The post-pandemic inflation shock and rate-hiking cycle produced a generational reset higher in bond yields, creating a compelling multiyear outlook for fixed income as inflation recedes and risks build in other markets.

The global economy continues to recover from pandemic aftershocks, including trade dislocations, outsize monetary and fiscal interventions, a prolonged inflation surge, and bouts of severe financial market volatility. At PIMCO’s 2024 Secular Forum, we explored how the aftereffects of those disruptions are producing some unexpectedly positive developments while also introducing longer-term risks.

Among the positives, disinflation has occurred more rapidly than anticipated in most developed market (DM) economies. Moreover, macroeconomic and inflation risks look more balanced than they did at our prior Secular Forum a year ago. Central banks are also poised to pivot toward rate cuts, likely on different schedules.

However, we see three main areas where investors have benefited but may be overlooking risks that could develop over our five-year secular horizon:

- Large-scale fiscal stimulus has fueled recent standout U.S. growth, but that exceptionalism has come at a cost: The U.S. is on an unsustainable debt trajectory that the government will ultimately need to address. Meanwhile, financial markets may increasingly need to operate without expectation of government support.

- Artificial intelligence (AI) is poised to realign labor markets and boost productivity, but significant economic impacts may take years. Massive capital investment has accompanied rapid stock market gains in ways reminiscent of past tech booms.

- Asset valuations in some markets offer investors little apparent cushion. This includes equities, where valuations appear stretched, and lower-rated corporate direct lending markets that are less liquid and more exposed to floating interest rates.

For investors, the early 2020s inflation shock and steep policy rate hikes produced a generational reset higher in bond yields, which now embed significant inflation-adjusted cushion. Starting yields are highly correlated with five-year forward returns. That supports an attractive long-term outlook for fixed income returns as inflation recedes, particularly on a risk-adjusted basis relative to other assets. Opportunities across global bond markets also appear uncommonly attractive and diverse, with active country and security selection being key.

We believe this secular backdrop merits a rethinking – and even a reversal – of the traditional 60% stocks / 40% bonds asset allocation paradigm.

As banks retreat from certain markets, we also see attractive opportunities in asset-based lending, particularly consumer-related areas given the strength of the U.S. consumer. We expect bank disintermediation and capital needs will create opportunities in commercial real estate (CRE) debt.

Our Secular Forum sessions explored how the U.S. and China are leading a shift toward a multipolar world order that is likely to alter market and policy dynamics. The peace dividend that countries enjoyed in recent decades is turning into a conflict expense that could be a disruptive force.

Secular theme: Balanced risks, but beware golden ages

Our 2023 Secular thesis, “The Aftershock Economy,” argued that the early 2020s disruptions would create an enduring new reality. We saw a world of elevated macroeconomic volatility and sluggish growth. We predicted that central banks would do whatever it takes to return inflation to “2-point-something” percent.

While this thesis broadly continues to hold, our outlook for the next five years must incorporate and assess major developments since our May 2023 forum:

- A war breaking out in the Middle East and a war in Europe dragging into its third year

- Rapid and – so far – painless disinflation to “2-point-something” percent in most DM economies

- Material divergence of inflation and growth trajectories between the U.S. and other DM economies

- An unforeseen doubling of the U.S. budget deficit in an economy with near record low unemployment

- An October “Treasury tantrum” triggered by worries that the unsustainable U.S. fiscal trajectory will worsen in the years ahead

- Continued bank retrenchment amid tightening regulations for capital and liquidity

Our secular views also build upon our latest Cyclical Outlook, “Diverging Markets, Diversified Portfolios.” That outlook sees central banks breaking ranks to follow varied rate-cutting paths, with relative U.S. strength persisting while many large DM economies slow. That has produced a “re-risking” theme in U.S. financial markets, as well as questions about whether these trends are short-term or more enduring.

Central banks have maintained flexibility …

The sharp post-pandemic cyclical adjustments that rippled through the global economy are now giving way to more lasting secular trends and with important implications. While we continue to expect sluggish global growth and more volatile business cycles over our secular horizon, the risks around that outlook appear better balanced than they did a year ago.

That’s partly due to the quick return of inflation in most advanced economies to “2-point-something” percent levels. Rapid policy tightening brought the inflation spike under control and did so without medium-term inflation expectations rising.

The better balance of risks is also due to central banks’ tacit adoption of an “opportunistic disinflation” strategy to navigate the remaining journey toward target levels. This strategy allows policymakers some leeway to lower rates to support growth at times when inflation appears subdued.

Concerns we had last year about tight monetary conditions triggering financial instability have not materialized. Systemic risks to global banking and nonbank financial markets appear contained.

That said, regulatory trends are clearly moving toward stricter bank capital and liquidity requirements. Banks’ inability to provide balance sheet capacity in certain markets will likely further push many lending activities to private capital.

We see a growing window for investors to step in as senior lenders in areas once occupied by regional banks, such as consumer lending, mortgage lending, and equipment finance. CRE will also present opportunities for flexible capital, as bank retrenchment exacerbates challenges posed by declining real estate prices and a more than $2 trillion wall of maturing loansFootnote1 over the coming years.

… But fiscal space is constrained

While the monetary policy backdrop has improved, the fiscal outlook has not. The global fiscal trajectory was a focus of this year’s Secular Forum, especially the path of U.S. federal debt.

It remains to be seen whether cyclical U.S. economic strength is durable or merely fueled by pandemic-period government support and a rising debt-to-GDP ratio. If the U.S. eventually faces a fiscal reckoning, debt consolidation through entitlement spending reforms and higher taxes is likely. However improbable it seems in the current political environment, even the seemingly untouchable may have to evolve.

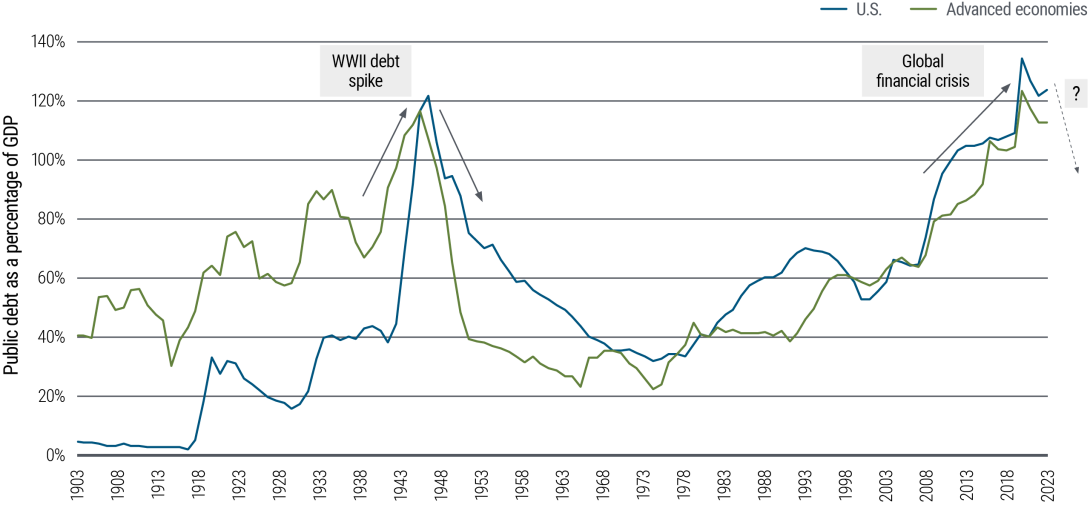

The massive stock of sovereign debt relative to GDP hanging over advanced economies (see Figure 1) will likely cause yield curves to steepen over our secular horizon, as investors continue to demand more compensation on longer-term bonds. There is evidence – for example, forward inflation-indexed yields or estimates of the Treasury term premium – to suggest that markets have already priced in some of this adjustment, even before central banks start to cut rates (to learn more, see our recent piece, “Will the True Treasury Term Premium Please Stand Up?”).

Figure 1: Fiscal space likely to be limited

Source: International Monetary Fund (IMF), Carmen Reinhart, Kenneth Rogoff, PIMCO; annual data through December 2023. “Advanced economies” refers to G-20 advanced economies (Australia, Canada, France, Germany, Italy, Japan, South Korea, U.K., and U.S.) through 2015 and all IMF-defined advanced economies through 2023.

Authorities will almost surely face more constraints when looking to discretionary fiscal policy to limit the damage from future business cycle downturns. Our baseline is not a sudden financial crisis, but recurring episodes of market volatility when focus shifts to fiscal issues.

Despite these fiscal pressures, we believe that the U.S. dollar will remain the dominant global currency, in no small part due to the lack of a viable challenger. A U.S debt reckoning could eventually come about, but it’s not likely imminent given U.S. advantages in immigration, productivity, and innovation; U.S. Treasuries being a global reserve asset; and the general dynamism of the U.S. economy. An elevated demand for U.S. Treasury securities as a “safe haven,” liquid store of value has, to date, limited the bond market’s concerns about fiscal sustainability. That suggests the timeline for fiscal reforms may be super-secular.

The U.S. may still be the “cleanest dirty shirt” compared with other economies. China’s outlook is challenged by property sector recession, an aging population, and less-open export markets. In Europe, fragmented politics will make it difficult to build a comprehensive growth strategy in the face of regional conflict, energy insecurity, and more direct competition from China on higher-value manufactured goods.

Moving to a multipolar world

The geopolitical landscape is increasingly defined by tensions between a dominant superpower (the U.S.) and its rising rival (China). Both China and Russia have clear long-term visions that are at odds with Western ideals. The peace dividend realized over the past three decades is becoming a conflict outlay.

This underscores a shift toward a multipolar world order, where cooperation seems limited and new middle powers may emerge. The shift will likely also lead to changing correlations across markets and increased divergence in potential growth and policy responses. Business cycles will likely also be less synchronized. We expect the underlying forces will lead to greater macroeconomic and financial market volatility than pre-pandemic.

Risks to financial stability have also increased and could become problematic should these conflicts begin to materially alter cross-border financial flows or create conditions for capital impairments. We believe the risk premium for credit investment in China is too low to be attractive given potential risks.

We expect China’s growth to continue slowing without stalling. Notably, China is re-globalizing. Its new growth model, focused on production and infrastructure to counterbalance a property sector collapse, is driving a rise in manufacturing exports. This pivot requires reevaluating China’s role in the global economy, especially its impact on commodity markets and inflation, as well as its integration into the global financial order.

Major emerging markets (EM) have displayed remarkable resilience this cycle. The typical combination of factors that often trigger EM crises – capital flight, tighter financial conditions, and a collapse in commodity prices – is not currently evident, nor does it appear likely to emerge over the secular horizon. Debt levels in EM countries are increasing but so far remain at sustainable levels compared with DM.

Roughly 60% of the world by GDP weight will be voting in a major election this year. With early signs of populist parties gaining support – particularly in Europe – global elections have scope to change both economic and geopolitical policy priorities. We see risks that elections increase trends toward fragmentation, multipolarity, and protectionist measures, favoring friend-shoring investments. Countries such as India, Indonesia, and Mexico are positioned to benefit.

Turning to the U.S. presidential election, we believe trade, tax policy, immigration, regulation, and environmental policy have the greatest scope for disruption. U.S. fiscal deficits are likely to remain near historic highs regardless of the election outcome. Both political parties are also focused on remaining tough on China.

AI effects coming into focus

Generative AI has the potential to transform labor markets and democratize access to decision-making tasks, enabling more of the workforce to make informed decisions.

But many organizations will face challenges as they seek to leverage AI effectively. Dramatically enhanced productivity and efficiency may not be evident in the macro data over the next five years. This is because maximizing the payoff from AI at the macro level will require not only adoption of the technology itself, but also the reconfiguration of work streams and the rethinking of production processes at the micro level of individual organizations.

Similar to the experience with other new technologies over the past few decades, there may not be much of an incremental impact on productivity from modest enhancements of existing work practices. But there is a chance of breakthrough changes that could have a larger impact on productivity growth in certain specific areas, such as healthcare and science.

While our base case is that the full impact of new AI large language models manifests gradually over the secular horizon, it’s possible that disruptions may occur more quickly. The capital spending boom in computing, data centers, and green energy technology increases availability of these resources for applications beyond AI, while AI investment makes AI-supported breakthroughs in other fields increasingly plausible. Downside surprises are possible as well, especially if misuse of AI models for surveillance, manipulation, or security threats results in innovation-stifling restrictions.

For now, capital spending can lead to a shorter-term sugar high. Ultimately, efficiency gains will be needed to generate longer-term sustainable growth.

The demand for chips, data centers, and the generation capacity that will power them is expected to be explosive, and these trends will have immediate sectoral consequences.

Neutral policy rates to remain low

Today’s elevated policy rates are the result of cyclical forces, namely an inflationary spike. Once inflation stabilizes near central bank targets, we expect neutral monetary policy rates in advanced economies will likely settle at levels below those that prevailed before the global financial crisis.

We believe the neutral nominal policy rate in the U.S. over our secular horizon will likely remain in the range of 2%–3% (implying a long-run neutral real rate of 0%–1%). By contrast, current pricing indicates markets expect the neutral rate may not fall far below 4%. That can present further opportunities for bond investors, as yields today already embed cushion in the form of positive real rates and term premium.

We expect central bank balance sheets, which are currently contracting under quantitative tightening (QT) programs, will remain substantially larger than before the era of quantitative easing (QE). DM central banks will likely continue to use asset purchase programs to ensure the smooth functioning of sovereign debt and repurchase markets, and to act as lenders of last resort. Examples include the U.S. Federal Reserve’s 2023 Bank Term Funding Program and the Bank of England’s 2022 operation to support the U.K. gilt market.

However, we think it is less likely that central banks deploy open-ended QE asset purchase programs in response to future economic downturns. The financial strain of maintaining large securities portfolios, where the costs of funding exceed the returns from these assets, has become increasingly apparent.

Monetary and fiscal puts – or expectations of government relief in the event of downturns – are further out of the money today. That constrains the government’s ability to stimulate flagging economies and provide support to dampen shocks. We expect additional volatility as markets trade more on fundamentals and less on the expectation that governments will come to the rescue.

Investment implications: Fixed income resurgence

Our 2024 Secular Outlook favors a renewed focus on public fixed income markets, which we believe are poised to generate competitive returns and lower risk compared with other asset classes. Today’s yields and a stabilizing inflation outlook are enabling bonds to reassert their fundamental advantages in portfolios: providing potential for attractive income, downside resilience, and stability through reduced correlation with equities.

Many sophisticated asset allocators have moved well beyond the traditional 60% stocks / 40% bonds paradigm. Even so, it remains an oft-cited rule of thumb that frames many investment conversations. We believe we are entering an era that warrants a rethinking and a reversal of that concept.

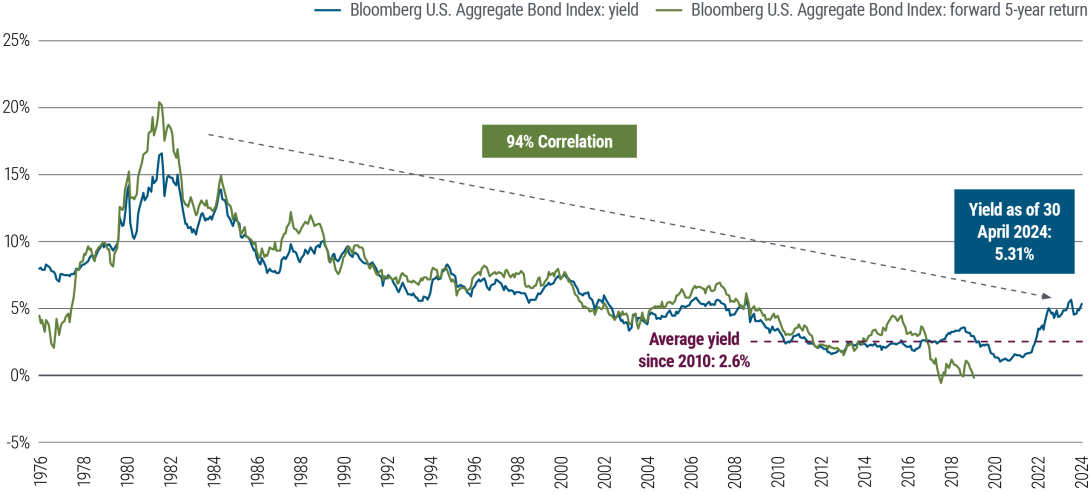

The post-pandemic inflation shock and subsequent central bank rate-hiking cycle reset bond yields sharply higher. Historically, starting yields are highly predictive of bond returns over a multiyear horizon (see Figure 2). The yields on the Bloomberg U.S. Aggregate and Global Aggregate (hedged to U.S. dollar) Indexes, two common benchmarks for high quality bonds, are about 5.31% and 5.41%, respectively, as of 30 April 2024.

Figure 2: Starting yields in bond markets historically correlated with 5-year forward returns

Source: Bloomberg, PIMCO as of 30 April 2024. Past performance is not a guarantee or a reliable indicator of future performance. Chart is provided for illustrative purposes only and is not indicative of the past or future performance of any PIMCO product. Yield and return are for the Bloomberg U.S. Aggregate Bond Index. It is not possible to invest directly in an unmanaged index.

Using that as a baseline, active investment managers can seek to enhance the yields investors earn. By identifying attractive opportunities in high quality areas – such as agency mortgage-backed securities – active managers can currently construct portfolios yielding about 6%–7% without taking on significant interest rate, credit, or illiquidity risk.

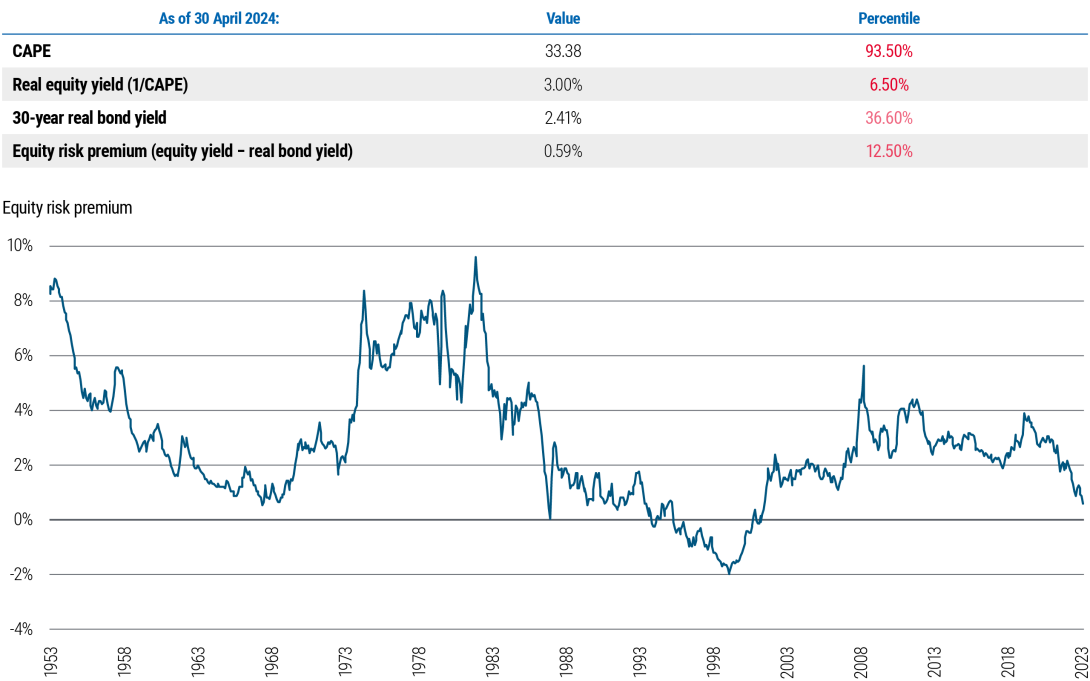

As a result, a diversified bond allocation offers the potential for long-term equity-like returns with a more favorable risk-adjusted profile, especially given what may be stretched valuations in stock markets (see Figure 3). Markets don’t appear to price significant recession risk, meaning bonds may be an inexpensive means to hedge that risk.

Figure 3: Equities screen expensive on an absolute basis and relative to U.S. Treasuries

Source: Bloomberg, Robert Shiller online data, Global Financial Data, PIMCO as of 30 April 2024. All value metrics are relative to the S&P 500 Index. CAPE is the cyclically adjusted price/earnings ratio. Real equity yield ratio refers to the average real earnings over the past 10 years divided by the last price. 30-year real bond yield corresponds to the yield on 30-year U.S. Treasury Inflation-Protected Securities (TIPS), backfilled with the nominal yield on 30-year U.S. Treasuries minus expected inflation. To compute inflation expectations, we estimate trend inflation according to Cieslak and Povala (2015) calibration and forecast inflation 30 years ahead.

Bonds today also embed a term premium that offers a cushion. We expect yield curves to steepen as policy rates decline and the term premium builds (for more, read our February PIMCO Perspectives, “Back to the Future: Term Premium Poised to Rise Again, With Widespread Asset-Price Implications”), and we have a curve steepener as a structural trade.

In the wake of its longest-ever inversion, the U.S. yield curve remains relatively flat. That means investors do not need to take a lot of interest rate risk. We currently find value at the 5-year part of the yield curve and are wary of potential underperformance of the long end due to fiscal concerns. Active fixed income is positioned to perform well if there are no recessions over our secular horizon and to perform even better if there are, with the potential for price appreciation if yields decline, which makes bonds attractive compared with cash, in our view.

Global bond markets offer particularly attractive and diverse opportunities that investors might be overlooking as a way to enhance yield without significantly increasing risk. Global yields – across DM and EM – have returned to attractive levels. Many economies outside of the U.S. face more fragility yet enjoy better starting fiscal conditions, both supportive of bonds.

We expect business cycles will be less synchronized, which will lead to lower correlations across financial markets. The differentiation in central bank policies and market conditions across regions presents unique opportunities for active, global investment platforms to capitalize on these discrepancies and potentially further enhance returns through country and security selection. Industrial subsidies and trade policies promoting onshoring, friend-shoring, and the energy transition will likely create both sectoral and national winners and losers, presenting further opportunities for active investors.

Given potential volatility around inflation, U.S. Treasury Inflation-Protected Securities (TIPS), commodities, and real assets offer inflation-hedging properties and higher real rates than pre-pandemic levels.

Prioritize credit selection and liquidity

While credit spreads appear broadly fair overall, credit and sector selection are poised to become more important over our secular horizon. Growth in both public and private credit markets should give active investors with flexible capital more opportunities during periods of volatility.

Many stronger, more resilient companies generate significant cash and don’t rely heavily on financing. Many weaker companies tend to need greater ongoing access to credit. The more productivity-enhancing AI technologies are, the more disruptive they are likely to be across companies and industries, creating more winners and losers. In the past, the advent of new technologies has often been followed by boom-bust cycles, creating volatility but also presenting bottom-up active investment opportunities.

We expect increased regulation for banks, which should lead to more disintermediation and more money flowing through private markets. Our focus remains on liquidity gaps arising from banks being pressured to manage capital and meet regulatory requirements. For example, this bank retrenchment will likely create opportunities for flexible capital in CRE debt, as we expect large-scale capital needs for asset owners facing a wall of loan maturities.

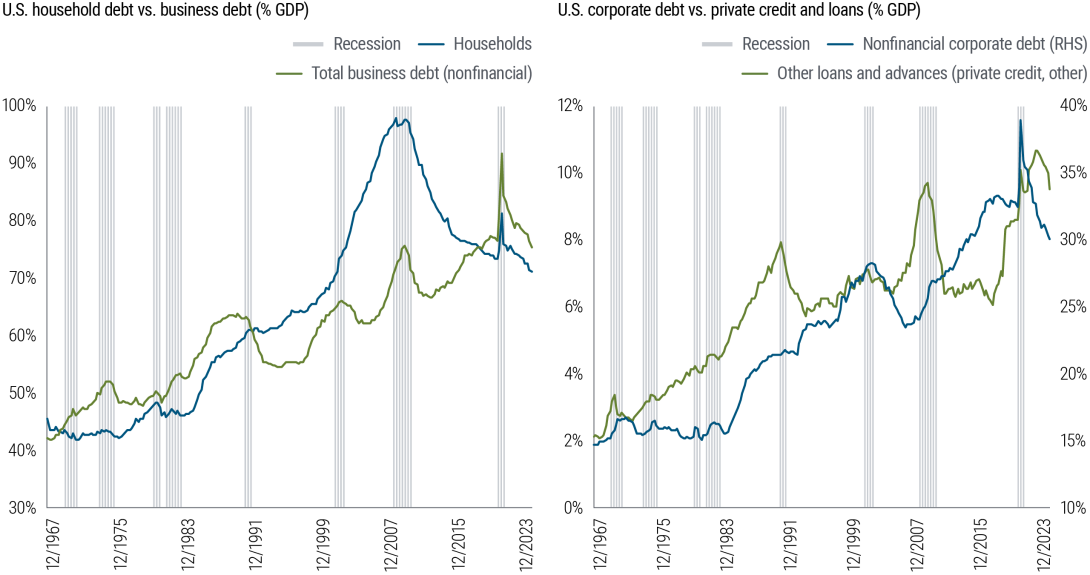

Asset-based lending is a prime example of what we see as an attractive and less crowded investment opportunity. Middle-market corporate lending appears to be in favor within private markets, but we believe areas such as consumer lending offer outstanding long-term fundamentals and value as U.S. household leverage has declined (see Figure 4) and housing markets remain well-supported.

Figure 4: Household debt has declined, while private corporate lending has grown

Source: Federal Reserve Flow of Funds data, Haver Analytics, PIMCO calculations as of 31 December 2023. Note: Nonfinancial corporate business other loans and advances category is used as an indicative proxy for assets such as private credit and bank loans.

We would contrast that with the amount of capital now concentrated in corporate lending. We are very concerned about the rapid growth within private, floating-rate markets that may not have been tested through prior default cycles. These conditions increase the risk of excesses building in areas such as technology and direct lending to companies with high leverage and lower credit ratings. Challenges could emerge during our secular time frame.

Given the high potential for returns in the more liquid segments of the bond market, investors should have a high hurdle – in the form of attractive return potential and strong lender covenants – for giving up liquidity. At today’s yield levels, the risk-adjusted return potential of broadening exposure to public fixed income markets – such as increasing allocations to high quality DM and EM bonds – also compares favorably with the trade-offs involved in extending into less liquid areas of credit markets.

1 According to Newmark Research calculations, as of 12 February 2024.

Download Article

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. U.S. agency mortgage-backed securities issued by Ginnie Mae (GNMA) are backed by the full faith and credit of the United States government. Securities issued by Freddie Mac (FHLMC) and Fannie Mae (FNMA) provide an agency guarantee of timely repayment of principal and interest but are not backed by the full faith and credit of the U.S. government. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Private credit involves an investment in non-publically traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. Diversification does not ensure against loss.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2024, PIMCO.

CMR2024-0524-3604901