Looking to Latin America to Fuel the EU's Energy Transition

The European Union’s ambition to decarbonize at an accelerated pace has the bloc well-situated as a leader in the green transition.1 A steady and secure supply of Critical Raw Materials (CRMs) will be essential for the EU to meet its goals. But limited CRM supply, rising global demand, and geopolitical uncertainty, along with the EU’s dependence on single-country sources, presents a challenge. In Latin America, the EU has a potential partner that is mineral-rich, keen to make use of its resources, and looking to diversify its trading partners. Compared to Asia and Africa, closer pre-existing trade ties with the EU and a more developed mining sector make Latin America a logical priority. Deepening ties would provide a path to diversifying the EU’s CRM supply chain and support Latin American economies, both of which carry wide-ranging investment implications that influence our portfolio positioning over the medium to long term.

The EU’s Decarbonization Ambitions

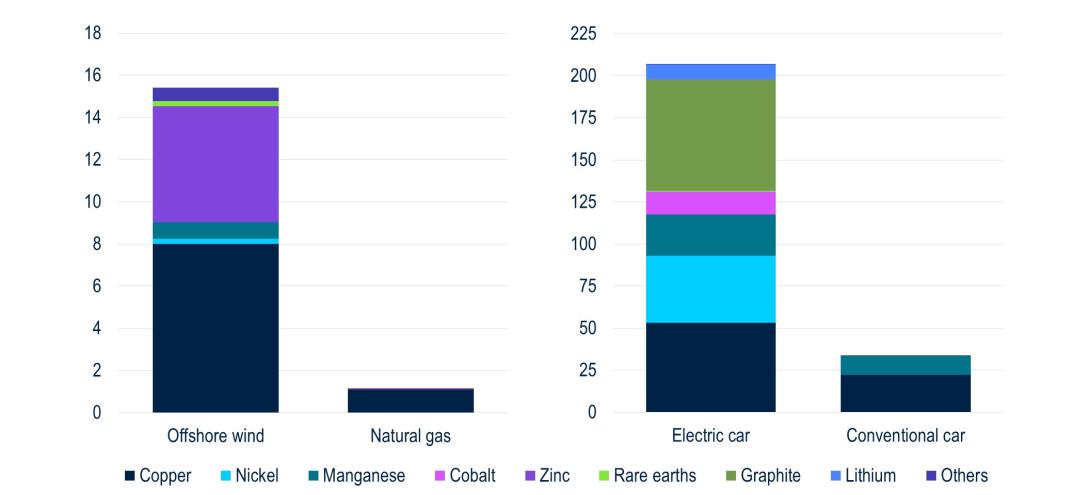

The EU’s Recovery and Resilience Facility (RRF) and the climate law ”Fit for 55” encourage and mandate significant investments in green technologies. For example, the Netherlands is the EU’s largest producer of natural gas but has been cutting production over the past decade and is now using funds from the RRF to make large investments in offshore wind energy. Under Fit for 55, the EU has effectively banned the sale of combustion engine vehicles from 2035, requiring all new cars sold to emit no CO2. Figure 1 shows that to make these kinds of structural changes, the EU’s manufacturing sector will need to source substantially more CRMs. Offshore wind requires far more copper, chromium, nickel, manganese, molybdenum, zinc, and rare earths than those required in natural gas production. The cars of the future will require more copper and manganese, as well as lithium, nickel, cobalt, and graphite.

Figure 1: Minerals Used in Clean Technologies Compared to Conventional Technologies (left panel: tonnes/MW; right panel: kg/vehicle)

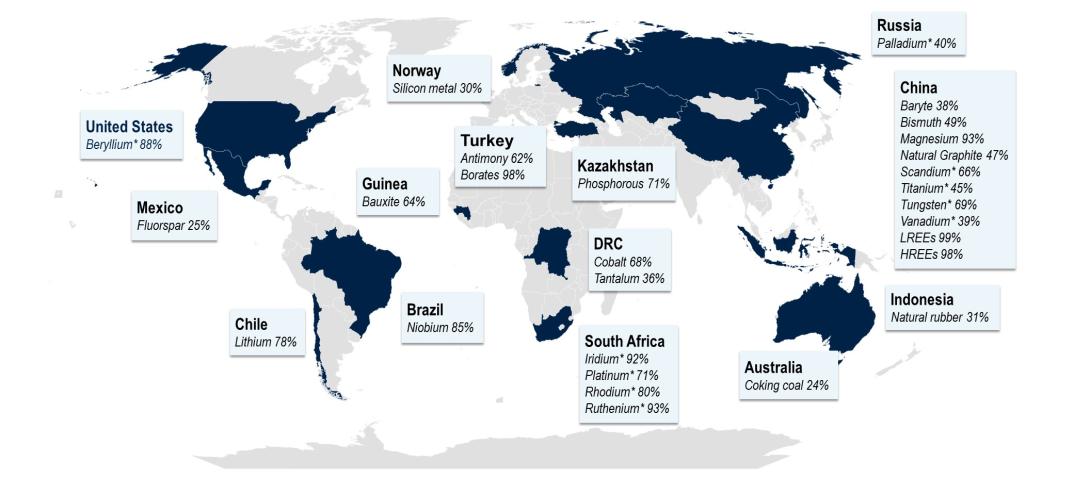

Source: IEA, May 5, 2021. Steel and aluminium not included. The values for vehicles are for the entire vehicle including batteries, motors and glider. The intensities for an electric car are based on a 75 kWh NMC (nickel manganese cobalt) 622 cathode and graphite-based anode. The values for offshore wind are based on the direct-drive permanent magnet synchronous generator system (including array cables) and the doubly-fed induction generator system respectively. The values for natural gas are based on ultra-supercritical plants and combined-cycle gas turbines. Actual consumption can vary by project depending on technology choice, project size and installation environment. The EU’s current supply of CRMs is highly concentrated. Figure 2 shows that 80% or more of the EU’s beryllium, lithium, niobium, magnesium, and rare earths (HREEs, LREEs) likely come from a single third country. But post-pandemic supply-chain disruptions, as well as renewed geopolitical tensions with two of its largest trading partners in Russia and China, reinforce the need for resilient, diversified supply chains that can provide a steady flow of raw materials. Policymakers themselves refer to a need to “reduce critical dependencies” and “diversify where appropriate.”2

Figure 2: Countries Accounting for Largest Share of EU Sources of CRMs (%)

Source: European Commission, March 2023. *Share of global production. With this in mind, the EU recently unveiled its Critical Raw Materials Act, which limits the sourcing of each strategic material from a single third country by 2030.3 As shown above, that is a big ask, and international engagement is vital. Another key element, which has also been discussed at the G7, is an explicit initiative to create a “CRM Club” of like-minded countries keen to strengthen CRM supply chains. And a commitment to joint procurement at the EU-level is an attempt to claw back bargaining power from producing countries.

CRMs in Latin America

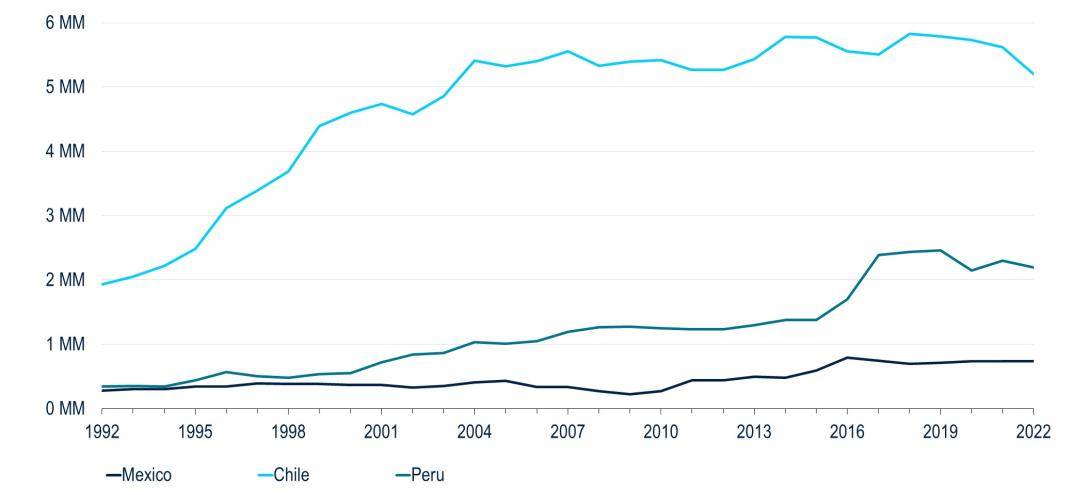

Of the critical minerals needed, Latin America is likely best suited to provide copper, lithium, graphite, and zinc. It does not produce cobalt, and it produces mostly class 2 nickel, which is less useful for technologies used in decarbonization activities. Copper is a key metal needed in several applications and copper market participants generally expect a significant shortfall in supply relative to demand beginning in a few years, with the expected supply of copper estimated to be only 80% of demand by 2030.4 Chile, Peru, and Mexico are particularly well positioned to benefit from this dynamic. The three countries together accounted for over 40% of global copper production in 2022 and have 36.5% of the world’s estimated copper reserves. However, output growth in those countries has stalled in recent years (Figure 3).

Figure 3: Latin American Copper Output Has Stalled Despite Large Reserves (metric tonnes)

Source: Macrobond, July 5, 2023. Latin America also has significant lithium reserves, but a large portion remains undeveloped. The region accounted for almost 37% of global 2022 production and currently accounts for more than 70% of estimated global reserves. Chile and Bolivia have the largest proven reserves (Figure 4), with significant room for expansion in both countries. Argentina, Brazil, and Mexico can also contribute to lithium production growth in the region, but to a lesser extent as their reserves are relatively small by comparison.

Figure 4: Global Lithium Reserve (metric tonnes)

Source: United States Geological Survey, January 2023. Graphite is present in both Brazil and Mexico, with Brazil having over 850 years of reserves at current production rates. The two countries represent only 6.7% of 2022 graphite production, but over 23% of global graphite reserves (mainly in Brazil). Zinc, which has applications in wind power, can also be sourced in a few Latin American countries. Bolivia, Mexico, and Peru provided almost 21% of the world’s zinc in 2022 and have at least 14% of global zinc reserves.

Source: United States Geological Survey, January 2023. Graphite is present in both Brazil and Mexico, with Brazil having over 850 years of reserves at current production rates. The two countries represent only 6.7% of 2022 graphite production, but over 23% of global graphite reserves (mainly in Brazil). Zinc, which has applications in wind power, can also be sourced in a few Latin American countries. Bolivia, Mexico, and Peru provided almost 21% of the world’s zinc in 2022 and have at least 14% of global zinc reserves.

A Value-Add Partner

Clearly Latin America can help the EU satisfy some of its CRM needs. That said, the EU will be competing with other large economic powers such as the U.S., China, Japan, and Korea. Paying more than another buyer is of course persuasive, but there are other ways in which the EU can compete for these minerals As Latin America seeks to move away from its “dig and ship” model of raw material production in favour of more value-added processes, the EU could help to develop the region’s processing capabilities. The EU could also offer technical, regulatory, environmental, and educational assistance, which would allow Latin America to advance its collective economy. The EU could also assist in the development of a recycling industry in Latin America as its economies advance. In many cases, social, political, and regulatory tensions have been holding back investment. With much of Latin America shifting toward populism and the development of new projects facing resistance from local communities, the EU could assist with environmental education and work with local regulators and mining companies to build credibility. This could facilitate faster mine development and, in turn, increased production of critical minerals. Another issue facing Latin American mining companies is the high tax rates placed on them by local governments.5 To offset this, the EU might offer low-cost financing to these governments to improve regulatory and environmental oversight, as well as fund much needed infrastructure such as hospitals, schools, and roads.

Models of Engagement

Of the 21 countries in Latin America, the EU has a trade agreement either in place or in the pipeline with 18 of them. But new deals or wide-ranging updates to existing ones can take decades. Instead, other models of engagement, such as Memorandums of Agreement (MoUs), or specific CRM amendments to existing agreements, may present a better opportunity. For example, the EU recently signed an MoU with Argentina on the development of sustainable raw material value chains. And a recent update of the EU-Chile trade deal has a dedicated chapter on CRMs, which amongst other things, allows EU companies to apply for exploration licences in Chile without discrimination, and commits to carrying out environmental impact assessments.

Investment Implications

As the transition to green technologies gathers momentum, CRMs are increasingly in high demand. However, supply is not expected to keep pace with burgeoning demand in the coming decade. This has wide-ranging implications for EU and Latin American economies alike. Closer regulatory alignment to the EU, the chance to move up the mining supply chain, and the potential benefits to GDP growth and currencies from a stronger current account could support long positioning in sovereign debt of certain Latin American countries, such as Chile and Peru. On the EU side, further ties with Latin America could help diversify supply chains away from China and provide an additional source of minerals critical to meeting its decarbonization goals. For certain metals, prices are likely to increase to unprecedented levels. This positive price action is necessary to bring out new supply as Latin American mining companies can develop CRM reserves more economically. Similarly, investments in the bonds of companies that produce these commodities could generate strong returns in the years to come. Ultimately, increased supply should alleviate pressure on these commodity prices, allowing for a more financially feasible global decarbonization plan. Special thanks to Francisco Campos-Ortiz and Katharine Neiss for their contributions on this piece. Read More From PGIM Fixed Income 1 IMF, “How to Meet the European Union’s Ambitious Climate Mitigation Goals,” September 24, 2020. 2. https://data.consilium.europa.eu/doc/document/ST-7-2023-INIT/en/pdf 3 European Commission, “Critical Raw Materials: Ensuring Secure and Sustainable Supply Chains for EU’s Green and Digital Future,” March 16, 2023. 4 IEA, “The Role of Critical Minerals in Clean Energy Transitions,” 2021. 5 S&P Global Market Intelligence, “Miners Ready to Cut Investment if Chile Raises Copper Tax,” August 18, 2022. Source(s) of data (unless otherwise noted): PGIM Fixed Income, as August 24, 2023. For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital. PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide. These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional. These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy. Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss. In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3. © 2023 PFI and its related entities. 2023-6261

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in