No Regrets: The ECB Keeps Policy on Hold

Inflation in the euro area is falling and the economy is rapidly weakening. Against that background, the ECB kept rates on hold at its policy meeting today.

Investors broadly expected that the ECB would keep rates at 4%. But it was a welcome surprise that its Governing Council didn’t discuss bringing forward the end of reinvestments under the pandemic emergency purchase programme (PEPP). Doing so would have risked a significant rise in long-dated bond yields. That could have put further stress on Italy at a fragile time.

The ECB had previously said that it wouldn’t end its PEPP reinvestments “until at least the end of 2024.” So, reversing that commitment could have damaged its credibility. In our view, it will not regret keeping its policy on hold at this time.

Our Take on the Meeting

Thursday’s hold by the ECB marks its first pause in rate rises since it started hiking in the summer of 2022. And against investors’ speculation, the ECB announced no changes to its balance sheet operations. President Lagarde said that the ECB Governing Council hadn’t even discussed bringing forward the end of PEPP reinvestments today.

Lagarde emphasized that euro area inflation remains uncomfortably high. However, our assessment is that the ECB struck a dovish tone. Both Lagarde’s monetary policy statement and her comments emphasized that the euro area economy is weakening. Previous interest rate hikes are already hitting European households and firms – and forward-looking indicators suggest there is more pain to come.

That said, Lagarde noted that talk of interest rate cuts was “premature.” We think the ECB will want to see core inflation continue to fall in coming months, and wage growth ease in early 2024, before it even contemplates lower rates. That would make the second quarter of 2024 the earliest opportunity for a rate cut.

In addition, Lagarde highlighted the asymmetric impact of plausible shocks that could further challenge the euro area. Those could include higher energy prices, on the back of the Israel-Hamas conflict, and effects of climate change on food prices. If either risk crystallizes, inflation could stay high for longer against the backdrop of a stagnating economy – a toxic mix for any central bank.

The bottom line for us is that we welcome the ECB’s dovish tilt at today’s meeting, against the backdrop of a weakening euro area economy and falling inflation. That said, we expect interest rates to stay at their current levels well into 2024, particularly in light of the plausible upside risks to inflation.

The ECB’s continued silence on PEPP has made it less likely that it reneges on its commitment to continue reinvestment until at least the end of 2024. This should help contain Italian government bond spreads through the winter – another welcome development. Our forecast for euro area GDP growth in 2024 stands at 0.5%. Consensus has come down markedly over the course of this year, and currently stands at 0.8%.

Market Implications

The ECB’s decision to keep rates on hold and not alter its balance sheet runoff was also prudent from a market perspective. Financial conditions have deteriorated in the past weeks. The Middle East conflict has added a layer of uncertainty to the headwinds from higher government bond yields. Tighter monetary conditions could have been damaging for European assets.

Nervousness in global financial markets was already high, so it is difficult to gauge how prices reacted to the ECB’s meeting. However, there are several noteworthy patterns.

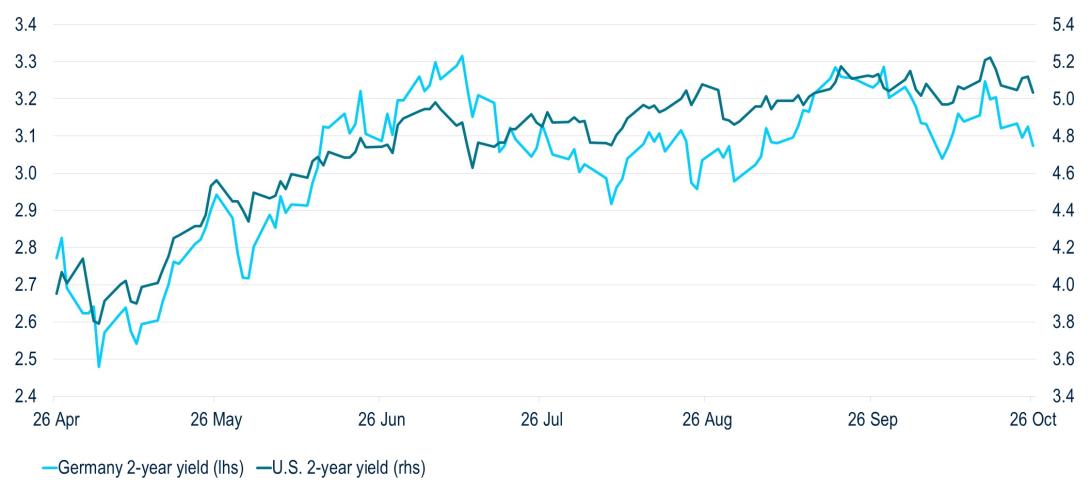

- First, the ECB’s decision to pause largely reflected a weaker economy and gradually falling inflation. As a result, German bond yields continued to fall. This contrasts with the more resilient U.S. economic outlook. So far in October, 2-year German Bund yields are down around 15 basis points, whereas 2-year U.S. Treasury yields are broadly flat (Figure 1). After today’s decision, the euro also weakened versus the U.S.-dollar, after several weeks of strength.

Figure 1: Two-year German Bund yields are lower so far in October, but 2-year U.S. Treasury yields are broadly unchanged

Source: Bloomberg, PGIM Fixed Income

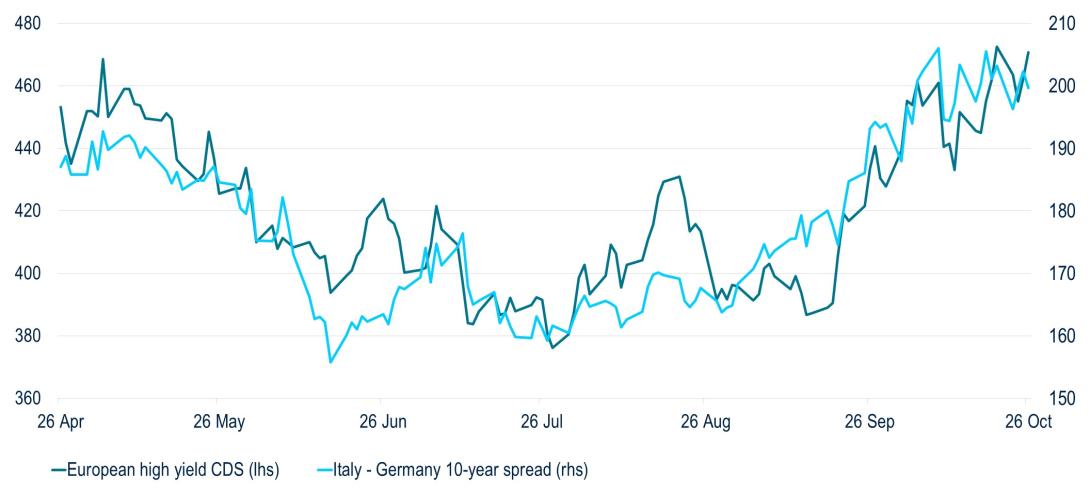

- A more important observation, we believe, is that the ECB’s decision to keep policy unchanged doesn’t necessarily reduce the risks to euro assets. It just doesn’t increase risk. Higher U.S. rates are spilling over to Europe and keeping financial conditions tight, even if the ECB leans dovish. In addition, the threat of another energy shock is real. In this context, it is unsurprising that corporate credit spreads and Italian government bond spreads to German Bunds remained wide even after the ECB’s decision (Figure 2).

Figure 2: Euro high-yield credit default swaps (iTraxx Crossover) and 10-year Italian government bond spreads over German Bunds have started to reflect a challenging macroeconomic and corporate outlook

Source: Bloomberg, PGIM Fixed Income

- Further, any news about the ECB bringing its balance sheet runoff forward could compound financial market risk, especially at a time when governments issue materially more debt than in previous years. This combination of tighter monetary policy and fiscal largesse has raised the term premium in the U.S. The same combination also presents in the euro area.

- Higher interest rates are restoring some value to euro-denominated fixed income. But conditions may not be supportive enough to give investors high conviction on euro risk assets just yet.

Read More From PGIM Fixed Income

The comments, opinions, and estimates contained herein are based on and/or derived from publicly available information from sources that PGIM Fixed Income believes to be reliable. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. Past performance is not a guarantee or a reliable indicator of future results.

Source(s) of data (unless otherwise noted): PGIM Fixed Income, as of October 26, 2023.

For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional.

These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy.

Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR.PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited including those available under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In Switzerland, information is issued by PGIM Limited, London, through its Representative Office in Zurich with registered office: Kappelergasse 14, CH-8001 Zurich, Switzerland. PGIM Limited, London, Representative Office in Zurich is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA and these materials are issued to persons who are professional or institutional clients within the meaning of Art.4 para 3 and 4 FinSA in Switzerland. In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a regulated entity with the Monetary Authority of Singapore under a Capital Markets Services License to conduct fund management and an exempt financial adviser. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 -Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2023 PFI and its related entities.

2023-7989

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in