More and more insurers are turning to private credit as a tool to try to enhance income, reduce volatility or diversify return streams. Insurance companies, particularly life insurers, have long focused on private placements in corporate and commercial real estate lending. They also lend to middle-market corporates, often partnering with third-party managers to source and manage these investments.

However, given the high amount of capital available for middle-market lending and the large corporate credit risk already in insurance portfolios, this focus may be too narrow. We think insurers should consider a more diversified allocation to private credit and expand into other privately originated credit assets globally, including residential mortgages, other parts of commercial real estate (CRE) lending, asset-backed securities, consumer loans and specialty finance.

Benefits of a broader view

Broadening the opportunity set in private credit can offer insurers several advantages.

First, it can allow their investment managers to take a more opportunistic approach to private credit. The benefits can be material, including greater ability to react to market overshoots and dislocations across credit assets, potentially resulting in attractive risk-adjusted returns. This is especially important today in the later stages of the credit cycle, as certain credit sectors have increased leverage faster than others and capital formation can differ dramatically across various private credit assets. As private credit becomes a larger, more structural allocation for insurers, we believe this opportunistic approach can better navigate economic cycles, while maintaining flexibility to target relative value opportunities across credit verticals and capital structures.

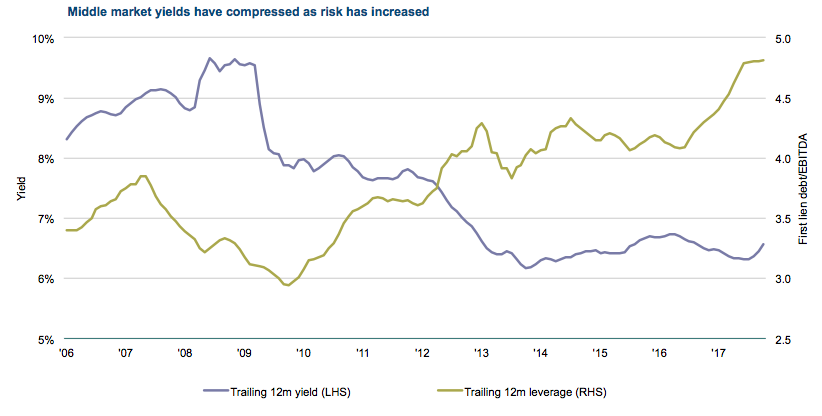

Froth in middle-market lending: capital formation and yields

Broadening the private credit opportunity set can also help insurers avoid too much exposure to specific sectors within corporate credit given various concentrations in public, private placement and middle-market debt.

The focus on direct originations to middle-market corporates has resulted in significant capital formation and supply/demand imbalances. Ultimately, this has led to lower yields and weaker deal structures for investors (see chart). The recent rapid pace of private fundraisings had created almost $100 billion in available capital for these loans by late 2017, according to Preqin; at the same time, public retail-oriented BDC (business development company) structures have grown to represent an additional $60 billion in capital, according to S&P LCD.

The capital imbalance is likely to continue growing, with more private fundraising, the BDCs’ move to capitalize on recent legislative changes allowing an additional turn of leverage to 2:1, and continued robust CLO (collateralized loan obligation) issuance, which we believe may add another $100 billion in annual demand for loans.

Insurance companies already have high corporate debt exposure, in particular growing allocations to BBB rated companies. More middle-market exposure would add to the potential impact of a corporate default cycle, which further supports the case for being opportunistic and diversifying into other private credit sectors.

Robust Capital Formation Has Created Froth In The Middle Market

As of 30 June 2018 | Source: LCD

For illustrative purposes. There can be no guarantee that the trends above will continue.

Where are the opportunities?

Credit markets have recovered at vastly different paces since the financial crisis in 2008-2009. We believe insurers should be mindful of the relative value across different lending markets.

While the corporate middle-market oversupply of capital has been reflected in less attractive pricing, weaker capital structures and lighter covenant protections, we see several other lending segments where complexity, dislocation or regulatory pressures have led to more balanced capital formation and attractive risk-adjusted returns through better pricing, stronger asset coverage and more favorable covenants. Risk management is crucial in the private credit sector, given the potential for market volatility and defaults, among other risks.

Here are three sectors where we see opportunity in private credit:

1. Residential mortgage lending

Re-regulation of the financial sector continues to hinder mortgage lending and has led to large financing gaps among high quality borrowers; continued disposition of legacy reperforming loans (RPLs); and opportunities to make transitional residential (“fix-and-flip”) loans. We also anticipate more opportunities in mortgage servicing rights over the coming years as nonbank lenders’ capital positions suffer from the slowdown in refinancing.

2. CRE lending

With commercial lenders facing similar regulatory limitations, transitional and value-add loans continue to offer value to investors with flexible private capital, in our view. These loans tend to have other attractive features as well, including shorter maturities, floating-rate coupons and strong covenants and collateral. Other opportunities in commercial real estate include credit tenant leases and small-balance mortgage lending.

3. Specialty finance

Capturing a broad array of receivables and esoteric asset-based financing, specialty finance markets may provide attractive opportunities for investors who have robust sourcing relationships, rigorous analytics capabilities and deep experience in deal structuring. Currently, PIMCO is finding opportunities in insurance, consumer and nontraditional asset-based financings in complex asset classes that are less trafficked and often have shorter maturities than many other private credit assets.

By taking a broader approach to private investments, insurers can bypass the crowds in middle-market lending and continue to rely on private credit in seeking to meet their income and return goals.

By PIMCO

Christian Stracke, Global Head of Credit Research

Christian Stracke is a managing director and global head of credit research at PIMCO.

Justin Ayre, Account Manager, Financial Institutions Group

Justin Ayre is an executive vice president at PIMCO, specializing in investment management services for financial institutions.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Private credit involves an investment in non-publically traded securities which are subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Investments in Private Credit may also be subject to real estate-related risks, which include new regulatory or legislative developments, the attractiveness and location of properties, the financial condition of tenants, potential liability under environmental and other laws, as well as natural disasters and other factors beyond a manager’s control. Residential or commercial mortgage loans and commercial real estate debt are subject to risks that include prepayment, delinquency, foreclosure, risks of loss, servicing risks and adverse regulatory developments, which risks may be heightened in the case of non-performing loans. Investing in distressed loans and bankrupt companies are speculative and the repayment of default obligations contains significant uncertainties. Diversification does not ensure against loss.

PIMCO does not offer insurance guaranteed products or products that offer investments containing both securities and insurance features. Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660, 800-387-4626. ©2018, PIMCO.

CMR2018-1119-366373