Source: US Energy Information Administration, February 2021. Although the first wave of venture and growth investing in clean tech (Clean Tech 1.0) still haunts some investors, technological evolution and supportive regulations have led many to reconsider the opportunity set in Clean Tech 2.0 (Climate Tech). In contrast to Clean Tech 1.0, in which venture and growth managers took on substantial technology risk, Climate Tech spans the risk spectrum, including a range of enabling technologies that support the inevitable transition to a greener economy, and some potentially game-changing technologies like green hydrogen and carbon capture, utilization and storage. Notably, this also includes asset-light businesses that seek to improve the emissions profiles of sectors that are the biggest emissions contributors. According to a PwC report, Climate Tech venture capital grew at nearly five times the rate of the overall global venture capital market between 2013 and 2019, increasing from $418 million in 2013 to $16.3 billion in 2019.9 StepStone sees this reflected in the growing number and size of funds focused on Climate Tech. Most have fallen under infrastructure, followed by growth equity and venture capital. Climate Tech-focused buyouts are still emerging as a strategy.

Source: US Energy Information Administration, February 2021. Although the first wave of venture and growth investing in clean tech (Clean Tech 1.0) still haunts some investors, technological evolution and supportive regulations have led many to reconsider the opportunity set in Clean Tech 2.0 (Climate Tech). In contrast to Clean Tech 1.0, in which venture and growth managers took on substantial technology risk, Climate Tech spans the risk spectrum, including a range of enabling technologies that support the inevitable transition to a greener economy, and some potentially game-changing technologies like green hydrogen and carbon capture, utilization and storage. Notably, this also includes asset-light businesses that seek to improve the emissions profiles of sectors that are the biggest emissions contributors. According to a PwC report, Climate Tech venture capital grew at nearly five times the rate of the overall global venture capital market between 2013 and 2019, increasing from $418 million in 2013 to $16.3 billion in 2019.9 StepStone sees this reflected in the growing number and size of funds focused on Climate Tech. Most have fallen under infrastructure, followed by growth equity and venture capital. Climate Tech-focused buyouts are still emerging as a strategy.

On the impact side, the SDGs provide a framework for investors to align their impact objectives with critical global problems. The Impact Management Project (IMP) and the IFC’s Operating Principles for Impact Management (OPIM) have created frameworks for evaluating and benchmarking impact management processes, thereby building on the decades of impact experience and codifying it for broader adoption (Figure 9). A critical additional dimension for impact investments over ESG is the need to track and measure outcomes. As the universe matures, investors are seeking greater standardization of metrics. The IRIS+ catalog of impact metrics was developed to address this issue. On climate, the TCFD encourages asset owners to disclose a variety of metrics, including the effect of hypothetical climate change scenarios on their portfolios. StepStone has intentionally aligned its approach with these frameworks: We believe standardization reduces compliance costs and enables us to collect more usable data. As such, we urge other asset allocators to align with peak bodies, rather than reinvent the wheel. EXIT MARKETS With more companies and countries making climate commitments, and technological advancements making several business models more sustainable, corporate buyers, alternative investment funds and public investment vehicles have become increasingly interested in these sectors. One sign of investors’ growing appetite for green ventures is the flurry of special purpose acquisition companies that went public last year, many of which are looking for the “next big thing” in clean energy. According to one report, last year more than a dozen such firms raised more than $5 billion. Many were backed by traditional oil and gas investors who are keen to be at the forefront of the energy evolution.14 Beyond Meat’s 2019 IPO and Oatly’s 2021 IPO also underscore the appetite for plant-based food companies, drawing the interest of a number of traditional venture and growth equity investors. This trend highlights some important shifts.

On the impact side, the SDGs provide a framework for investors to align their impact objectives with critical global problems. The Impact Management Project (IMP) and the IFC’s Operating Principles for Impact Management (OPIM) have created frameworks for evaluating and benchmarking impact management processes, thereby building on the decades of impact experience and codifying it for broader adoption (Figure 9). A critical additional dimension for impact investments over ESG is the need to track and measure outcomes. As the universe matures, investors are seeking greater standardization of metrics. The IRIS+ catalog of impact metrics was developed to address this issue. On climate, the TCFD encourages asset owners to disclose a variety of metrics, including the effect of hypothetical climate change scenarios on their portfolios. StepStone has intentionally aligned its approach with these frameworks: We believe standardization reduces compliance costs and enables us to collect more usable data. As such, we urge other asset allocators to align with peak bodies, rather than reinvent the wheel. EXIT MARKETS With more companies and countries making climate commitments, and technological advancements making several business models more sustainable, corporate buyers, alternative investment funds and public investment vehicles have become increasingly interested in these sectors. One sign of investors’ growing appetite for green ventures is the flurry of special purpose acquisition companies that went public last year, many of which are looking for the “next big thing” in clean energy. According to one report, last year more than a dozen such firms raised more than $5 billion. Many were backed by traditional oil and gas investors who are keen to be at the forefront of the energy evolution.14 Beyond Meat’s 2019 IPO and Oatly’s 2021 IPO also underscore the appetite for plant-based food companies, drawing the interest of a number of traditional venture and growth equity investors. This trend highlights some important shifts.

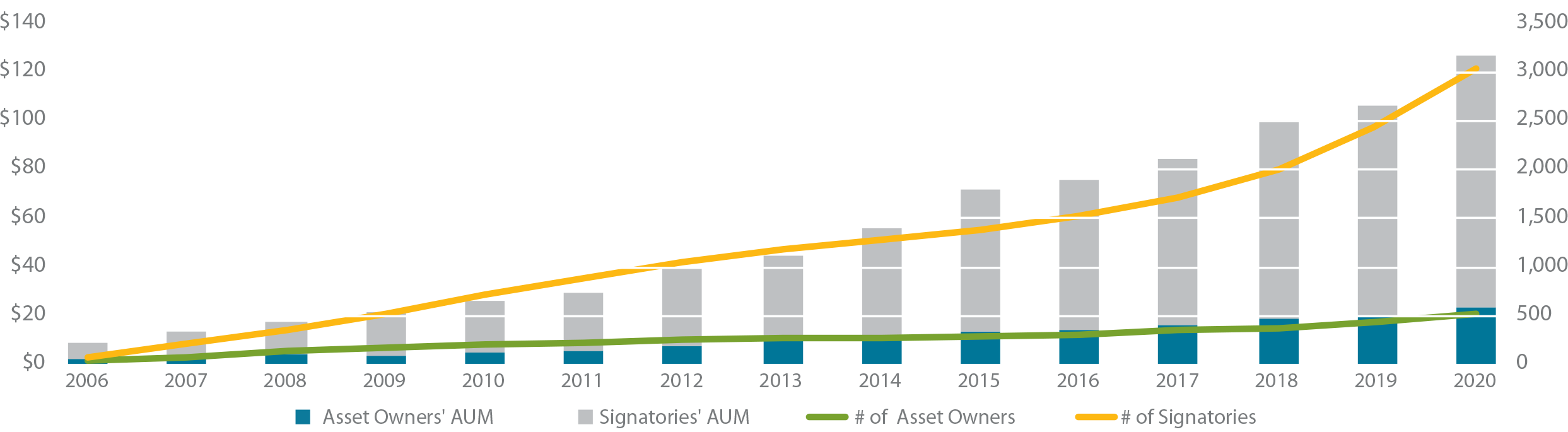

Source: Global Impact Investing Network, 2020; StepStone Group analysis.

Source: Global Impact Investing Network, 2020; StepStone Group analysis. StepStone Group

StepStone Group (Nasdaq: STEP) is a global private markets investment firm focused on providing customized investment solutions and advisory and data services to our clients. StepStone’s clients include some of the world’s largest public and private defined benefit and defined contribution pension funds, sovereign wealth funds and insurance companies, as well as prominent endowments, foundations, family offices and private wealth clients, which include high-net-worth and mass affluent individuals. StepStone partners with its clients to develop and build private markets portfolios designed to meet their specific objectives across the private equity, infrastructure, private debt and real estate asset classes.

W. Casey Gildea

Managing Director casey.gildea@stepstonegroup.com

+1.212.351.6114

277 Park Ave, 45th Floor

New York, NY 10172