Italy's Bank Tax: It's Hard to Please Everyone All of the Time

The Italian government’s unexpected announcement earlier this month of a 40% one-off tax on local banks’ domestic excess profits prompted a negative market reaction. Although the selloff was enough for Italy’s finance ministry to scale back the tax the next day, the muddled episode provides another reminder of how heightened political polarization can impact investors.1

In its wake, the situation raises doubts in investors’ minds about the Italian government’s market friendliness and about Italian banks’ vulnerability to future political meddling.

An Unexpected Surprise…

Italian banks are doing well. We expect the two leading Italian banks’ domestic net interest income, the largest component of their profits, to grow 79% in 2023, compared to 2021. As a result, however, politicians and customers have accused the banks of excessively profiting from rising ECB rates and of passing on too little of those increases to savers.

Nevertheless, this month’s windfall tax surprised banks and investors. Deputy Prime Minister Salvini announced it in a speech on August 7, without the finance minister present and with little detail on how the government would calculate the tax. Italian bank spreads underperformed, and investors’ initial reaction wiped over €10 billion off Italian banks’ combined market cap. This loss far exceeded the €2-€3 billion that the government hoped to raise.

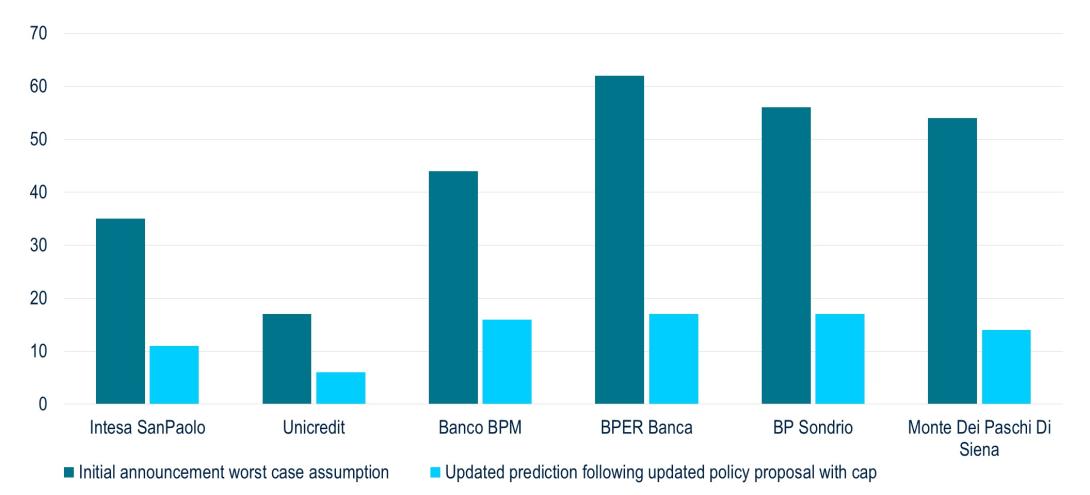

So, one day after it announced the bank tax, the government hastily capped it at 0.1% of each bank’s assets. After the cap, the impact on Italy’s banks would be less than half what investors initially feared (Figure 1), and share prices recovered around 60% of the initial selloff.

Figure 1: Italy’s larger banks should weather the revised tax better than their smaller peers. (impact of bank levy as % of predicted 2024 group net income)

Source: PGIM Fixed Income. The worst-case assumption is based on the tax applying to both 2021 (net interest income growth above 3%) and 2022 (net interest income growth above 6%) using 2020 as a base year, with a 40% tax applied. In the updated proposal, the thresholds are higher and only the higher number from 2021 and 2022 would apply. The cap of 0.1% of assets is introduced (which is the binding limit for all banks above). In all cases the “excess profit” calculation is based on domestic income. For the asset cap, this is based on the Italian parent company (a smaller perimeter than the group), but the income hit is shown against group net profit. For informational purposes only. Projections are not guaranteed, and actual results may vary.

…More Damaging Than Necessary

Our estimate of the sector-wide impact of the revised tax now lines up with the €2-€3 billion that the government was aiming for. This is a number that Italy’s banking sector can easily absorb.

The country’s big banks, in particular, are set for record profits this year—admittedly, after years of poor performance—and have been returning capital to shareholders. For the largest domestic banks, Intesa Sanpaolo and Unicredit, we calculate hits of 11% and 6% of expected 2024 net income, respectively (the tax only applies to domestic operations, so Unicredit fares better because it is more internationally diversified).

Smaller banks, with generally poorer profitability and less efficient balance sheets, see a proportionally larger hit. But even for them, this tax is a minor setback as their credit profiles have improved in recent years.

Windfall taxes aren’t unique to Italy, and they don’t have to elicit market routs. Spain’s bank tax, introduced in July 2022, led to a similarly negative initial reaction. But Spanish banks did not see a permanent risk premium, partly because their underlying earnings continued to improve, which outweighed the tax.

Italy’s tax, on the other hand, comes as banks’ margins look to be at cyclical highs, as the ECB rate cycle peaks. Moreover, the nature of Italy’s surprise announcements, with few details and poor communication, disquieted investors.

Prime Minister Meloni belatedly took “full responsibility” and said that she stands behind the tax. She has worked to portray herself as business-friendly but has damaged those ambitions with this measure. Italy’s parliament is yet to approve the tax and could alter it again, as even some of Meloni’s own government coalition support scaling it back.

This tax reminds investors that banks’ performance can depend on politics as much as on financial fundamentals. As a result, the latest episode may complicate one of the government’s other aims, to sell its stake in bailed-out bank Monte dei Paschi di Siena.

A Broader View: Macroeconomics and Italy’s Fiscal Policy

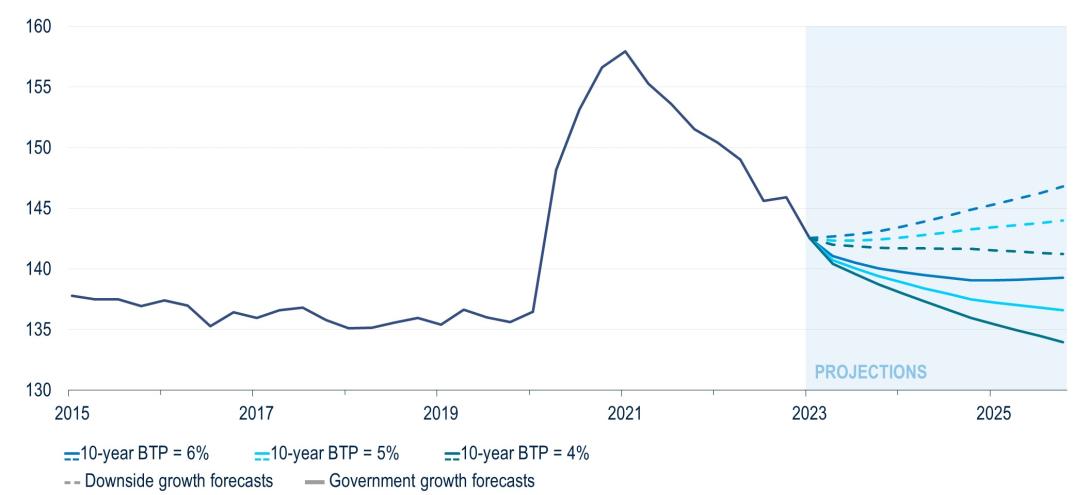

Last year, we expressed our near-term confidence in Italy’s political, economic, and fiscal outlook (Italy: Europe’s “Sleeping Beauty”). At the time, we did not think that the ECB's impending rate hikes would lead to significantly wider Italian bond spreads.

That earlier view has aged well. Our analysis last year suggested that a decline in Italy’s debt-to-GDP ratio was all but certain, and that high nominal GDP growth would more than offset the effect of rising interest rates. Since then, upside surprises to inflation have lowered Italy’s debt-to-GDP ratio even more rapidly than we had expected. Figure 2 shows that, if the yield on Italy’s 10-year sovereign bond (BTP) stays around today’s levels of 4%, the country needs annual nominal GDP growth of at least 2.5% to bring down the debt-to-GDP ratio.

Figure 2: The reduction in Italy’s debt-to-GDP ratio may be short-lived. (Italy debt-to-GDP ratio, %)

Note: BTP are Italian government bonds (“Buoni del Tesoro Poliennali”). The solid line in Figure 2 is the debt-to-GDP ratio, at a given yield, given the government's GDP forecast. The dashed line is the debt-to-GDP ratio, at a given yield, given a downside growth forecast. Source: PGIM Fixed Income, Macrobond, and Italian MEF.

But external factors now make Italy’s key deliverable—growth—more of a challenge (Figure 2). This raises concerns about debt sustainability. The ECB’s response to high inflation has tightened European financial conditions more than investors expected this time last year. Italy’s manufacturing-based economy already suffers from tight energy supply, and China’s underwhelming recovery is an additional headwind.

With inflation on its way down and the growth outlook weak, government policy will face greater investor scrutiny. This bank tax sent the wrong signal.

So how did it come to this? Since being elected, Meloni has largely remained true to her pledge to be a “safe pair of hands” on public finances. For example, her government wound up energy subsidies more rapidly than Italy’s European neighbors. And it mostly scrapped the “citizens’ income”—a popular and generous welfare program implemented by a previous government.

After some fiscally prudent, but unpopular, decisions, the tax on excess bank profits was intended to fund support for mortgage holders and tax cuts. Some saw it as a nod to Meloni’s populist origins, in an attempt to claw back political capital in her voter base.

This month’s bank tax may not be the last time we see a “Robin Hood” policy. And some will regard policies like these as symptoms of the global trend toward heightened political polarization, which may lead to reduced policy credibility. The Italian government now faces that credibility risk after learning a tough lesson: pleasing the electorate, the bond market, and shareholders at the same time is a tricky balancing act.

1 See our Q3 Outlook for more on the effects of loosening global macroeconomic anchors.

Read More From PGIM Fixed Income

This material reflects the views of the author as of August 15, 2023 and is provided for informational or educational purposes only. Source(s) of data (unless otherwise noted): PGIM Fixed Income. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. Past performance is not a guarantee or a reliable indicator of future results.

Source(s) of data (unless otherwise noted): PGIM Fixed Income, as August 25, 2023.

Notice: Important Disclosures

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iii) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”); (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) PGIM Netherlands B.V., located in Amsterdam (“PGIM Netherlands”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom, or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

Conflicts of Interest: PGIM Fixed Income and its affiliates may have investment advisory or other business relationships with the issuers of securities referenced herein. PGIM Fixed Income and its affiliates, officers, directors and employees may from time to time have long or short positions in and buy or sell securities or financial instruments referenced herein. PGIM Fixed Income and its affiliates may develop and publish research that is independent of, and different than, the recommendations contained herein. PGIM Fixed Income’s personnel other than the author(s), such as sales, marketing and trading personnel, may provide oral or written market commentary or ideas to PGIM Fixed Income’s clients or prospects or proprietary investment ideas that differ from the views expressed herein. Additional information regarding actual and potential conflicts of interest is available in Part 2A of PGIM Fixed Income’s Form ADV.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorized and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area(“EEA”), information is issued by PGIM Netherlands B.V., an entity authorized by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In South Africa, PGIM, Inc. is an authorized financial services provider –FSP number 49012. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you of that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 -Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

All investments involve risk, including the possible loss of capital.

These materials are for informational or educational purposes. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. Clients seeking information regarding their particular investment needs should contact their financial professional.

This document may contain confidential information and the recipient hereof agrees to maintain the confidentiality of such information. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of this document, in whole or in part, or the divulgence of any of its contents, without PGIM Fixed Income’s prior written consent, is prohibited. This document contains the current opinions of the manager and such opinions are subject to change. Certain information in this document has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all such information; nor do we make any express or implied warranties or representations as to its completeness or accuracy. Any information presented regarding the affiliates of PGIM Fixed Income is presented purely to facilitate an organizational overview and is not a solicitation on behalf of any affiliate. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services. These materials do not constitute investment advice and should not be used as the basis for any investment decision.

This material may contain examples of the firm’s internal ESG research program and is not intended to represent any particular product’s or strategy’s performance or how any particular product or strategy will be invested or allocated at any particular time. PGIM’s ESG processes, rankings and factors may change over time. ESG investing is qualitative and subjective by nature; there is no guarantee that the criteria used or judgment exercised by PGIM Fixed Income will reflect the beliefs or values of any investor. Information regarding ESG practices is obtained through third-party reporting, which may not be accurate or complete, and PGIM Fixed Income depends on this information to evaluate a company’s commitment to, or implementation of, ESG practices. ESG norms differ by region. There is no assurance that PGIM Fixed Income’s ESG investing techniques will be successful.

These materials do not take into account individual client circumstances, objectives or needs. No determination has been made regarding the suitability of any securities, financial instruments or strategies for particular clients or prospects. The information contained herein is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. Any discussion of risk management is intended to describe PGIM Fixed Income’s efforts to monitor and manage risk but does not imply low risk. No risk management technique can guarantee the mitigation or elimination of risk in any market environment. These materials do not purport to provide any legal, tax or accounting advice. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation.

Any references to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Any securities referenced may or may not be held in portfolios managed by PGIM Fixed Income and, if such securities are held, no representation is being made that such securities will continue to be held.

Any financial indices referenced herein as benchmarks are provided for informational purposes only. The use of benchmarks has limitations because portfolio holdings and characteristics will differ from those of the benchmark(s), and such differences may be material. You cannot make a direct investment in an index. Factors affecting portfolio performance that do not affect benchmark performance may include portfolio rebalancing, the timing of cash flows, credit quality, diversification and differences in volatility. In addition, financial indices do not reflect the impact of fees, applicable taxes or trading costs which reduce returns. Unless otherwise noted, financial indices assume reinvestment of dividends.

Any projections or forecasts presented herein are as of the date of this presentation and are subject to change without notice. Actual data will vary and may not be reflected here. Projections and forecasts are subject to high levels of uncertainty. Accordingly, any projections or forecasts should be viewed as merely representative of a broad range of possible outcomes. Projections or forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. PGIM Fixed Income has no obligation to provide updates or changes to any projections or forecasts.

Any performance targets contained herein are subject to revision by PGIM Fixed Income and are provided solely as a guide to current expectations. There can be no assurance that any product or strategy described herein will achieve any targets or that there will be any return of capital. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value.

© 2023 PFI and its related entities

2023-6410

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in