Number 147956). Note to Austrian and German Readers: This information is issued in Germany and Austria by AB Europe GmbH. Note to Swiss Readers: This document is issued by AllianceBernstein Schweiz AG, Zürich, a company registered in Switzerland under company number CHE-306.220.501. AllianceBernstein Schweiz AG is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA) as a distributor of collective investment schemes. Swiss Representative & Swiss Paying Agent: BNP Paribas Securities Services, Paris, succursale de Zürich. Registered office: Selnaustrasse 16, 8002 Zürich, Switzerland, which is also the place of performance and the place of jurisdiction for any litigation in relation to the distribution of shares in Switzerland. The Prospectus, the key investor information documents, the Articles or management regulations, and the annual and semiannual reports of the concerned fund may be requested without cost at the offices of the Swiss representative. Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). The information in this document is intended only for persons who qualify as “wholesale clients,” as defined in the Corporations Act 2001 (Cth of Australia), and should not be construed as advice. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely the informational purposes and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information contained herein reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2020 AllianceBernstein L.P.