Brent Humphries | President and Founding Member—AB Private Credit Investors Investors in middle market direct lending can realize incremental yield versus public corporate credit markets by making a longer-term commitment to the asset class. In our view, this yield advantage is compensation for illiquidity—a premium that has lasted year after year and across cycles. We do not believe investors are taking on added credit risk to capture that premium, which is well above historical norms today. In our view, this is an opportune time for investors looking to enter the market or add to existing exposure.

The Basics: What’s the Illiquidity Premium?

Middle market direct loans are underwritten with a buy-and-hold perspective: investors expect to hold the investment until it’s repaid. Stated loan maturities of five to six years are most common in the middle market, and loans most often repay in the second or third years. Because there’s no active, liquid secondary market for private loans, secondary trades are rare and require buyers and sellers to negotiate pricing directly. Longer-term commitments to borrowers require longer-term commitments from investors. As compensation for accepting less liquidity, investors demand incremental yield. Loan managers that are diligent in sourcing, underwriting and managing portfolios can capitalize on the inherent inefficiencies of private markets to generate incremental yield without taking on added credit risk. For investors that don’t need daily liquidity, this makes middle market loans attractive compared with traditional, tradable fixed income.

Investors’ Search for Yield Leads to Direct Lending

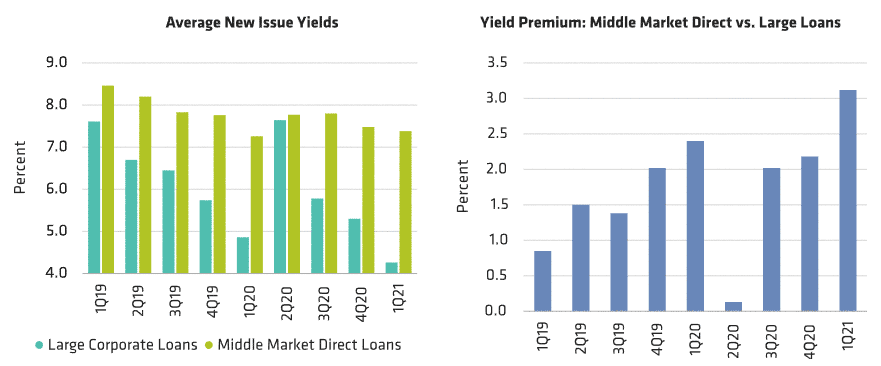

Extra yield is particularly attractive in today’s market, with accommodative monetary policy keeping downward pressure on risk-free rates in recent years. At the end of May 2021, the 10-year US Treasury bonds yield stood at 1.6%, well below the relatively recent high of 3.2% in late 2018. As investors have intensified their search for higher-yielding assets, capital flows have followed, helping drive yields lower across the investible public universe, with current yields on many credit asset classes near record lows. Yields have declined in middle market direct lending too, though not as much as in public credit markets. As a result, the direct lending yield premium has increased, strengthening the relative risk-adjusted return potential of middle market loans versus broadly syndicated loans (BSL) or high-yield bonds, for example. From the first quarter of 2019 to the first quarter of 2021, average new issue yields for BSLs declined 43%, from 7.6% to 4.3%. Middle market direct loan yields were more resilient, falling only 13% from 8.5% to 7.4% (Display, left). As a result, the difference in new issue yields between the two loan segments rose sharply in favor of the middle market—from about 85 basis points to more than 300 basis points, well above its historical range of approximately 150 to 225 basis points (Display, right).

Middle Market Direct Lending’s Expanding Illiquidity Premium

Past performance does not guarantee future results.

As of March 31, 2021

Large corporate loans reflect large loans executed via banks and non-bank lenders. Middle market loans reflect loans executed via non banks.

Source: Refinitiv

Technical Factors Contribute to Above-Average Illiquidity Premium

Stronger investor appetite for leveraged loans drove $13 billion of retail inflows in the first quarter of 2021, according to S&P Global. Industry observers cite two main factors for higher demand: First, historically low reference rates (including the fed funds rate, prime rate and LIBOR) have fueled the search for higher-yielding assets. Second, investors are seeking floating-rate assets to protect against the inevitable reversion to the mean when prevailing market rates rise.

Recent issuance of collateralized loan obligations (CLO), vehicles that collectively represent the largest buyer of leveraged loans in the US, has been healthy too, with approximately $39 billion of issuance in the first quarter of 2021. Recent inflows, paired with CLO issuance, put outsized downward pressure on public leveraged loan yields.

Because middle market direct lending isn’t as easily accessible and liquid as public credit, it has generally been more insulated from these dynamics. As a result, the middle market illiquidity premium has reached historic highs, making this segment particularly attractive in the current environment—both on an absolute and relative value basis.

Middle Market Yield Premium: Driven by Illiquidity, Not Incremental Credit Risk

Some investors may attribute the incremental yield from investing in the middle market to their perception of higher credit risk from investing in smaller companies, but our analysis suggests this is not the case. In fact, middle market direct loans have historically realized lower loss rates than those of larger transactions. Over the past 25 years, senior loans to middle market businesses (loans under $250 million) have realized a cumulative loss rate of 0.5% versus 0.7% for larger loans (loans over $500 million).

Several factors underpin lower loss rates for the middle market. Directly sourced, privately negotiated transactions tend to feature more conservative loan structures, such as less leverage and larger equity cushions. Middle market loans generally provide tighter legal documentation too. For example, middle market loans commonly incorporate maintenance covenants; BSLs, on the other hand, are most often covenant-lite. Also, stronger connectivity among lenders (typically sole or small club groups), borrowers and financial sponsors (if applicable), as well as more robust reporting, can enable lenders to act faster and more decisively in periods of portfolio company stress. Together, these factors have contributed to lower loss rates in middle market direct loans relative to BSLs.

To sum up, we believe that investors willing to forego liquidity for a portion of their portfolio by making a longer-term commitment to private credit can realize a meaningful yield premium without taking on added credit risk. In fact, the risk is arguably lower, based on historical loss ratios.

The middle market direct lending yield premium has been persistent year after year, and we think it makes sense to consider strategic exposure to the asset class within a diversified asset allocation. Today, the yield premium is well above historical norms, which we believe creates a timely and compelling opportunity to add or increase exposure to middle market loans.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.