Under the new guidelines for New York insurers, shares of certain fixed income ETFs can receive bond-like capital treatment. The new regulatory stance has the potential to accelerate insurers’ adoption of fixed income ETFs.

Adoption of fixed income ETFs by insurance companies is poised to accelerate following a rule change by the New York Department of Financial Services. The new regulation treats the shares of certain fixed income ETFs in a manner similar to bonds for the purpose of an insurer’s risk-based capital report. Insurers generally hold significantly less risk-based capital against debt than equity securities.

According to the new guidelines, an ETF can receive bond-like capital treatment if it meets certain criteria, including:

- The portfolio of the ETF consists of investments in fixed income securities, cash, and cash equivalents;

- The ETF tracks a bond index (i.e., is not actively managed) and makes publicly available no less frequently than monthly a detailed list of its holdings;

- The ETF has a minimum of $1 billion in AUM;

- The ETF allows in-kind redemptions;

- The ETF is registered pursuant to the Investment Company Act of 1940, 15 U.S.C. §§ 80a-1 – 80a-64;

- The ETF is rated by a nationally recognized statistical rating organization;

- The ETF is identified as qualifying for bond treatment by the Purposes and Procedures Manual of the NAIC Investment Analysis Office and has a preliminary or final NAIC Standard Valuation Office designation.

In light of the ratings standard (#6 above), our team has worked expeditiously to secure ratings for many SPDR® fixed income ETFs. Today, 19 of our fixed income ETFs meet the New York regulatory criteria. You can see the full SPDR ETF line-up here, along with NAIC designations and ratings where applicable.

Along with other major industry participants, SPDR provided input to the New York Department of Financial Services on the regulatory change, and we applaud the Department’s approach. In our view, it strikes an appropriate balance of providing New York insurers the certainty and clarity necessary to allow them to treat reserve investments in certain fixed income ETFs as investments in bonds rather than as equities while also imposing high thresholds of eligibility criteria that ensure robust investor protections, transparency, and access to liquidity.

Regulatory Shift Likely to Accelerate Use of ETFs by Insurance Companies

In recent years, fixed income ETFs have become mainstream components of insurance companies’ portfolios, providing a way for insurers of all sizes to achieve access to bond investment exposure.

The updated regulatory stance in New York has the potential to further ignite US insurers’ adoption of fixed income ETFs.

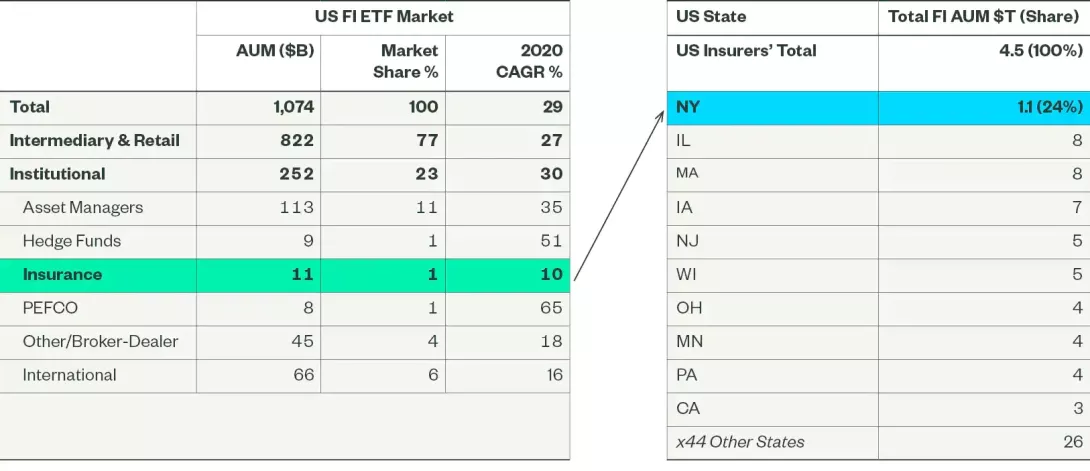

As shown below, US insurance companies’ total fixed income ETF investments previously amounted to $11 billion, or 1% of total bond ETF assets. New York insurers account for $1.1 trillion in fixed income AUM, equivalent to 24% of the US total. This appreciably large pool of capital is now better positioned to use ETFs within their bond portfolios.

US Insurers Fixed Income ETF Adoption

Source: Schedule D filings, as of December 31, 2020, via S&P Global Market Intelligence.

ETFs Provide Tools for Duration Management Ahead of Fed Policy Recalibration

Duration management is emerging as a central theme as investors prepare for a less accommodative policy stance from the Federal Reserve.

For insurance companies — including New York firms with newly expanded abilities to use fixed income ETFs — short-duration credit strategies may offer a highly liquid portfolio management solution to mitigating the impact of rising rates.

| Ticker | SPDR ETF | 2021 Designation1 | S&P Rating | Meets New York Criteria | Option Adjusted Duration as of 2/2/2022 |

|---|

| BIL | SPDR® Bloomberg 1-3 Month T-Bill ETF | Preliminary NAIC 1.A | 'AAAf

/S1+' | Yes | 0.15 years |

| SPSB | SPDR® Portfolio Short Term Corporate Bond ETF | Preliminary NAIC 2.A | 'BBB+

f/S1' | Yes | 1.81 years |

Source: State Street Global Advisors, as of February 2, 2022.

As an ETF leader, our expertise has helped us build trusted partnerships with top insurance companies. To learn more about how we may be able to assist you and your clients, please reach out to the SPDR Insurance team, Benjamin Woloshin and Dewey Yoo.

For additional information, you can also access the following resources:

Download the report here

Footnote

1 Preliminary NAIC Designations are the intellectual property of the National Association of Insurance Commissioners (NAIC) and are redistributed here under License. A Preliminary NAIC Designation is an opinion of the NAIC Securities Valuation Office (SVO) of the probable credit quality designation that would be assigned by the SVO to an investment if purchased by an insurance company and reported to the SVO. A Preliminary NAIC Designation is only one of the regulatory factors considered by the SVO as part of its analysis of probable regulatory treatment under the Regulatory Treatment Analysis Service (RTAS). A full discussion of such other regulatory factors is set forth in the RTAS Letter provided to State Street Global Advisors. A Preliminary NAIC Designation cannot be used to report the ETF to state insurance regulators. However, the purchasing insurance company may obtain an NAIC Designation for the ETF by filing the security and final documents for the ETF with the SVO. The indication of probable regulatory treatment indicated by a Preliminary NAIC Designation is not a recommendation to purchase the ETF and is not intended to convey approval or endorsement of the ETF Sponsor or the ETF by the NAIC.

NAIC Designations are the intellectual property of the National Association of Insurance Commissioners (NAIC) and are redistributed here under License. An NAIC Designation is a proprietary symbol used by the NAIC Securities Valuation Office (SVO) to denote a category or band of credit risk (i.e., the likelihood of repayment in accordance with a written contract) for an issuer or for a security. NAIC Designations may be notched up or down to reflect the position of a specific liability in the issuer’s capital structure and/or the existence of other non-payment risk in the specific security. Under NAIC reporting rules, shares of an ETF are presumed to be reportable as common stock. The SVO may classify an ETF as a bond or preferred stock and assign it an NAIC Designation if it meets defined criteria. For a discussion of these criteria please call the SVO or refer to the Purposes and Procedures Manual of the NAIC Investment Analysis Office. The assignment of an NAIC Designation is not a recommendation to purchase the ETF and is not intended to convey approval or endorsement of the ETF Sponsor or the ETF by the NAIC.

NAIC designations should not be construed as an indication of the current or future profitability of any investment.

Disclosures

The views expressed in this material are the views of SPDR Insurance Team through the period ended February 8, 2022 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

Prior to 10/31/2021, the SPDR Bloomberg 1-3 Month T-Bill ETF was known as the SPDR Bloomberg Barclays 1-3 Month T-Bill ETF.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

There can be no assurance that a liquid market will be maintained for ETF shares

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

NAIC designations are assigned to securities held by state-regulated insurance companies by the Securities Valuation Office (SVO) of the National Association of Insurance Commissioners (NAIC). Designations are opinions of credit quality, and range from the highest quality of 1 to the lowest of 6. A higher quality designation results in less capital requirements to support the insurers’ investments. Unlike the ratings of nationally recognized statistical rating organizations, NAIC designations are not produced to aid the investment decision making process and therefore are not suitable for use by anyone other than NAIC members.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

4322287.1.1.AM.INST

Exp. Date: 02/28/2023