The most sustainable emerging market companies are on par with those in developed markets. Our emerging market quant equity approach is designed to benefit from these businesses.

Speed read

- Emerging markets have tremendous growth potential in sustainability

- Sustainable emerging market companies are as ‘green’ as those in developed markets

- Our sustainable emerging market equity strategy targets this opportunity

Sustainable investing in emerging markets is considered challenging because of the belief that these markets generally have weaker environmental, social and governance characteristics than developed ones. By applying a range of metrics, we show that the most sustainable companies in emerging markets are on par with those in developed markets.

With wider data coverage and better data quality, emerging markets present a significant opportunity potential for sustainable investors. Using Robeco’s quant approach, we look to benefit from this opportunity by identifying what we believe to be the right companies and construct tailor-made solutions that meet investors’ financial and sustainability objectives.1

A sustainable growth opportunity

Emerging markets offer significant growth potential in the realm of sustainability. This new reality is set by the example of countries such as China and India, who have started playing a leading role in the clean energy transition.

For example, China now supplies 75% of the world’s solar panels, and India was the first country to set extensive standards for light-emitting diodes (LEDs), which is expected to save around 277 terawatt-hours of electricity between 2015 and 2030 – the equivalent of about 10% of Europe’s total carbon emissions in 2020. Significantly, Asia-Pacific is the region with the largest and highest growth of investment in low-carbon energy sources.

Despite this tremendous opportunity, sustainable investing in emerging markets poses unique challenges, with concerns about the lack of oversight and regulatory standardization across jurisdictions, and the view that emerging markets are lagging in terms of sustainability.

As active investors, we see the varied nature of the emerging market sustainability landscape as an excellent opportunity to create highly sustainable emerging market portfolios. The key question is: how do we find such well-positioned and sustainable companies in emerging markets?

The quest to find the most sustainable companies in emerging markets

This challenging task calls for a data-driven selection approach, which has the advantage of broad coverage. The ultimate goal is to build a portfolio that meets specific constraints and demands with respect to sustainability characteristics. Our approach is to cover multiple sustainability angles and measures, including ESG risks, environmental footprint, water consumption, waste management, and the company’s contribution to the SDGs.

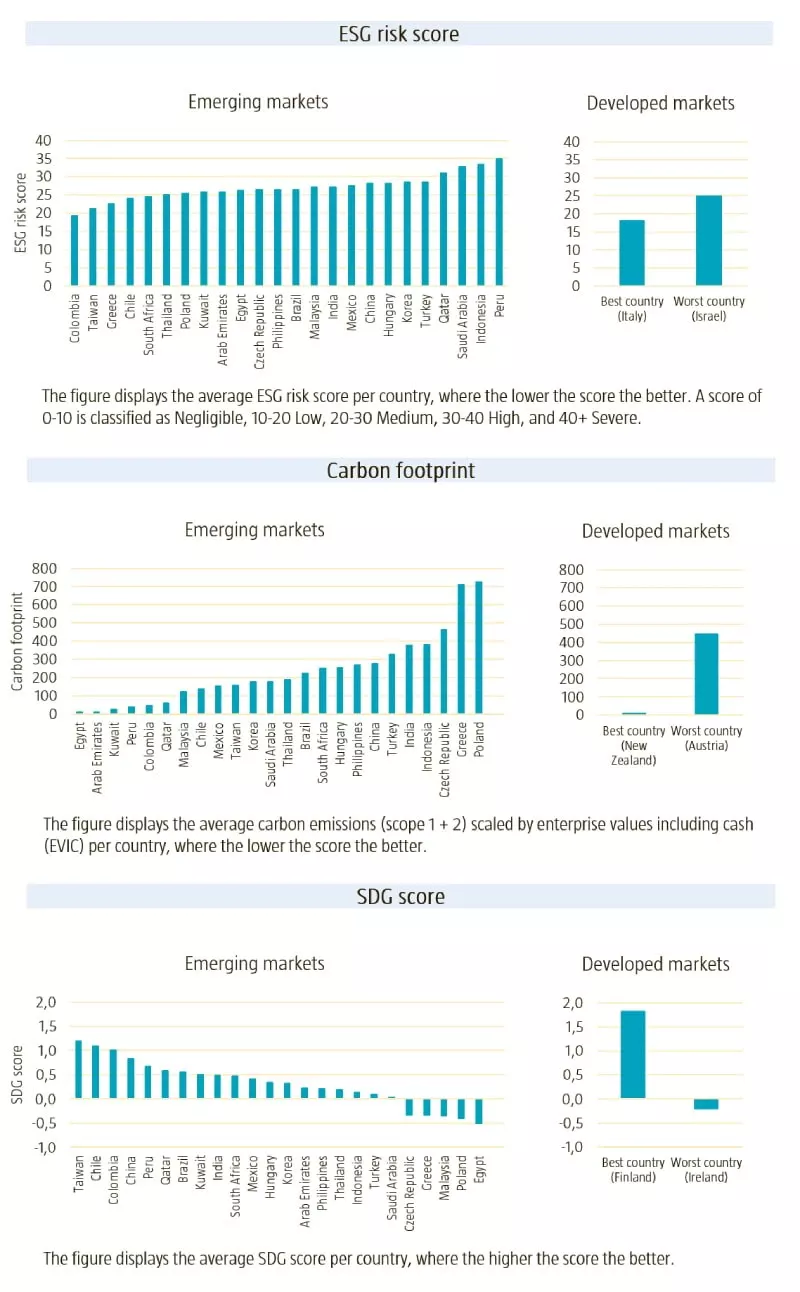

Our sustainability assessment is done at a country and at a stock level. Figure 1 shows the average sustainability scores (ESG risk score, carbon footprint and SDG score) of benchmark constituents in each individual country and the comparison with the best and worst-scoring country in developed markets.

We observe that the worst-performing country in developed markets is in general still doing better than the worst one in emerging markets, while – aside from SDG scores – the best countries in developed markets and emerging markets on average perform equally well. For example, the country with the highest ESG risk in developed markets is Israel, with a score of 25, while Peru in emerging markets has a score of 35. At the other end of the scale, the country with the lowest ESG risk in emerging markets is Colombia with a score of 19, while in developed markets it is Italy with a score of 18.

Figure 1 | Country dispersion of sustainability scores in emerging markets versus developed markets

Source: Sustainalytics, Trucost, Robeco. The universe consists of constituents of the MSCI World and MSCI Emerging Markets indices. Data as of March 2022.

Additionally, we observe that there are not many countries that perform exceptionally well or poorly on all three measures. For instance, Peru receives a poor score on ESG but has a low carbon footprint and a top-quartile SDG score. Similarly, Egypt has a low carbon footprint but does not perform very well in terms of SDG.

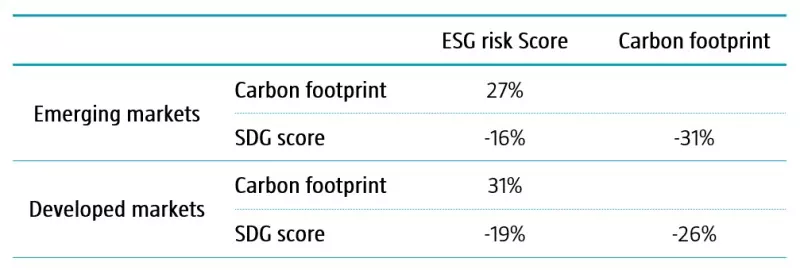

This finding highlights the fact that there are low correlations among these three measures (ranging between -30% and +30%), as shown in Figure 2. These results emphasize the importance of a multi-dimensional approach to sustainability, which takes different aspects into account when constructing portfolios.

Figure 2 | Correlation across different sustainability measures

Source: Sustainalytics, Trucost, Robeco. Displayed are the rank correlations of each individual stock’s score. Data as of March 2022.

Sustainability of emerging market stocks

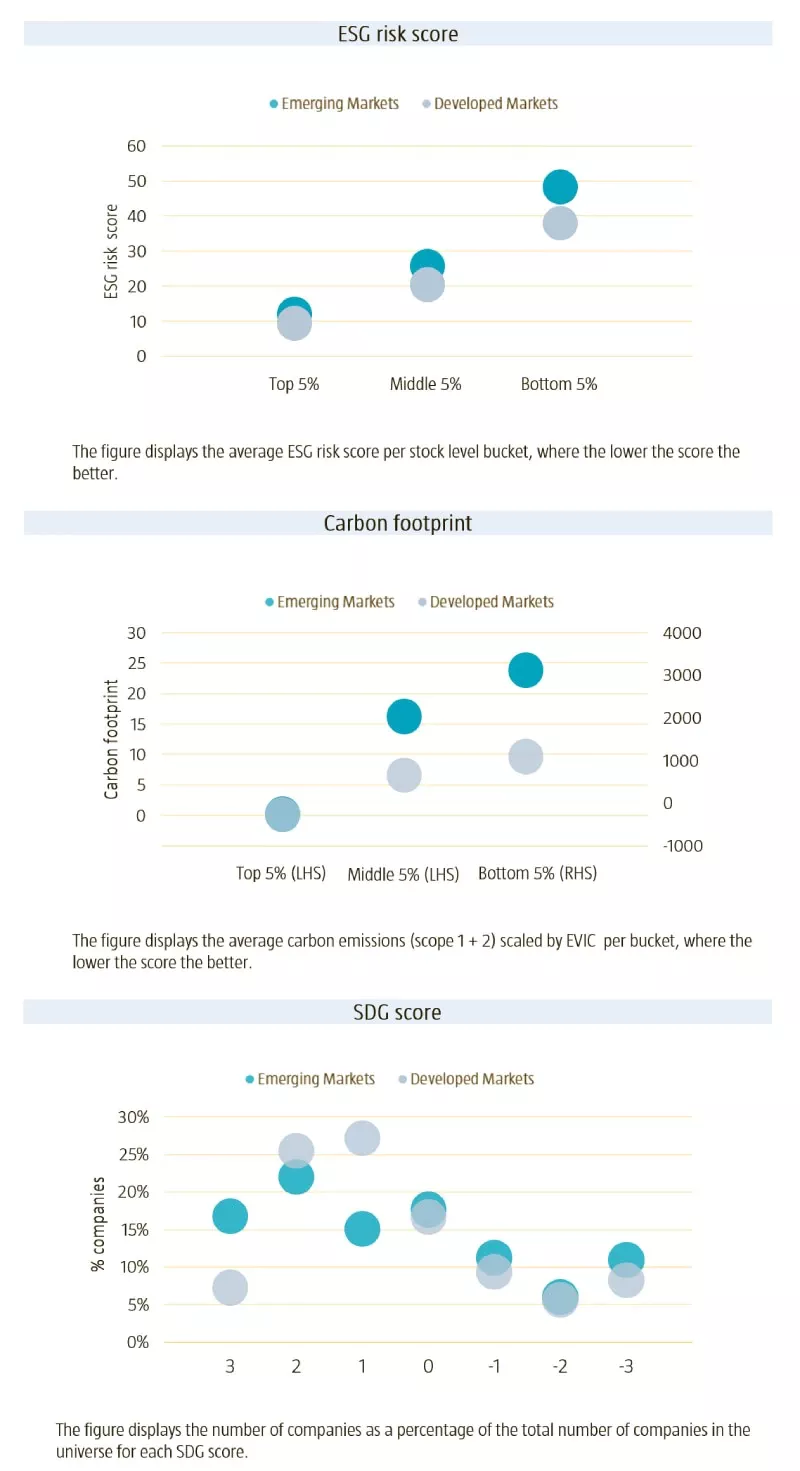

In addition to analyzing the dispersion at the country level, we look further into the dispersion at the stock level. This is important for the selection of companies in an equity portfolio. We divide the companies in each universe into 20 buckets based on their sustainability scores and present the average scores of the top, middle and bottom bucket in Figure 3. For SDG scores we present the percentage of companies for the seven different SDG values (from +3 to -3).

In line with our findings at the country level, we observe differences between emerging and developed markets at the stock level, and particularly for the worst-scoring companies.

Figure 3 | Average sustainability scores per stock level bucket in emerging markets versus developed markets

Source: Sustainalytics, Trucost, Robeco. Data as of March 2022.

Similar to our country-level conclusion, the worst-scoring companies in emerging markets are less sustainable than those in developed markets. However, we observe that the companies in the top-scoring levels in emerging markets are highly sustainable and rate similar to the top companies in developed markets or are even more sustainable when measured by the top SDG scores.

Ample data quality and coverage in emerging markets

In order to construct a portfolio with robust sustainability integration, that is not subject to selection bias and that is customizable, it is critical to have ample, high-quality data on various sustainability aspects.

Thanks to increasing demand from investors for transparency, stricter regulation for disclosures, our collaboration with trusted data suppliers and a growing team of sustainable investing analysts at Robeco, we have in recent years achieved a degree of coverage in emerging markets that is as wide as we have in developed markets.

Conclusion

Investors increasingly are focusing on sustainable investing in emerging markets. With wider data coverage and better data quality, emerging markets present significant opportunity potential for sustainable investors. These companies are not just sustainable according to emerging market standards but prove to be highly similar to their developed market counterparts. The big challenge is in identifying such sustainable companies in emerging markets.

Our analysis allows us to identify these companies by using a multi-dimensional sustainability approach. Robeco’s quant approach is designed to identify and benefit from these sustainable companies and to construct tailor-made solutions in an effort to meet investors’ unique financial and sustainability objectives.

1 This article is based on a more detailed paper by the same authors, “Marrying sustainability and emerging markets expertise in quantitative strategies”, June 2022.